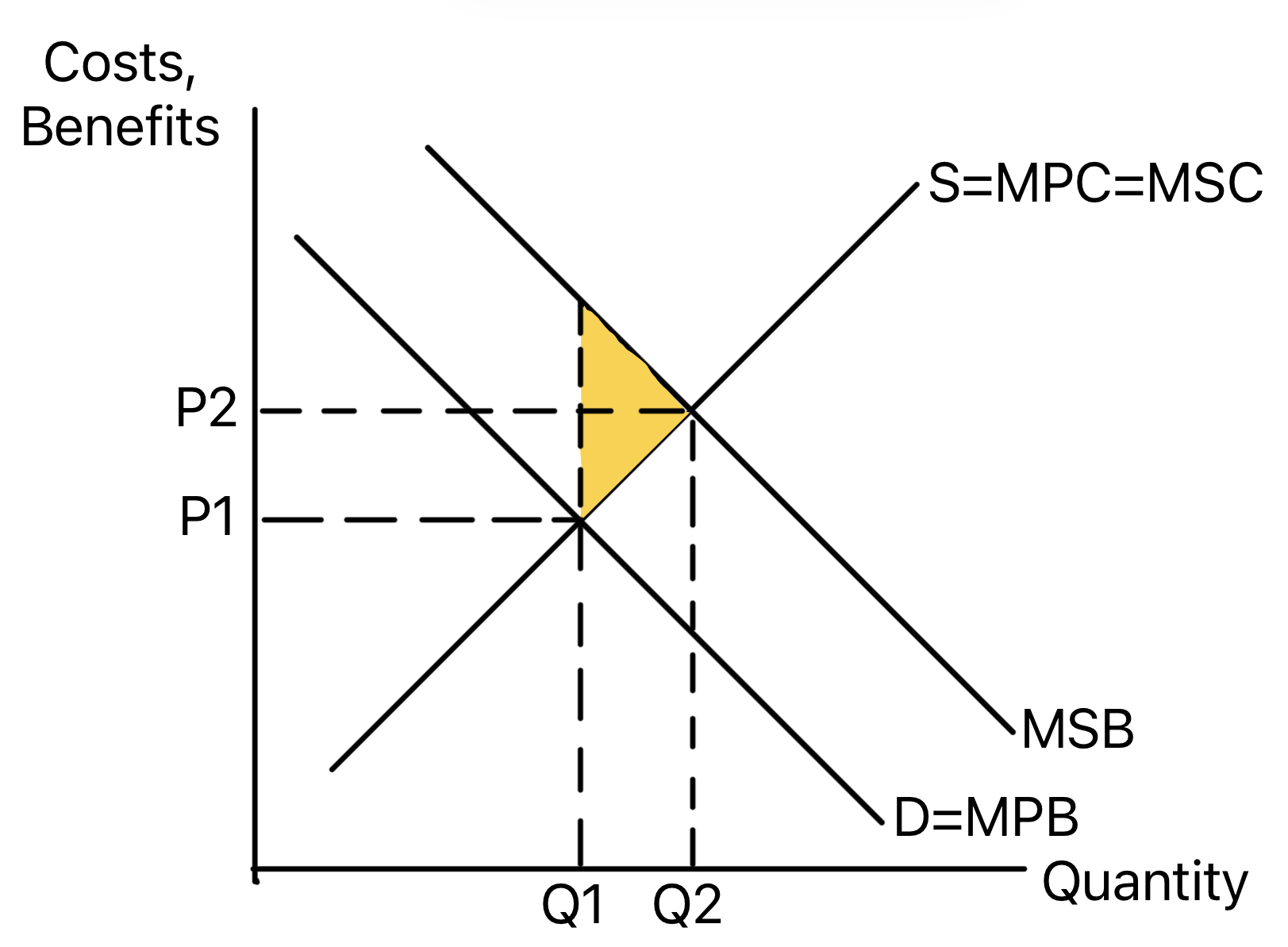

Edexcel A-Level Economics (9EC0) | Theme 1 and Theme 3

A single revision page for the microeconomics diagrams used across

the Edexcel Theme 1 and Theme 3 notes. Each card keeps the

original diagram image and adds a quick explanation of what to

show in an exam answer.

Diagram collection: This page includes the

diagrams currently referenced in the Edexcel Theme 1 and Theme 3

revision notes, with exact duplicate image files included once.

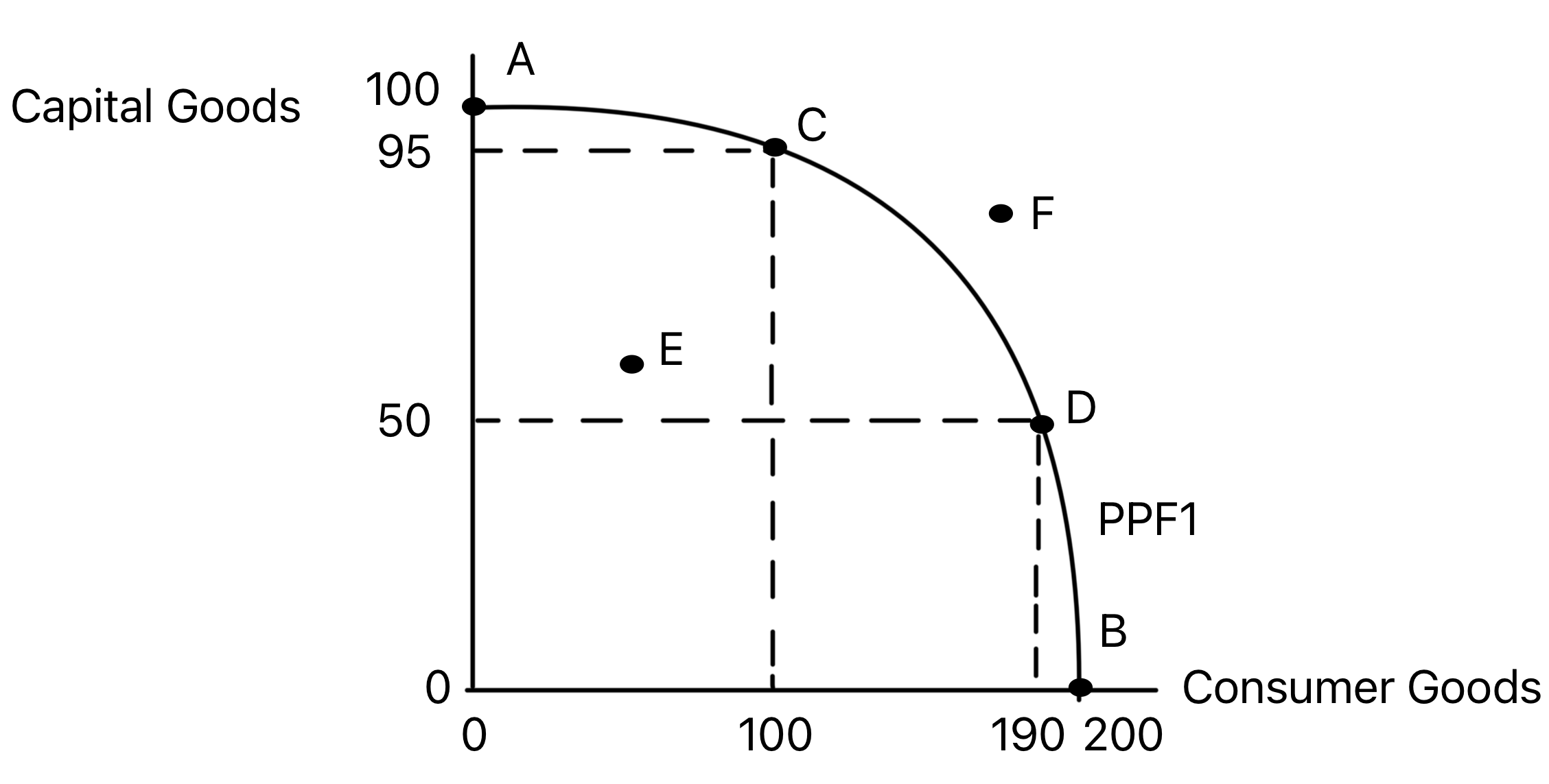

Shows the maximum combinations of two goods that can be

produced with existing resources and technology.

The curve shows scarcity, opportunity cost and productive

efficiency. Points on the frontier are productively

efficient, points inside it show unemployed or inefficiently

used resources, and points beyond it are currently

unattainable.

Use in exams: Use it for trade-offs,

opportunity cost, productive efficiency and short-run spare

capacity.

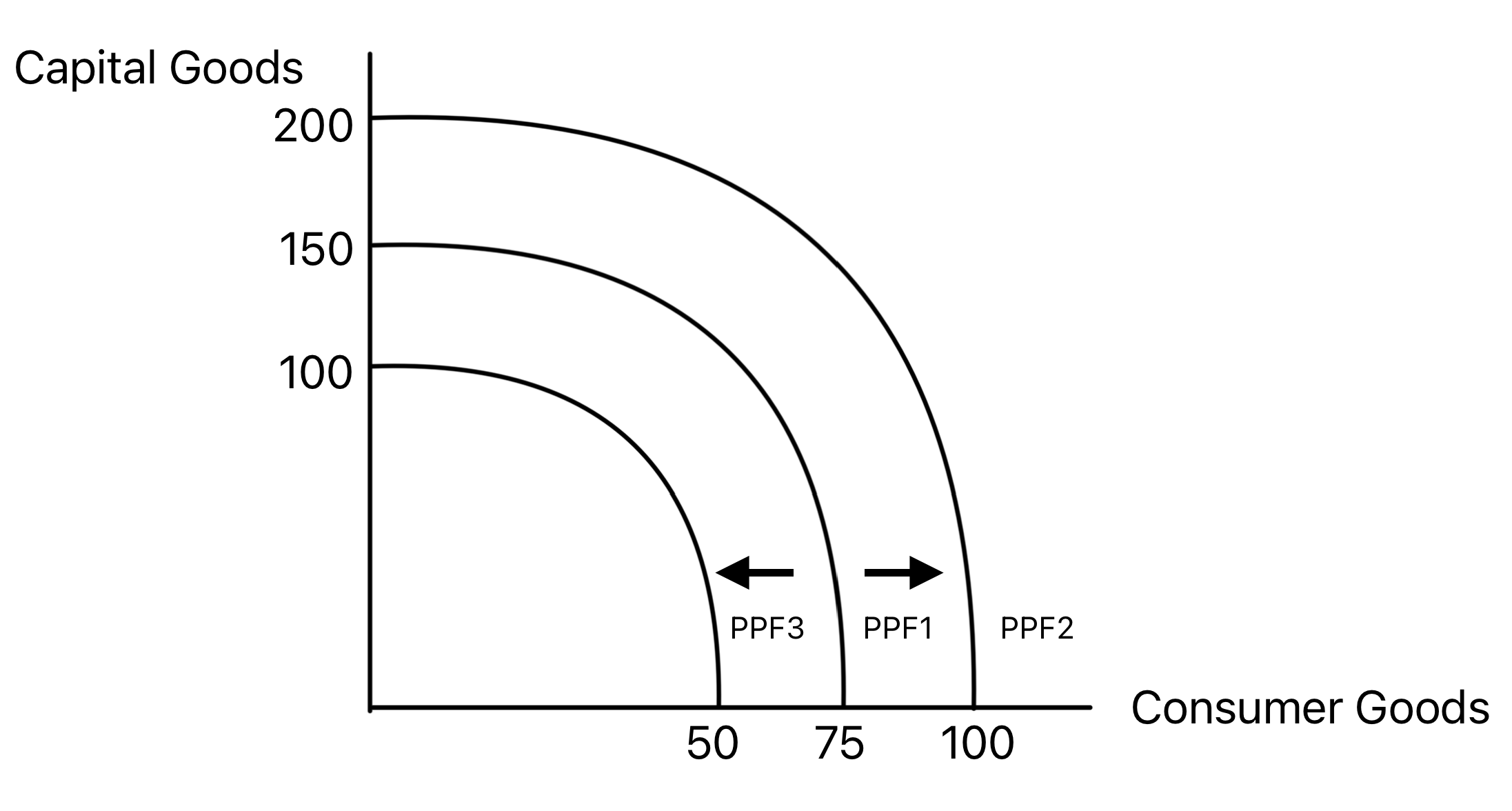

Shows how an economy's productive potential changes when

productive capacity rises or falls.

An outward shift represents economic growth caused by more

or better-quality resources, improved technology, or higher

productivity. An inward shift represents a loss of

productive potential.

Use in exams: Use it when explaining

long-run growth, natural disasters, investment, education,

migration or technological progress.

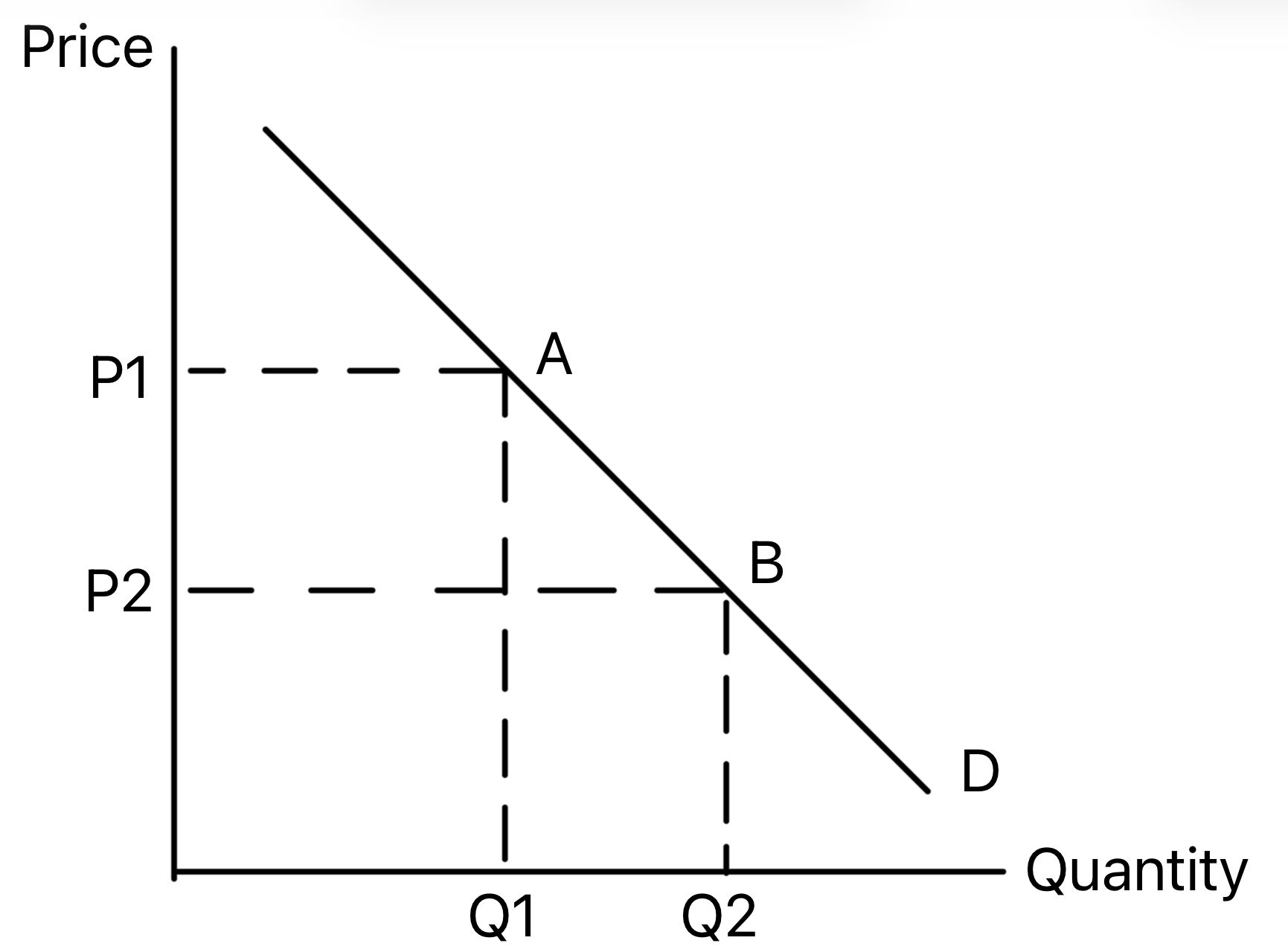

Shows an extension or contraction in quantity demanded

caused by a change in the good's own price.

A fall in price causes an extension down the demand curve,

while a rise in price causes a contraction up the curve. The

demand curve itself does not shift.

Use in exams: Use it when the only direct

cause is a change in the price of the product itself.

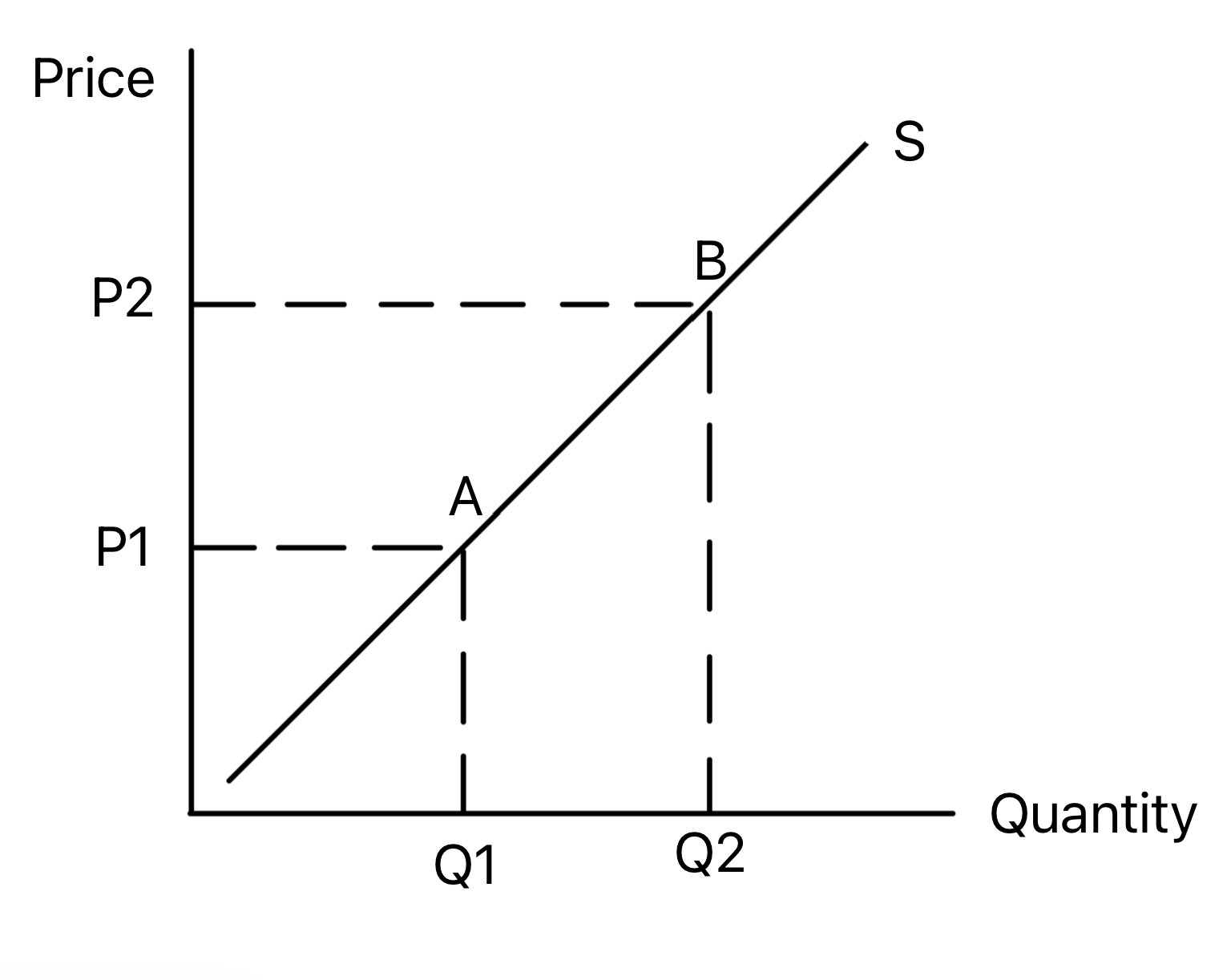

Shows an extension or contraction in quantity supplied

caused by a change in the good's own price.

A rise in price normally causes an extension up the supply

curve, while a fall in price causes a contraction down the

curve. The supply curve itself does not shift.

Use in exams: Use it when producers respond

to a price change rather than a change in production

conditions.

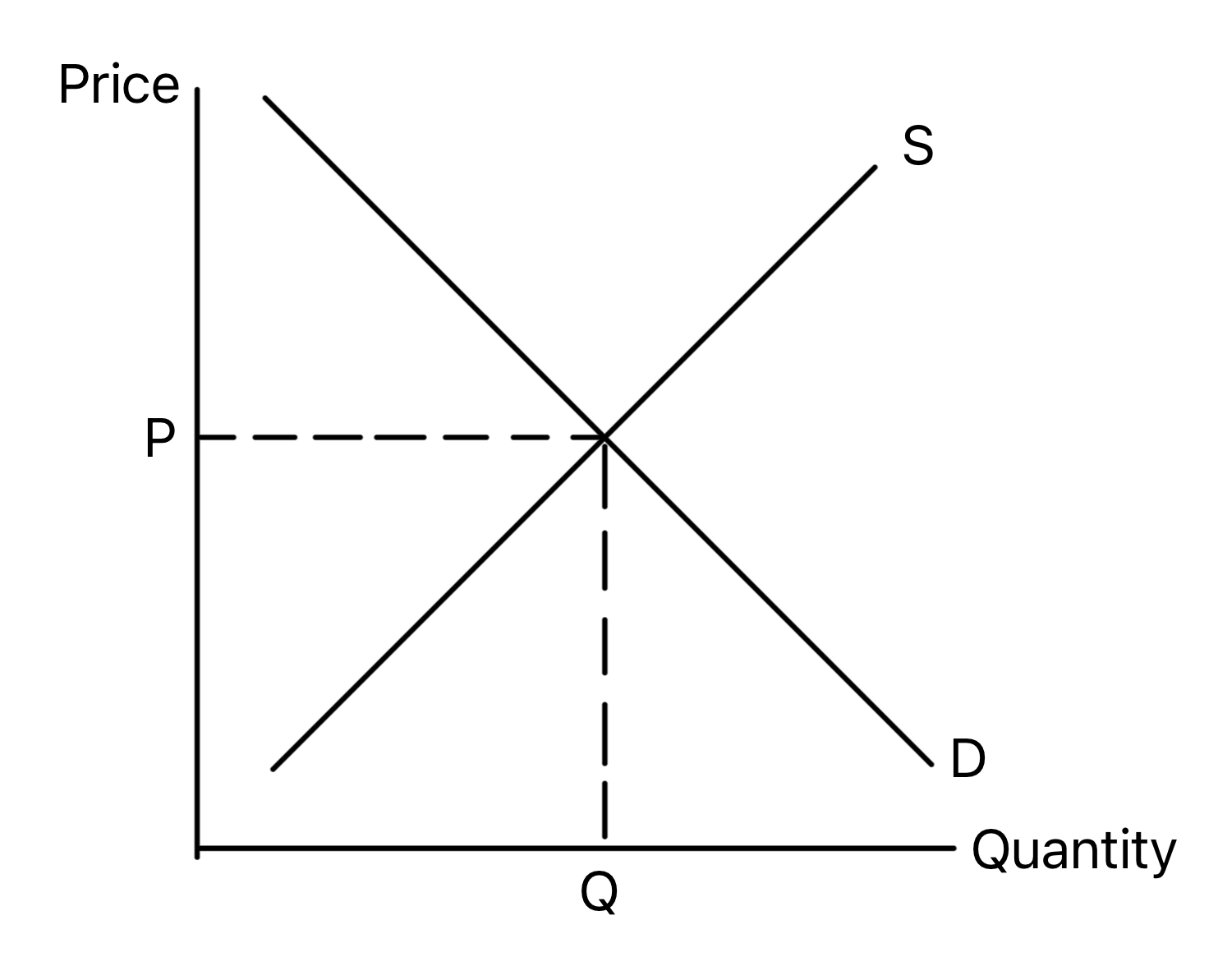

Shows the price and quantity where demand equals supply.

Equilibrium occurs where quantity demanded equals quantity

supplied. At this point there is no tendency for price to

rise or fall, assuming ceteris paribus.

Use in exams: Use it as the starting point

before showing a shift, shortage, surplus or intervention.

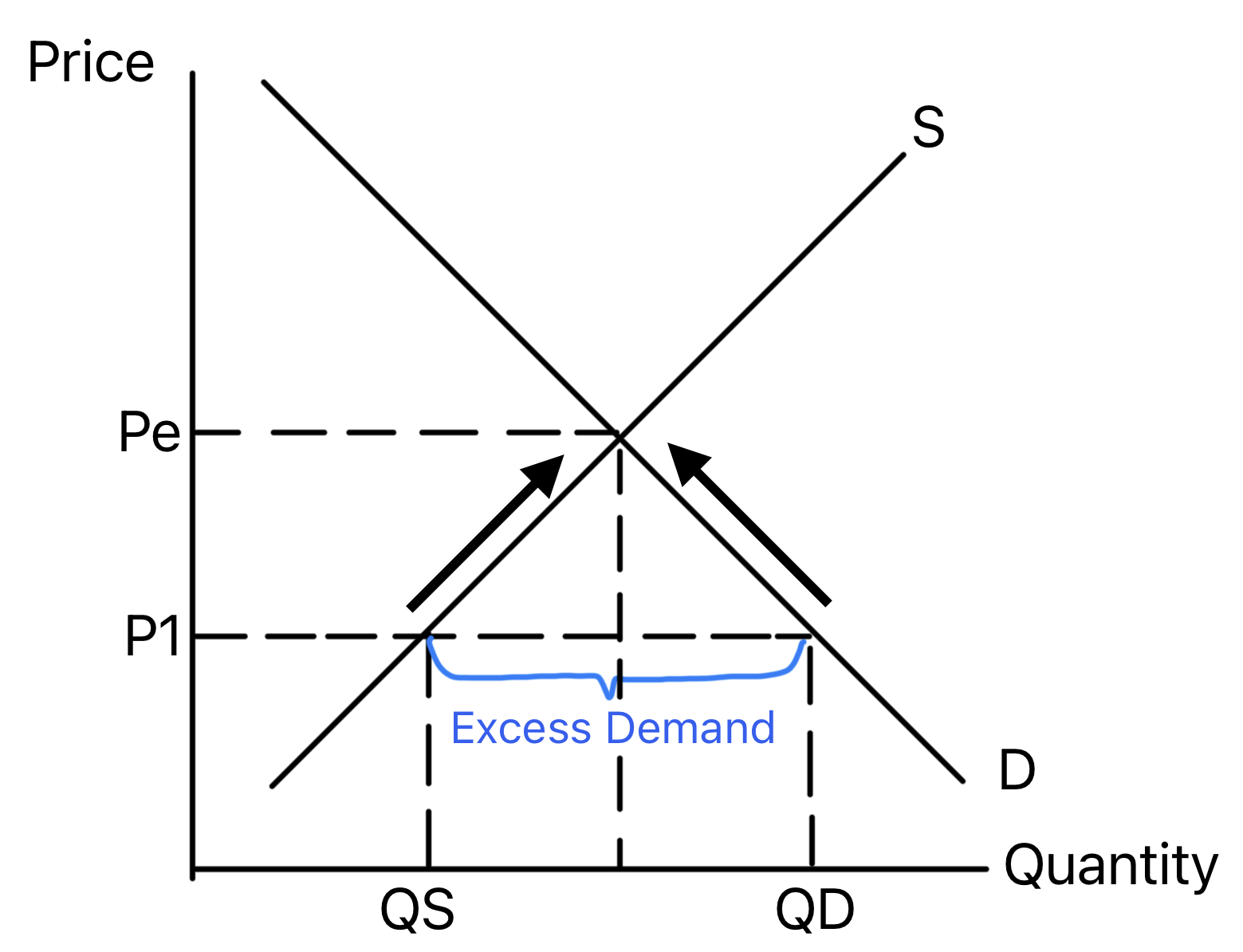

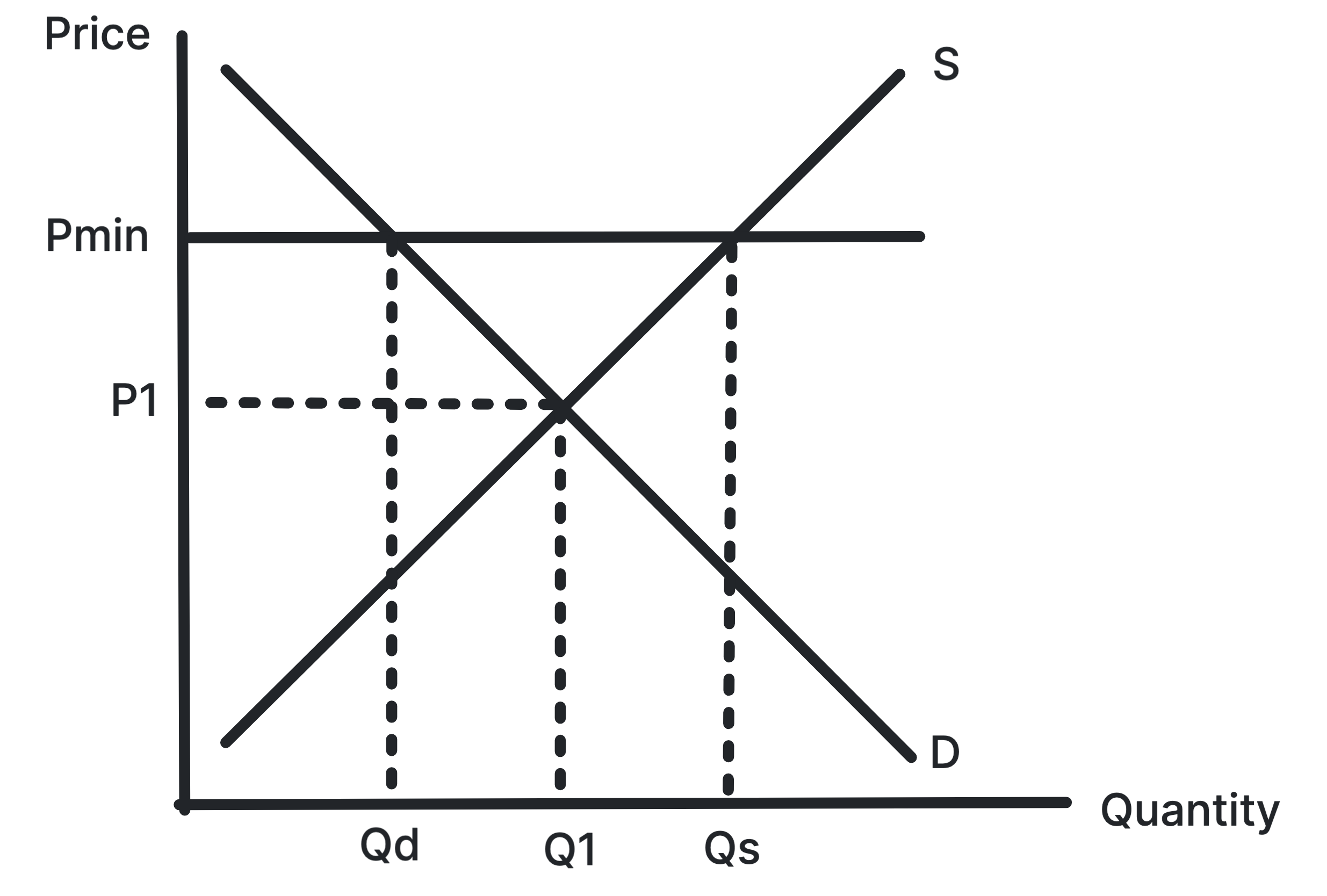

Shows a shortage when price is set below the equilibrium

price.

At a price below equilibrium, consumers want to buy more

than firms are willing to supply. Competitive pressure

should push prices up toward equilibrium.

Use in exams: Use it for shortages,

rationing, queues and maximum price controls below

equilibrium.

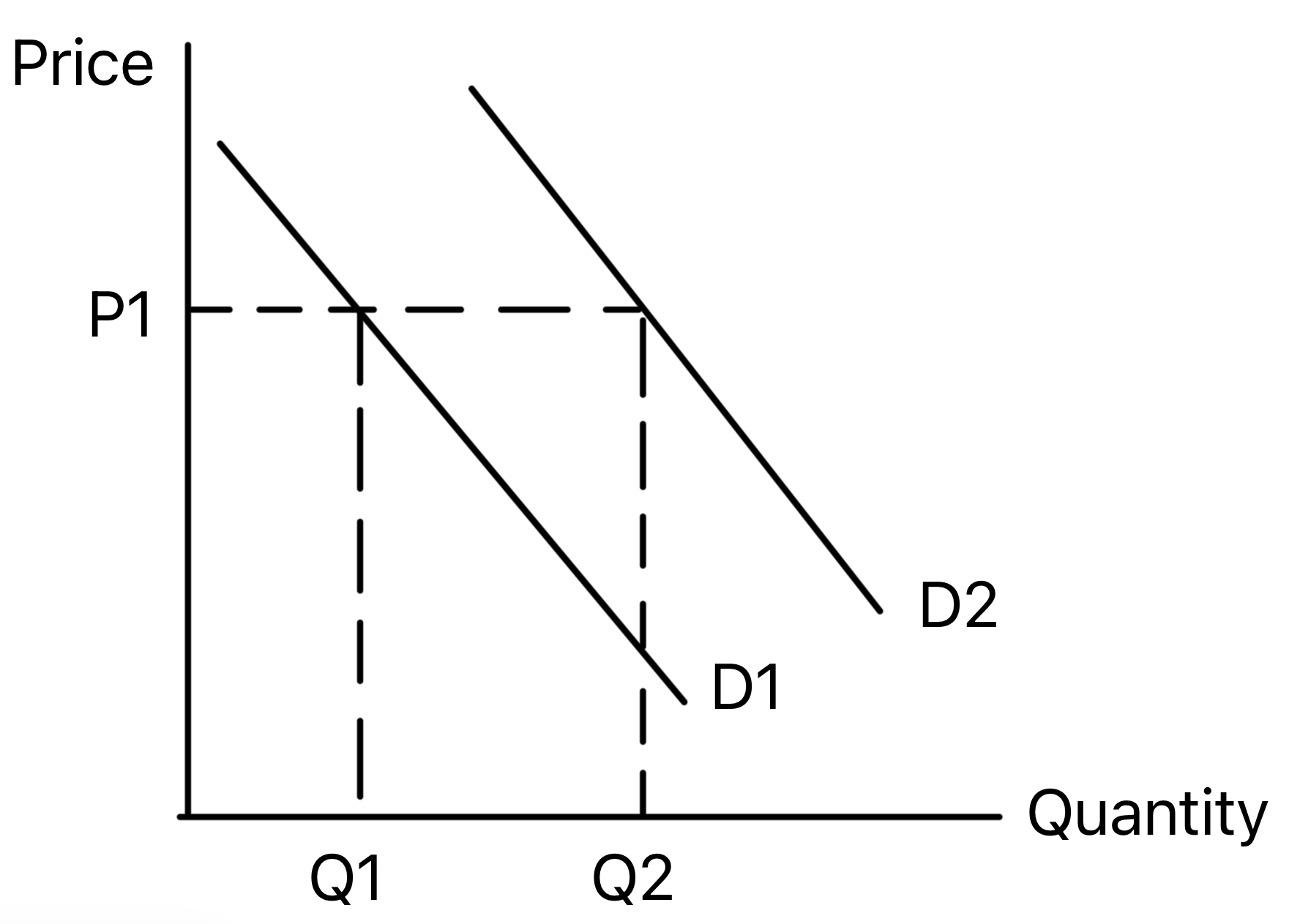

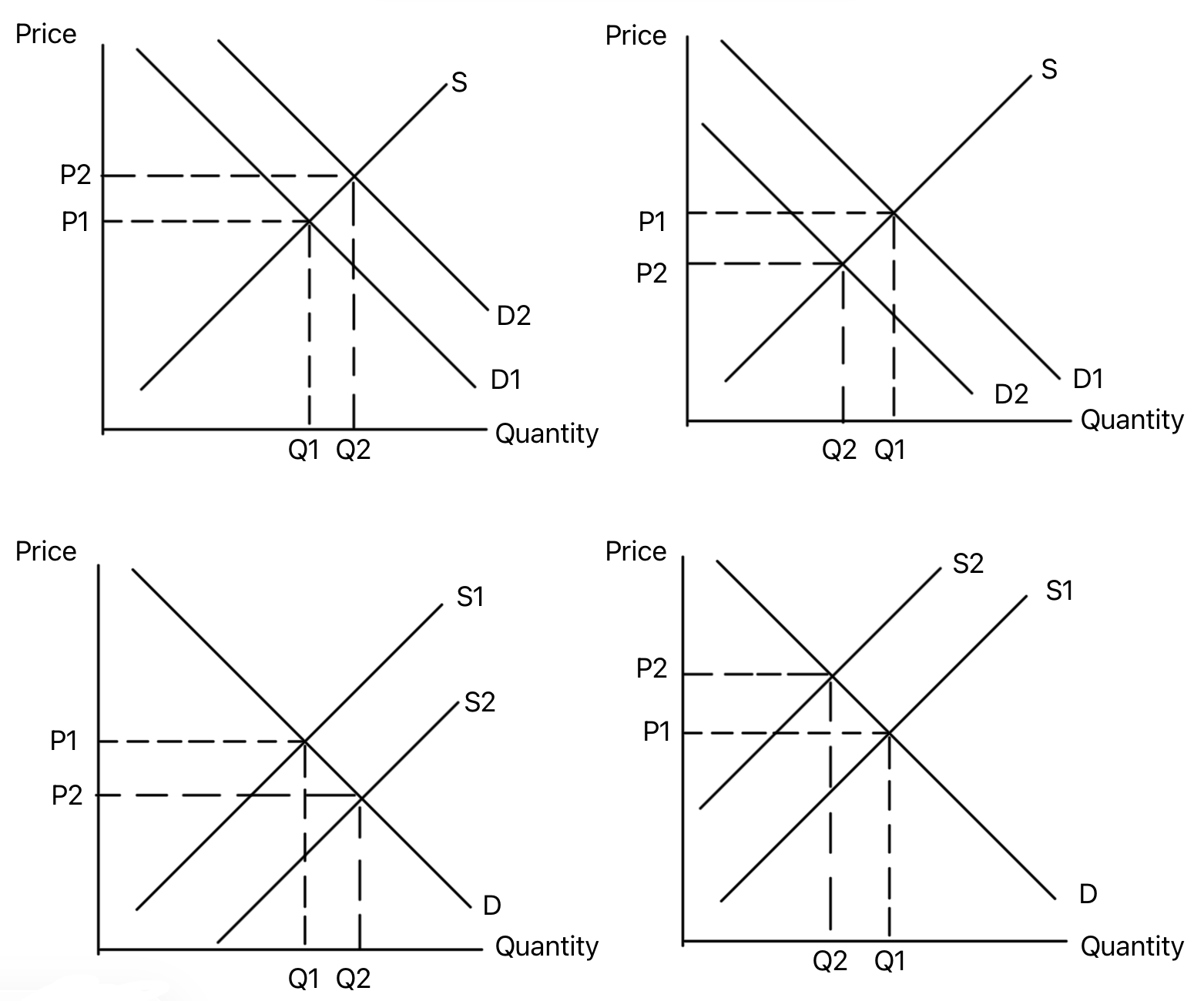

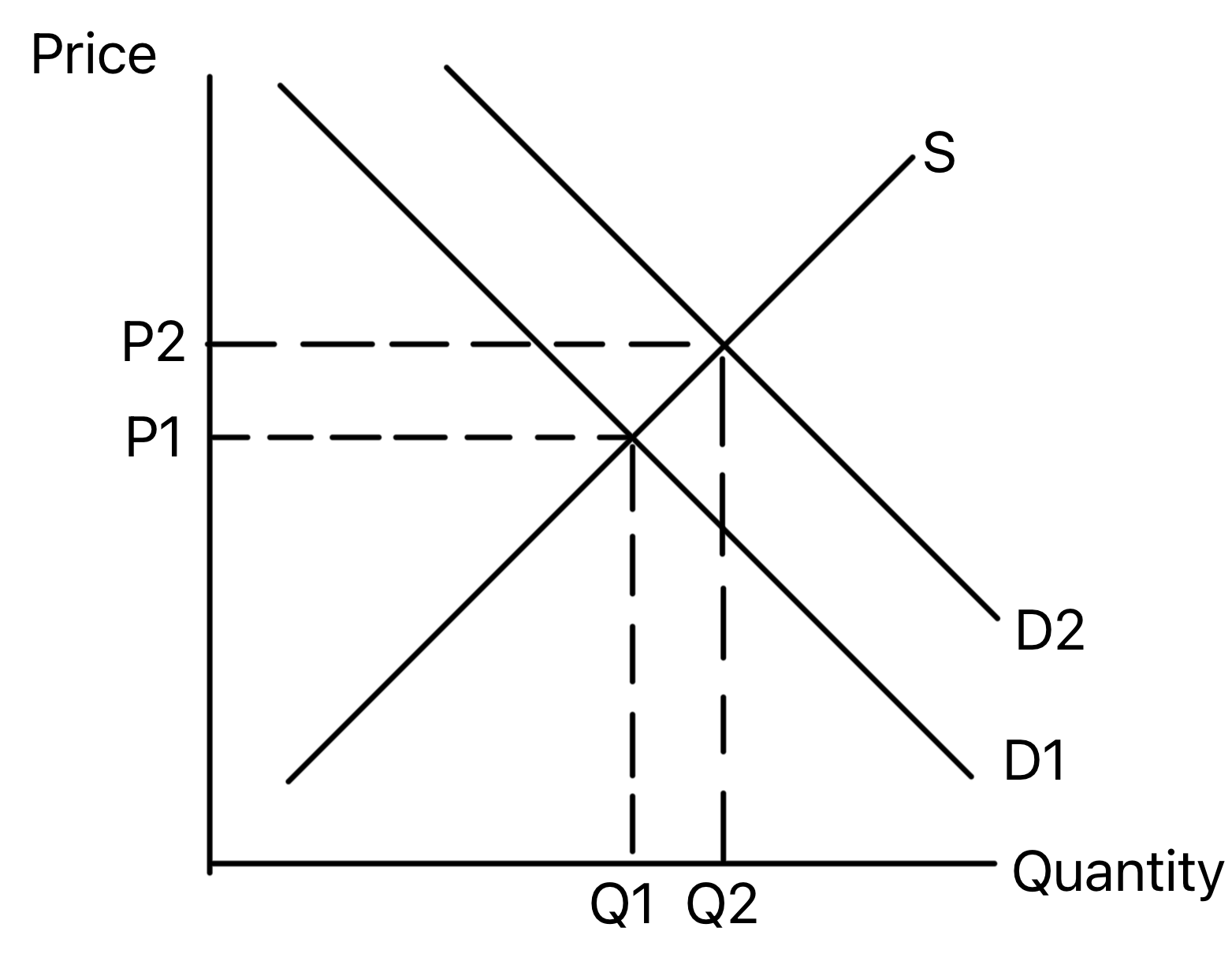

Shows demand shifting right, causing a higher equilibrium

price and quantity.

A rise in demand creates excess demand at the original

price. Price then rises, encouraging more supply and

reducing quantity demanded until the market clears.

Use in exams: Use it for rising popularity,

higher income for normal goods, or higher prices of

substitutes.

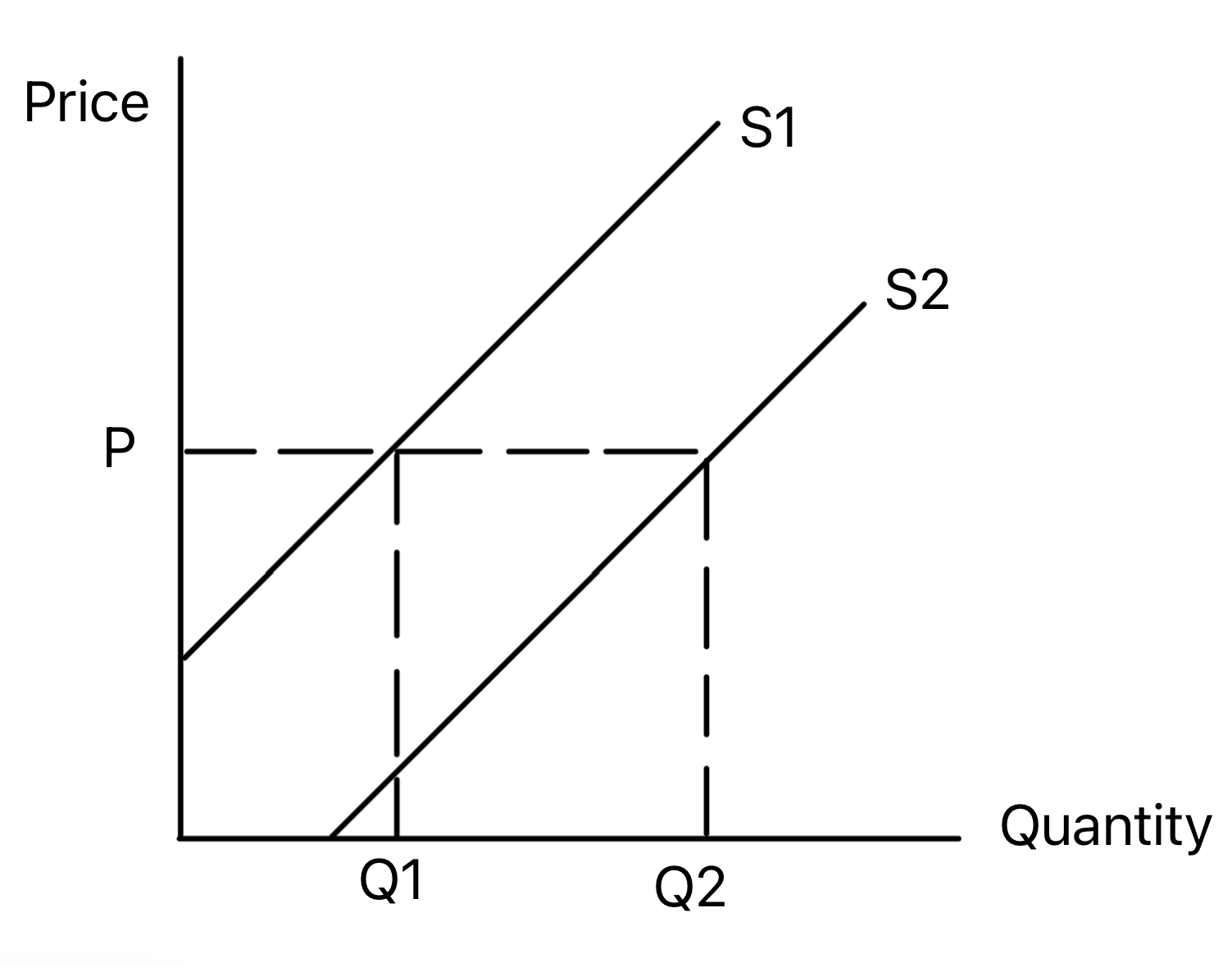

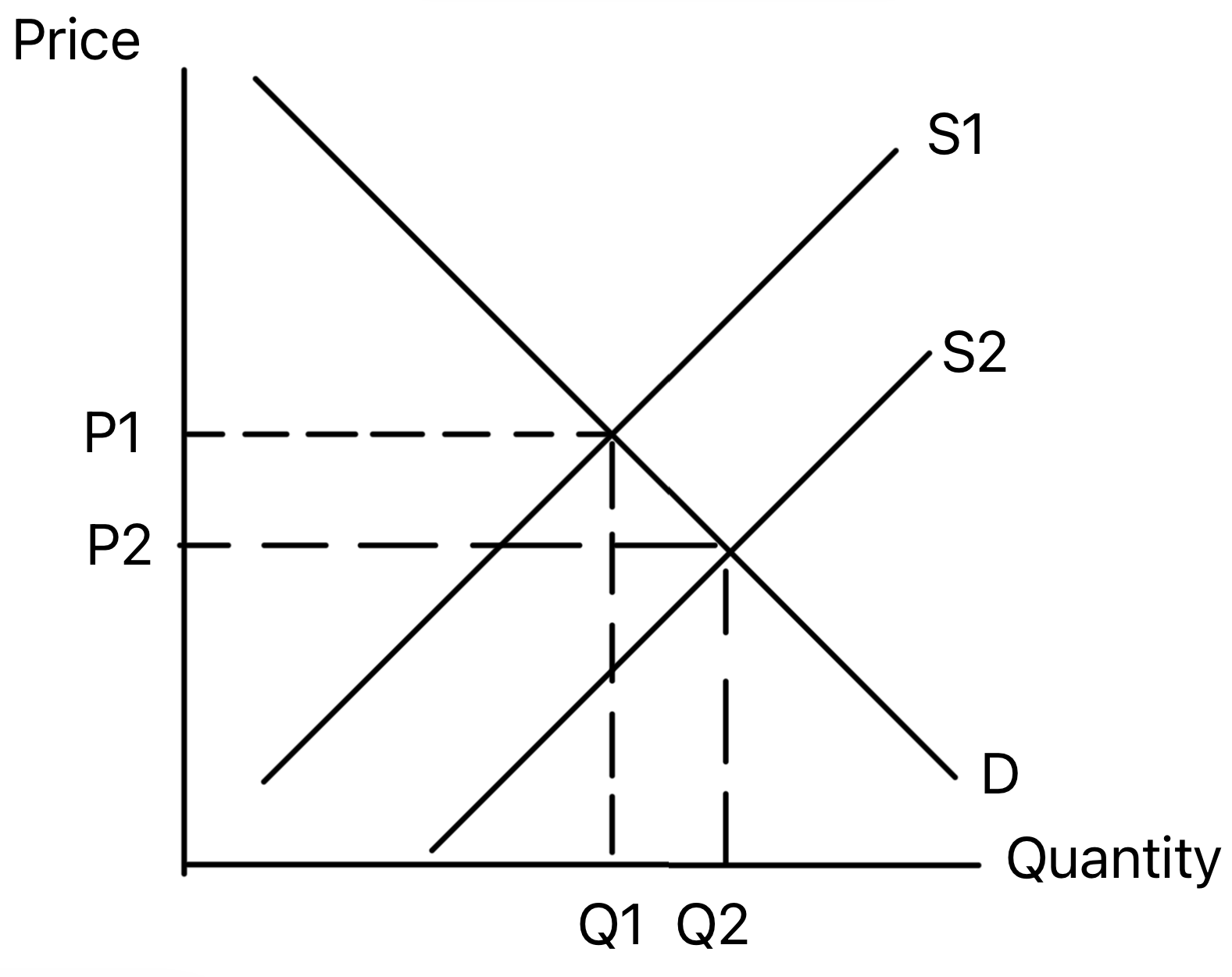

Shows supply shifting right, causing a lower equilibrium

price and higher quantity.

A rise in supply creates excess supply at the original

price. Price then falls, encouraging consumers to buy more

until the market reaches a new equilibrium.

Use in exams: Use it for lower costs,

productivity improvements, subsidies, new firms or improved

technology.

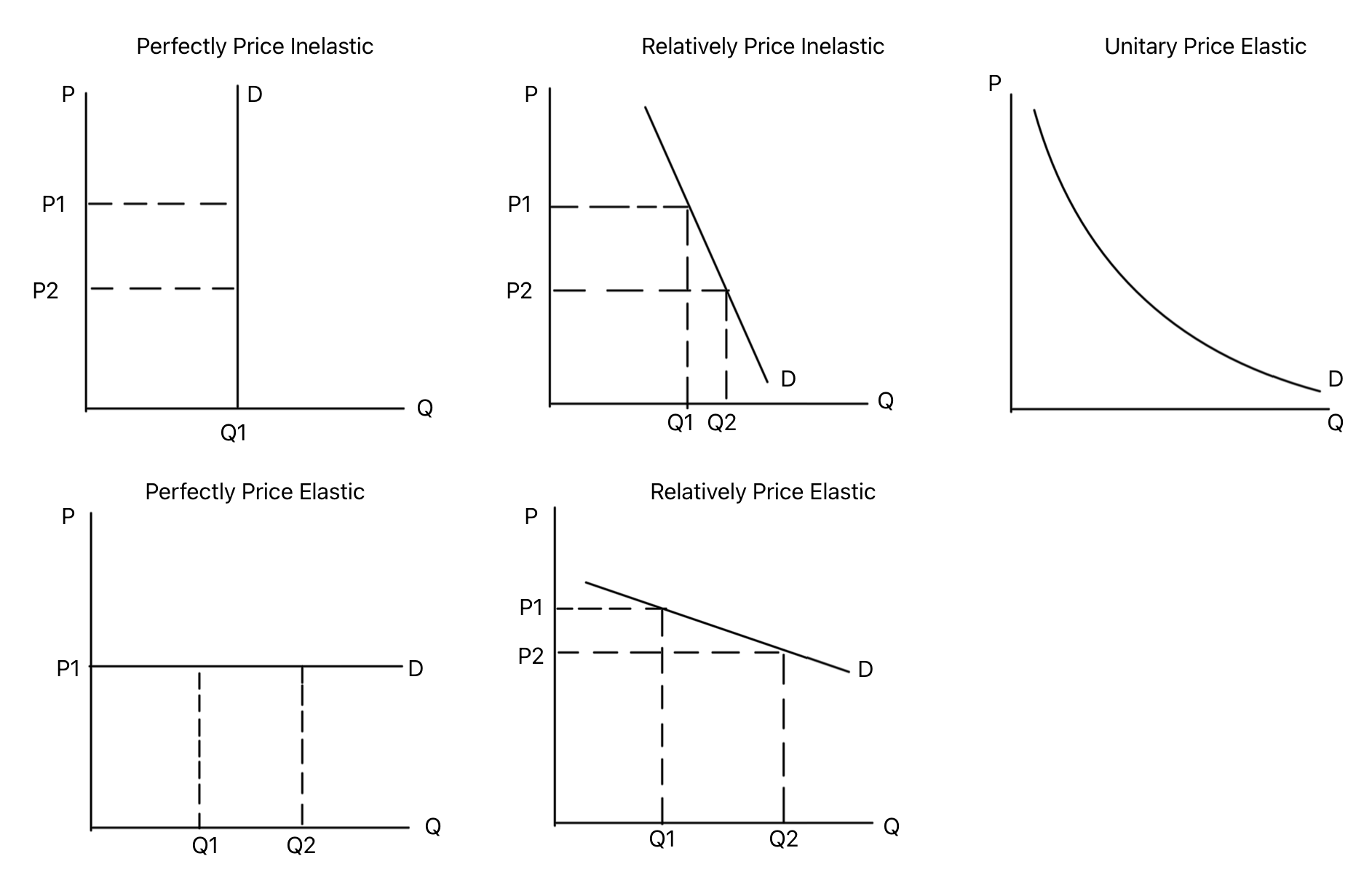

Shows how demand curve steepness relates to price

elasticity of demand.

Steeper demand curves are more price inelastic, while

flatter curves are more price elastic. Perfectly inelastic

demand is vertical, and perfectly elastic demand is

horizontal.

Use in exams: Use it when explaining the

effect of price changes, taxes or market power on revenue

and quantity demanded.

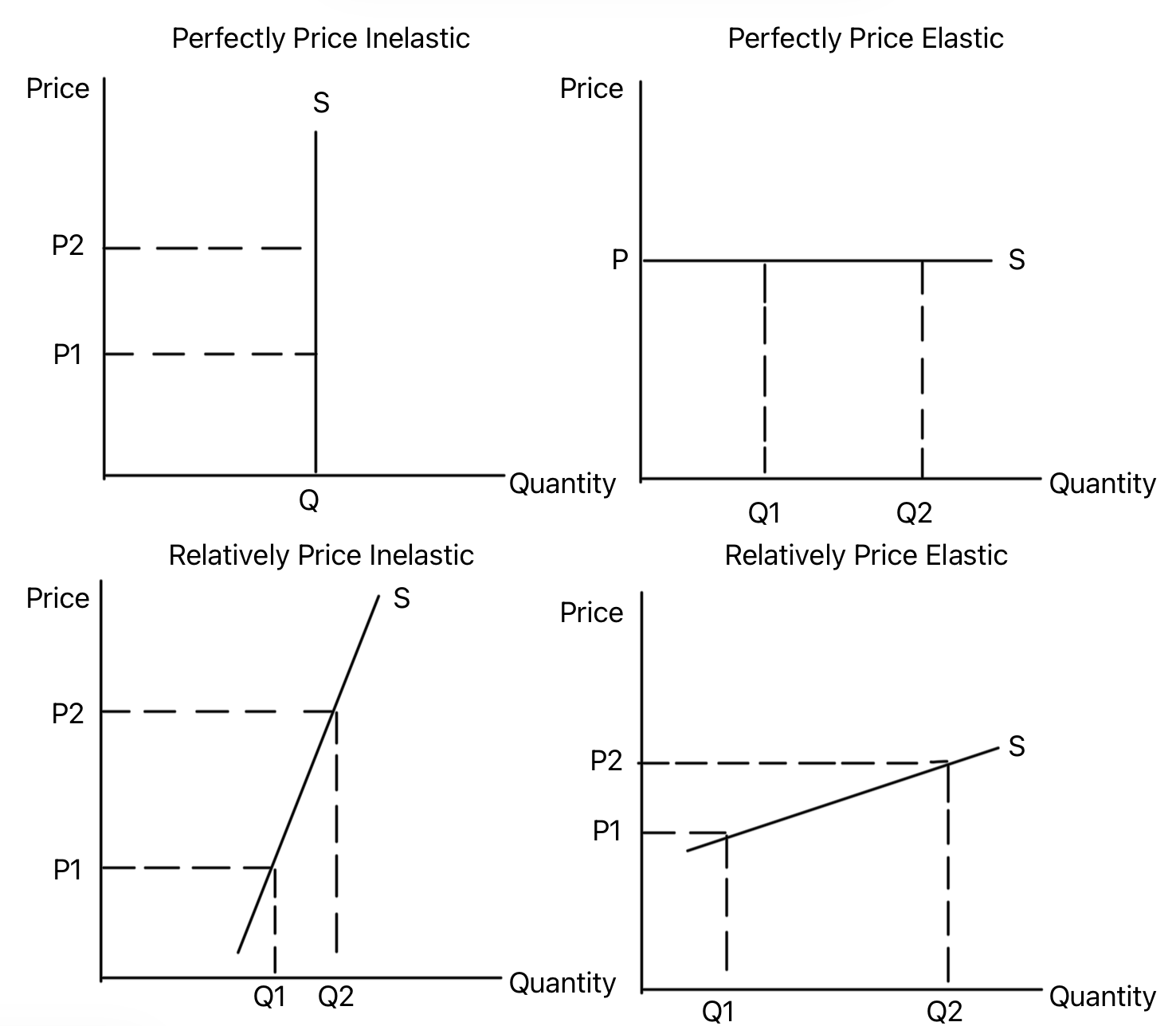

Shows how supply curve steepness relates to price

elasticity of supply.

Steeper supply curves are more price inelastic, while

flatter curves are more price elastic. Elasticity depends on

spare capacity, stock levels, production time and factor

mobility.

Use in exams: Use it when analysing how

quickly firms can respond to price changes or demand shocks.

Consumer Surplus, Producer Surplus, Taxes and Subsidies

Theme 11.2.8

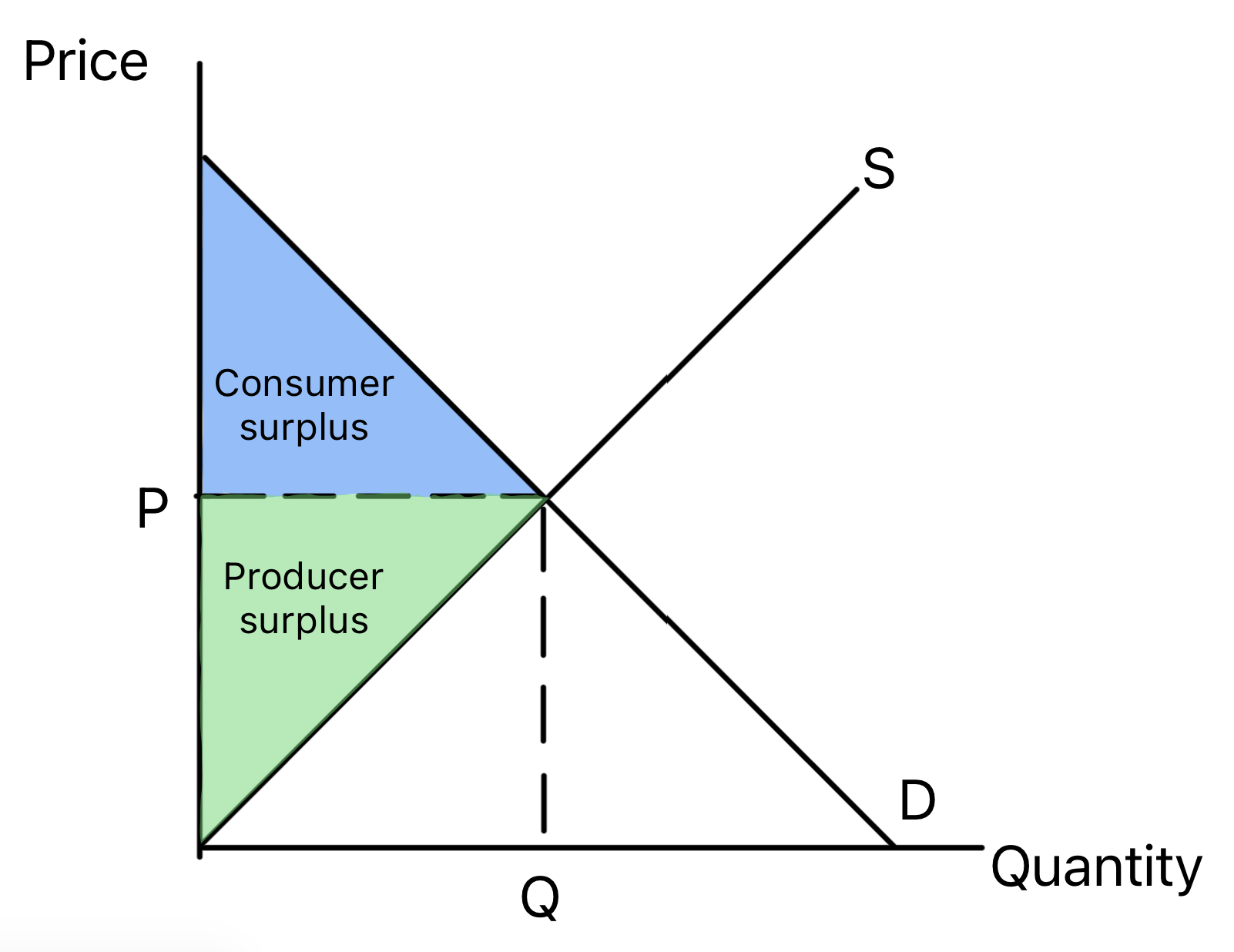

Consumer and Producer Surplus

Shows consumer surplus above the market price and producer

surplus below it.

Consumer surplus is the extra welfare buyers gain when they

pay less than they were willing to pay. Producer surplus is

the extra welfare sellers gain when they receive more than

the minimum they were willing to accept.

Use in exams: Use it to analyse welfare

changes, allocative efficiency and the impact of market

interventions.

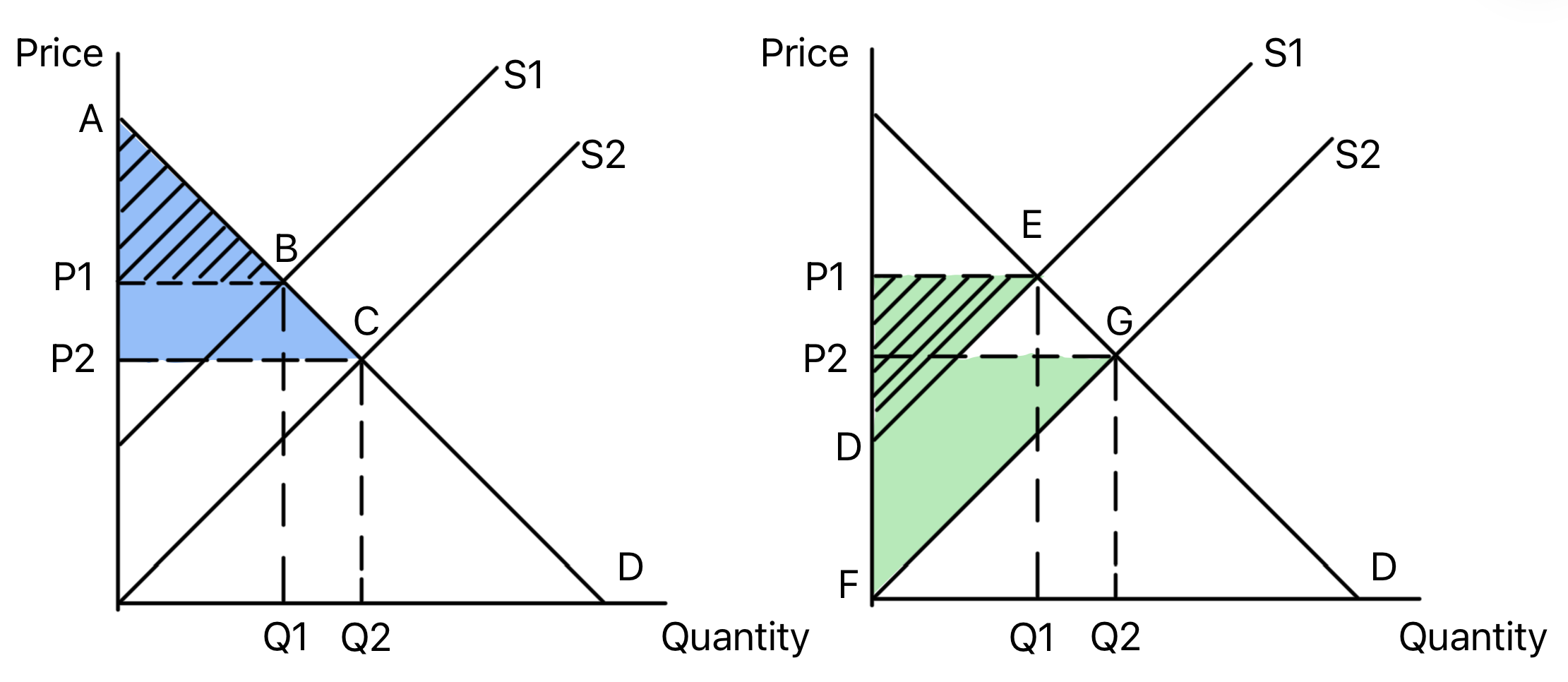

Shows how an outward shift of supply changes consumer and

producer surplus.

Higher supply lowers price and raises quantity. Consumer

surplus usually increases because consumers pay less and buy

more, while producer surplus changes depending on the size

of the price fall and quantity rise.

Use in exams: Use it for subsidies,

productivity improvements, lower input costs and welfare

analysis.

Shows how an outward shift of demand changes consumer and

producer surplus.

Higher demand raises price and quantity. Producer surplus

usually increases because firms sell more at a higher price,

while consumer surplus changes depending on the new price

and quantity.

Use in exams: Use it when a demand shock

changes welfare, such as a rise in incomes or consumer

confidence.

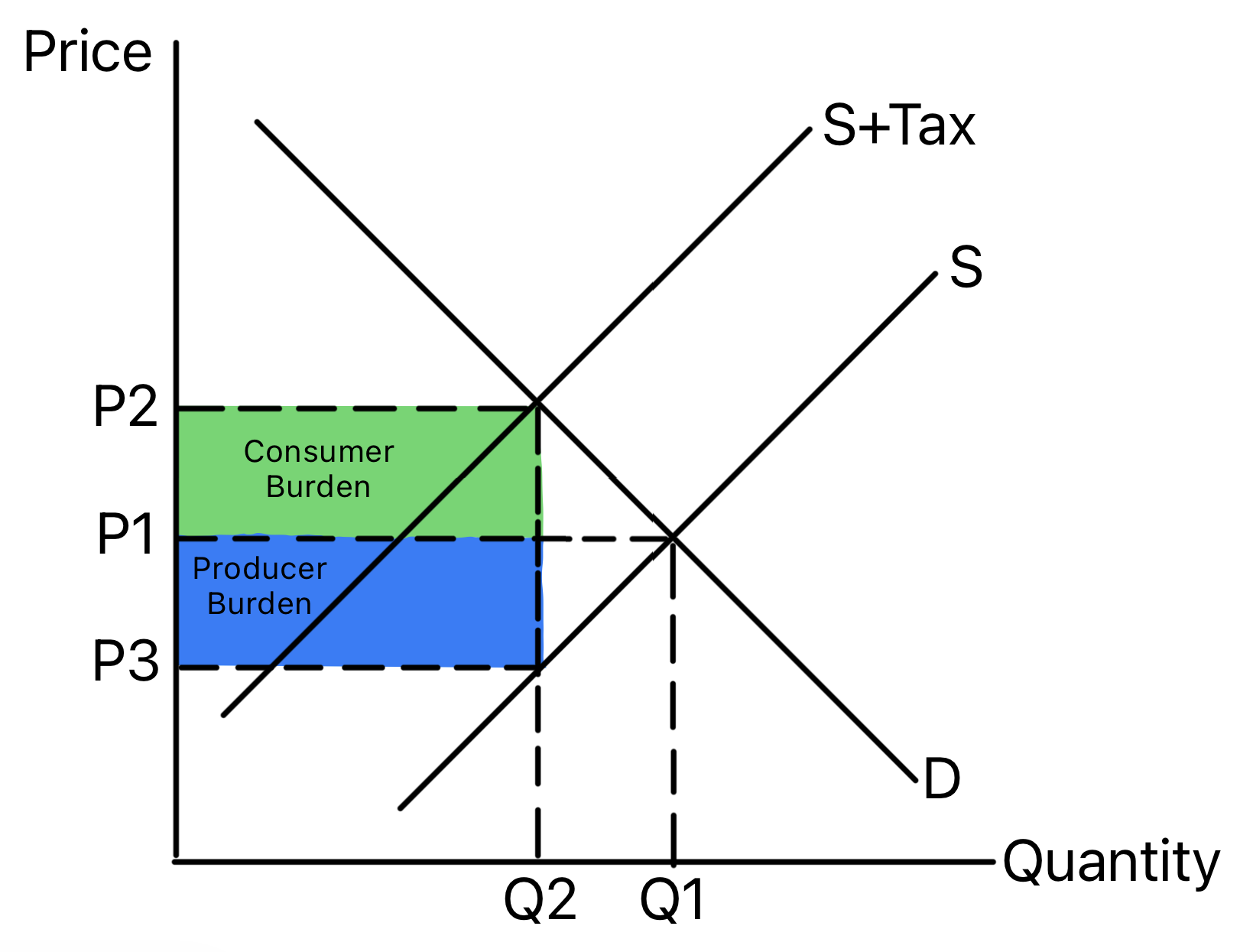

Shows a specific indirect tax shifting supply left and

raising the market price.

The vertical distance between the old and new supply curves

is the tax per unit. The tax burden is shared between

consumers and producers depending on the relative

elasticities of demand and supply.

Use in exams: Use it for taxes on goods

with external costs, demerit goods and government revenue.

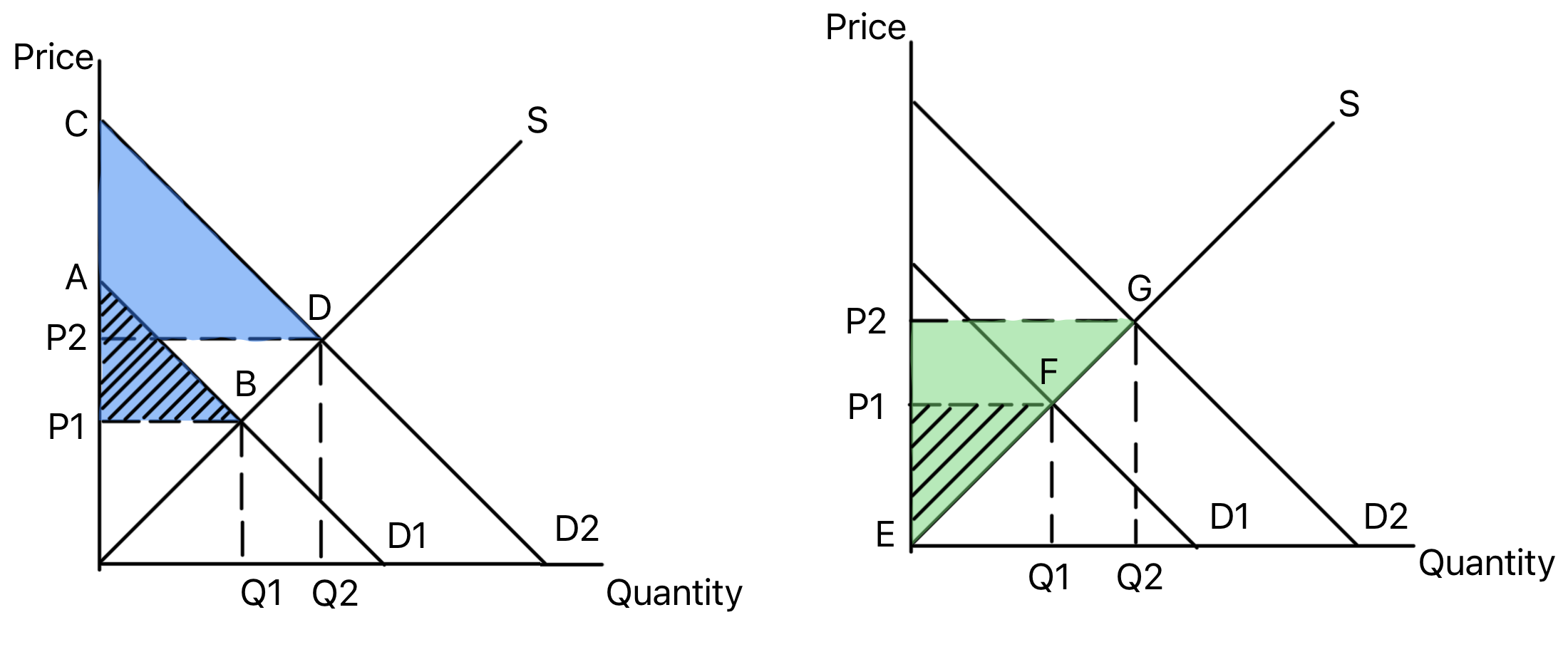

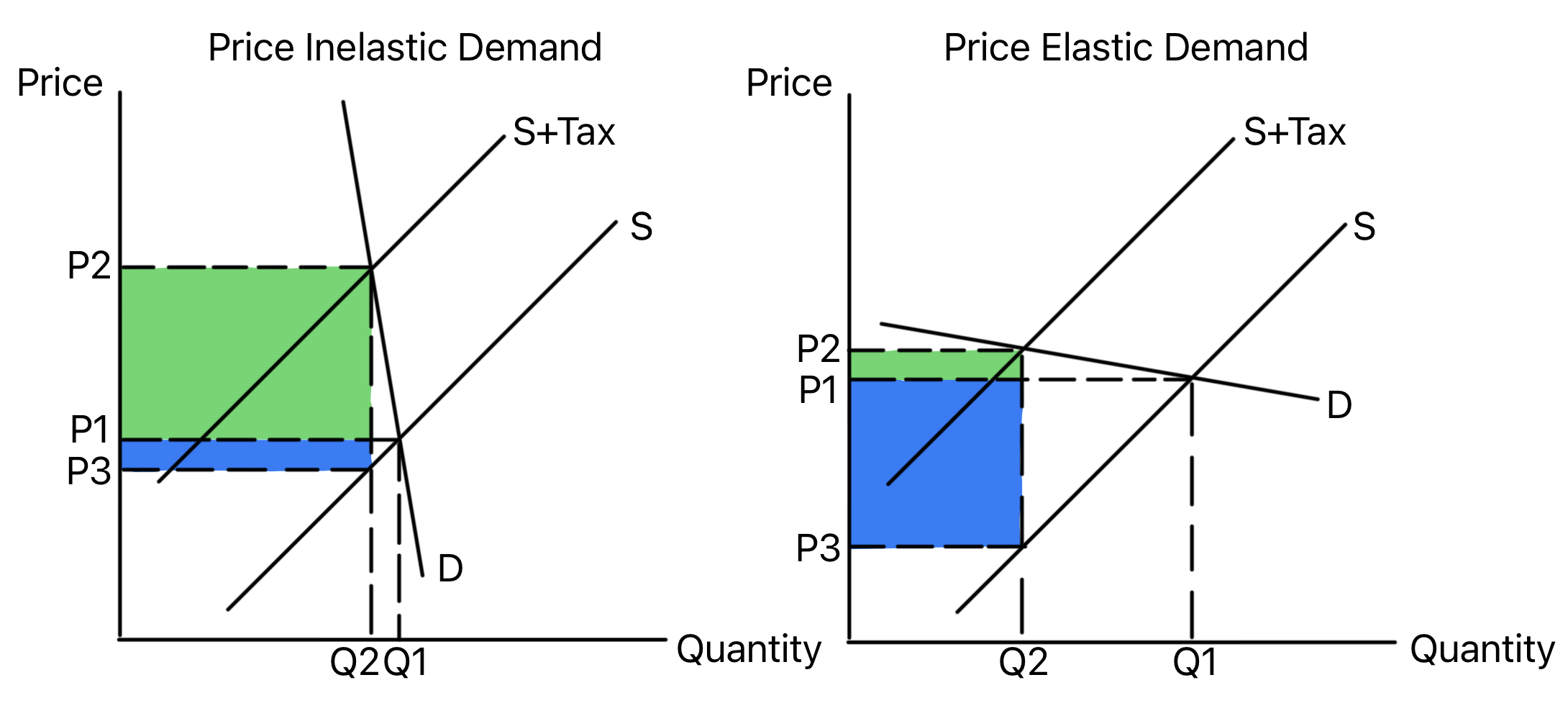

Compares the effect of an indirect tax when demand is

price inelastic and price elastic.

When demand is price inelastic, consumers bear more of the

tax and quantity falls by less. When demand is price

elastic, producers bear more of the tax and quantity falls

by more.

Use in exams: Use it to evaluate whether a

tax will reduce consumption or mainly raise revenue.

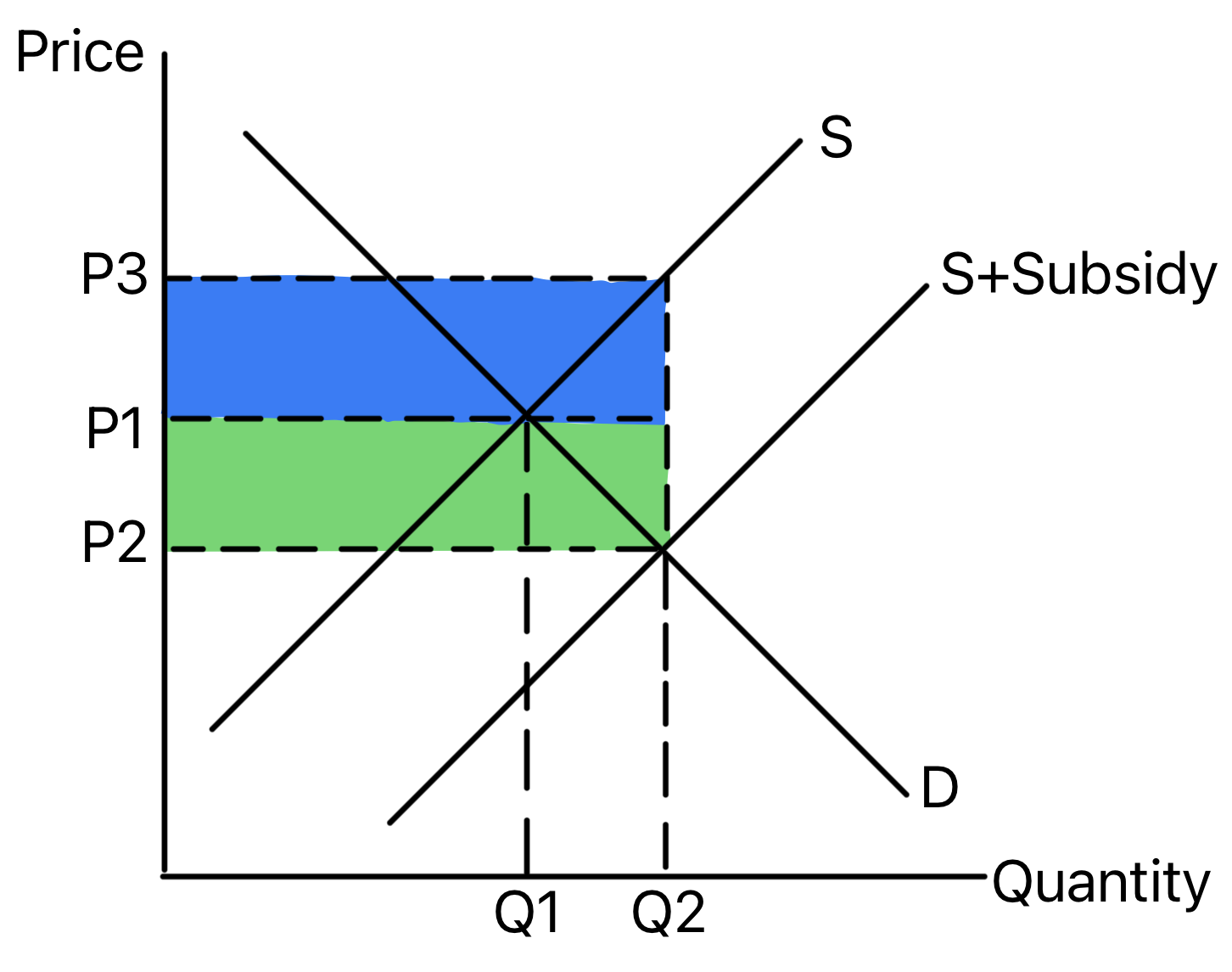

Shows a subsidy shifting supply right and lowering the

market price.

A subsidy reduces firms' costs, increasing supply. The

benefit is shared between consumers and producers depending

on relative elasticities, while government spending covers

the subsidy cost.

Use in exams: Use it for merit goods,

positive externalities and policies designed to increase

output.

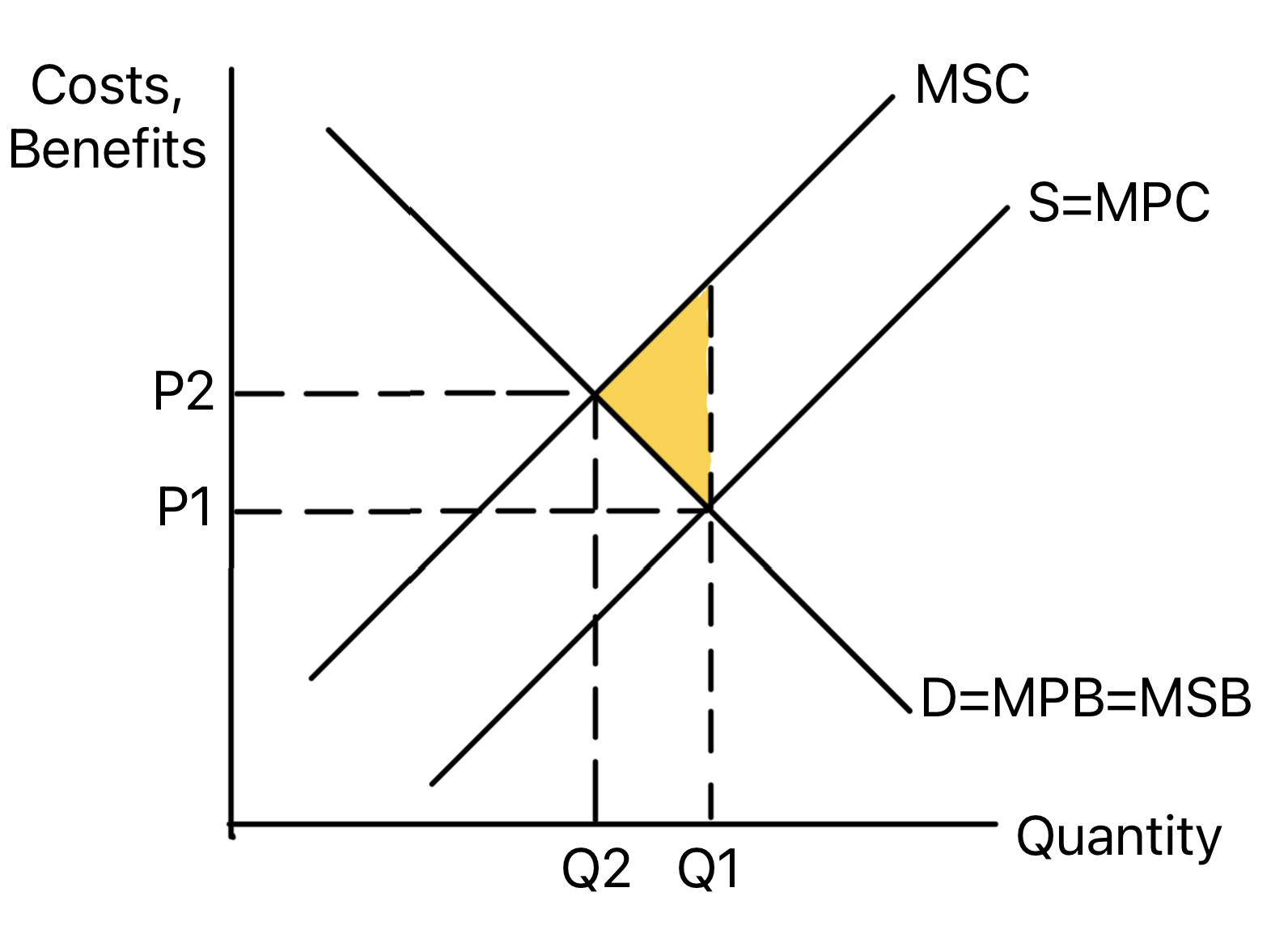

Consumers only consider private benefits, so marginal

private benefit is below marginal social benefit. The market

under-consumes the good relative to the social optimum.

Use in exams: Use it for merit goods,

education, healthcare, vaccination and subsidy arguments.

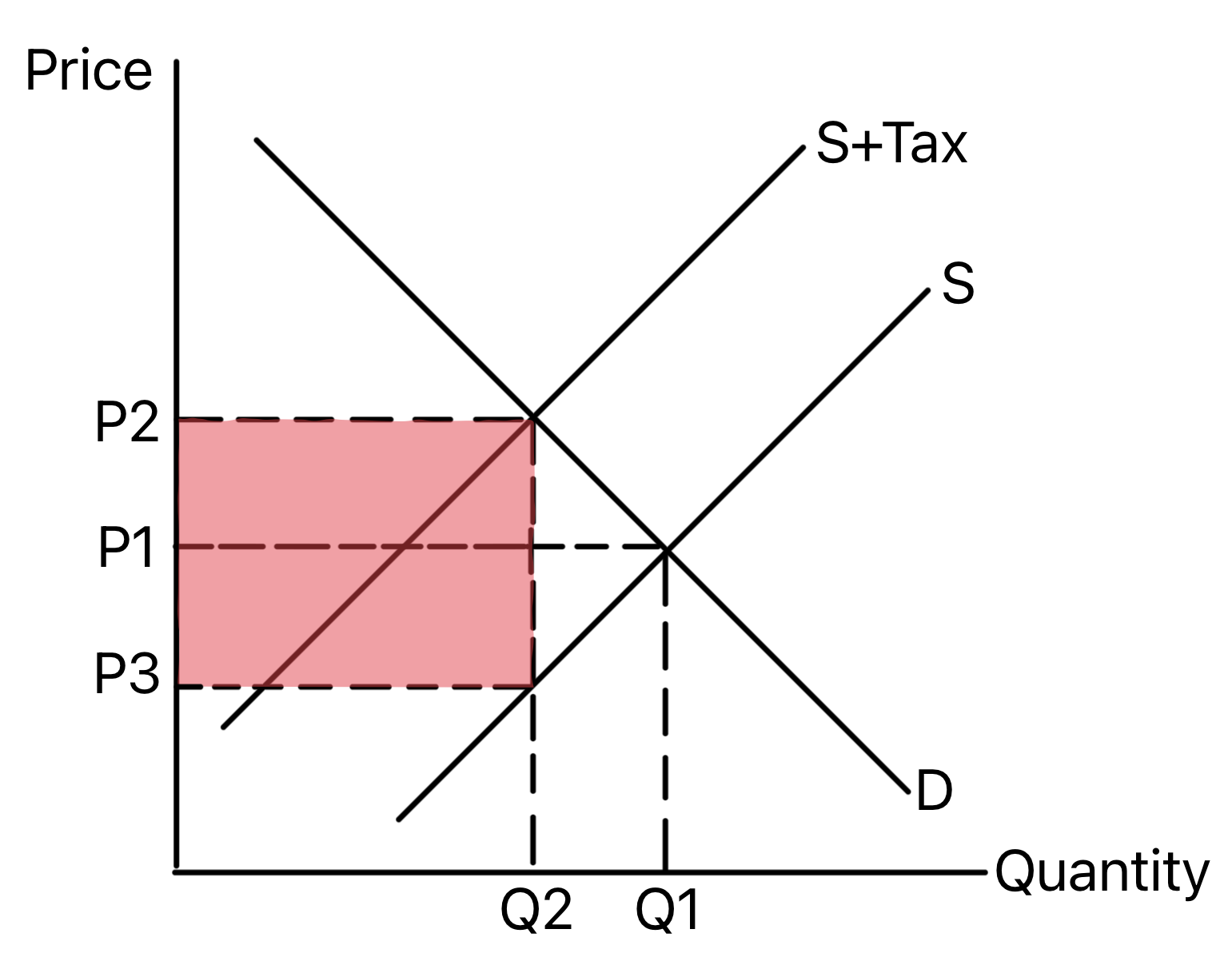

Shows how an indirect tax raises price, reduces quantity

and creates government revenue.

The tax shifts supply left and creates a gap between the

price consumers pay and the price producers receive. The tax

per unit multiplied by the new quantity gives government

revenue.

Use in exams: Use it to analyse demerit

goods, external costs and the trade-off between revenue and

lower consumption.

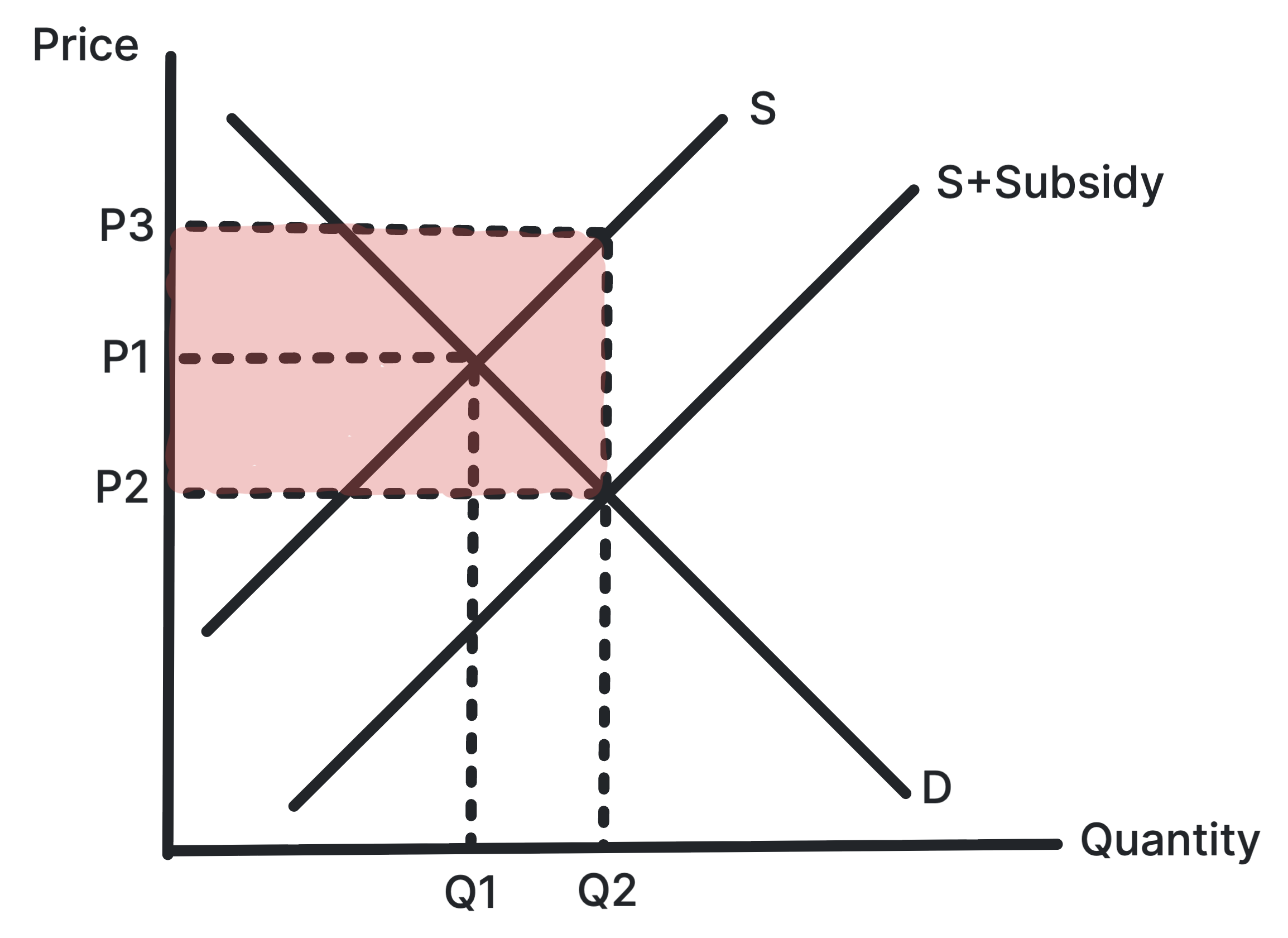

Shows how a subsidy lowers price, raises quantity and

creates a cost to government.

The subsidy shifts supply right and creates a gap between

the price consumers pay and the price producers receive. The

subsidy per unit multiplied by the new quantity gives total

government expenditure.

Use in exams: Use it for merit goods,

positive externalities, affordability and intervention

costs.

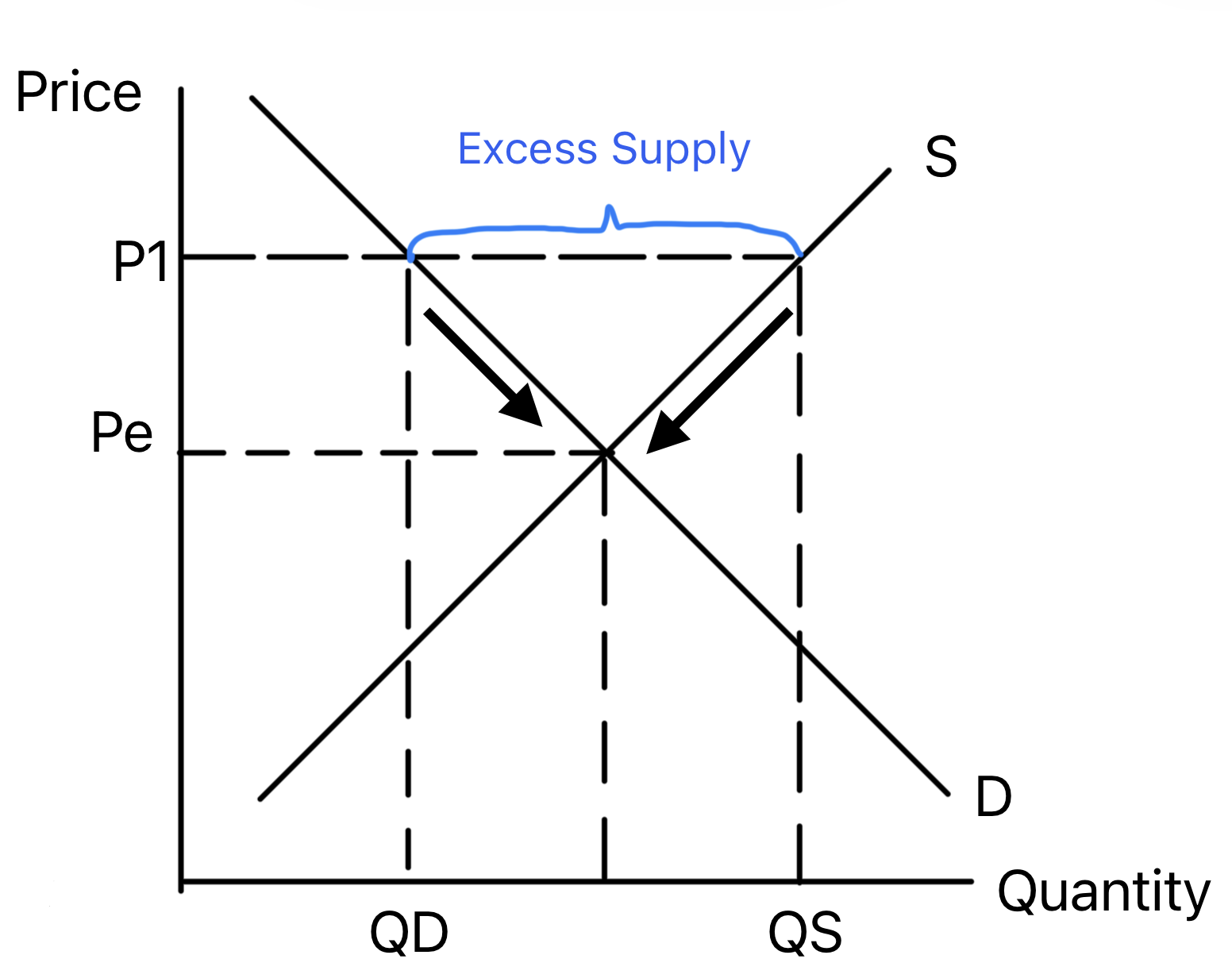

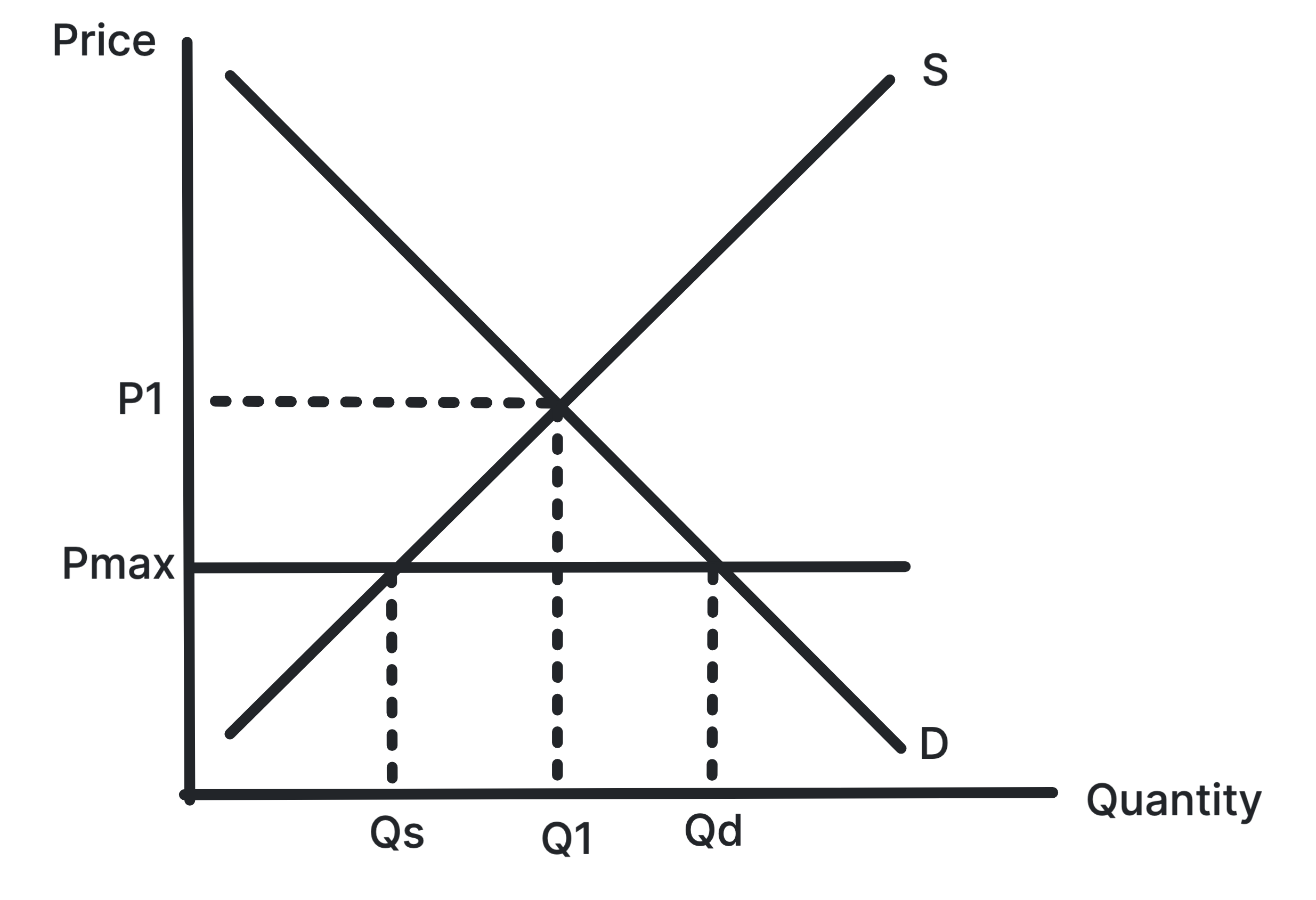

Shows a price floor above equilibrium creating excess

supply.

A minimum price is only effective if it is set above the

market equilibrium. It can raise producer incomes or reduce

consumption but creates a surplus.

Use in exams: Use it for agricultural

prices, alcohol pricing, labour markets and intervention

evaluation.

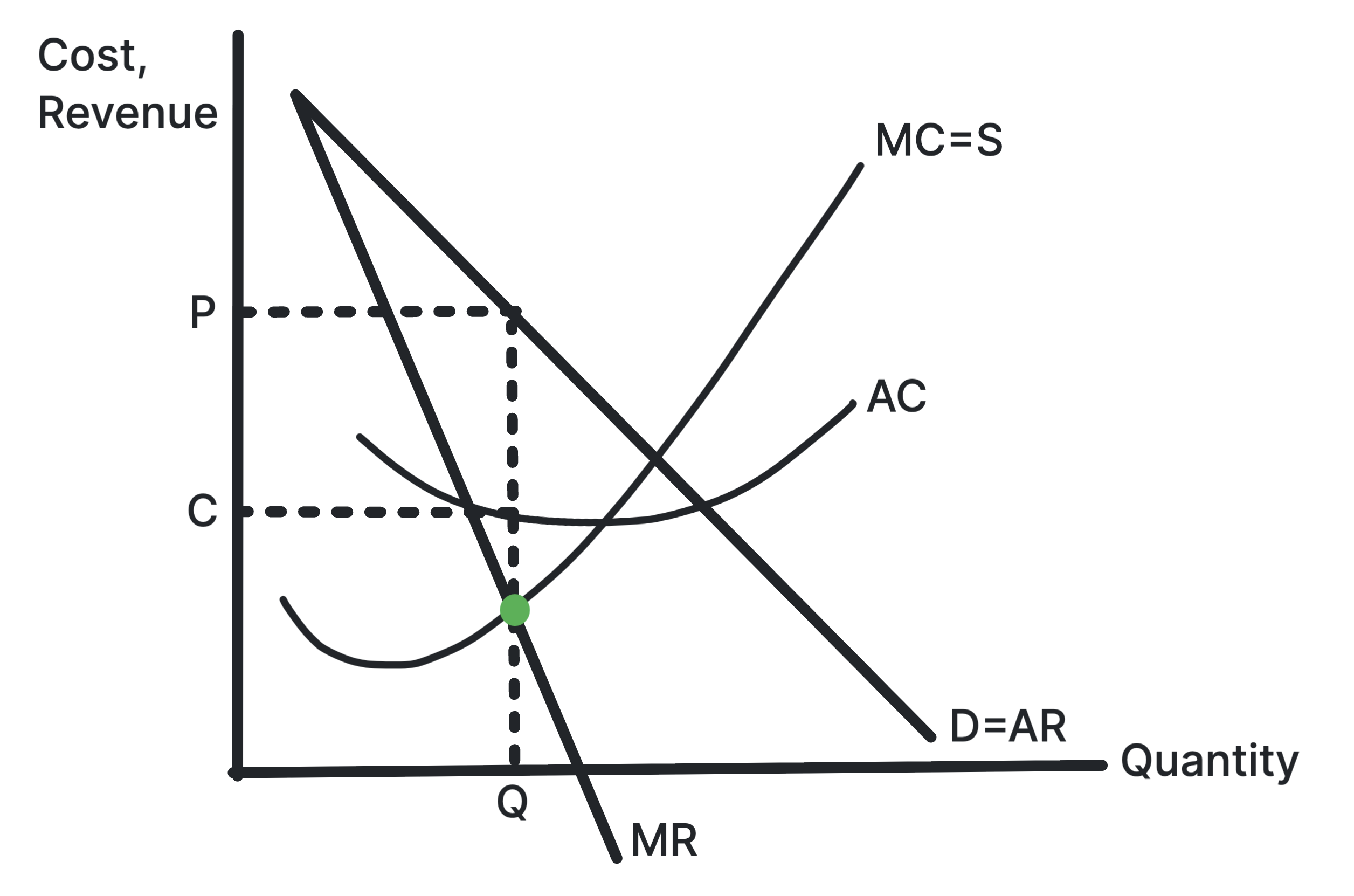

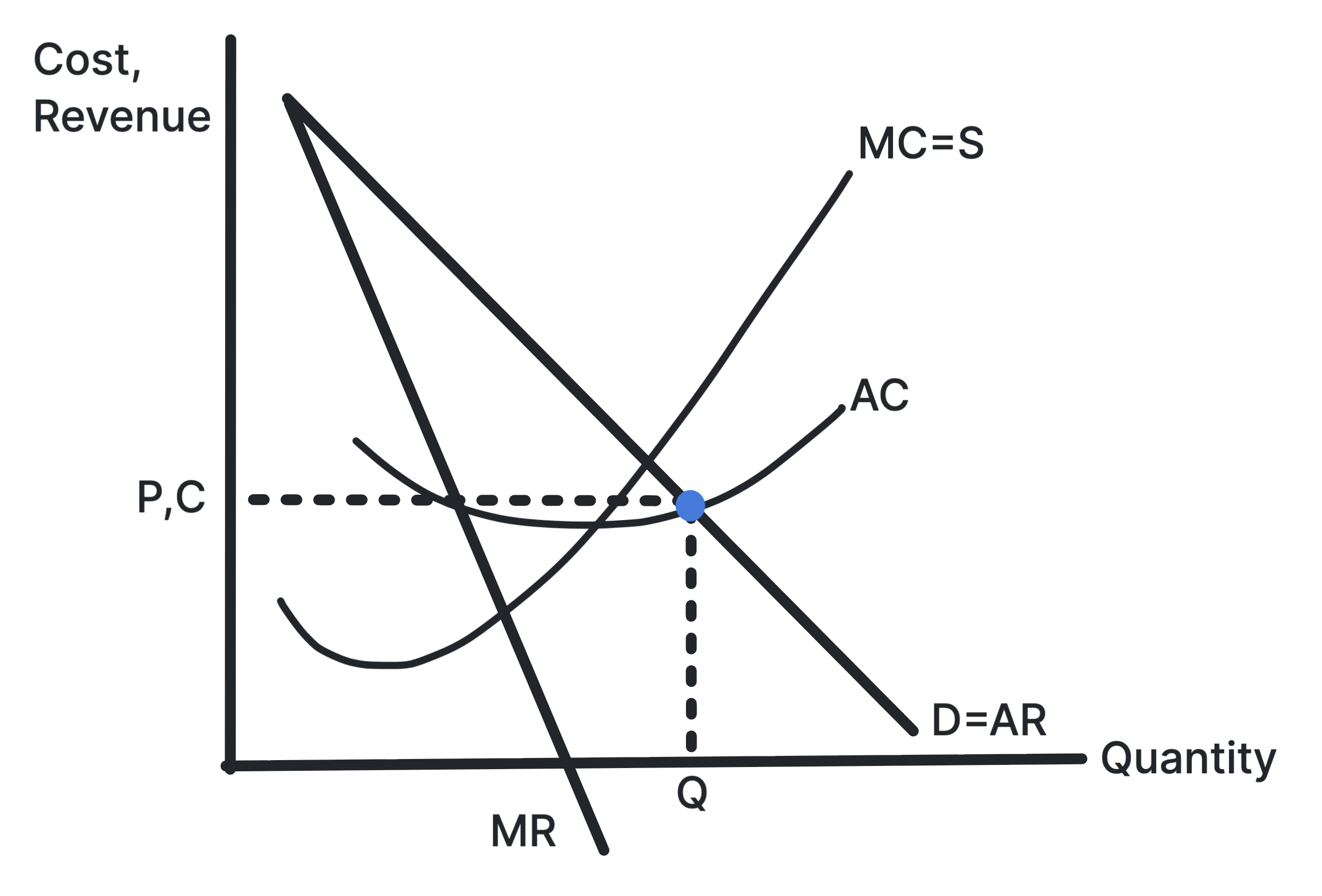

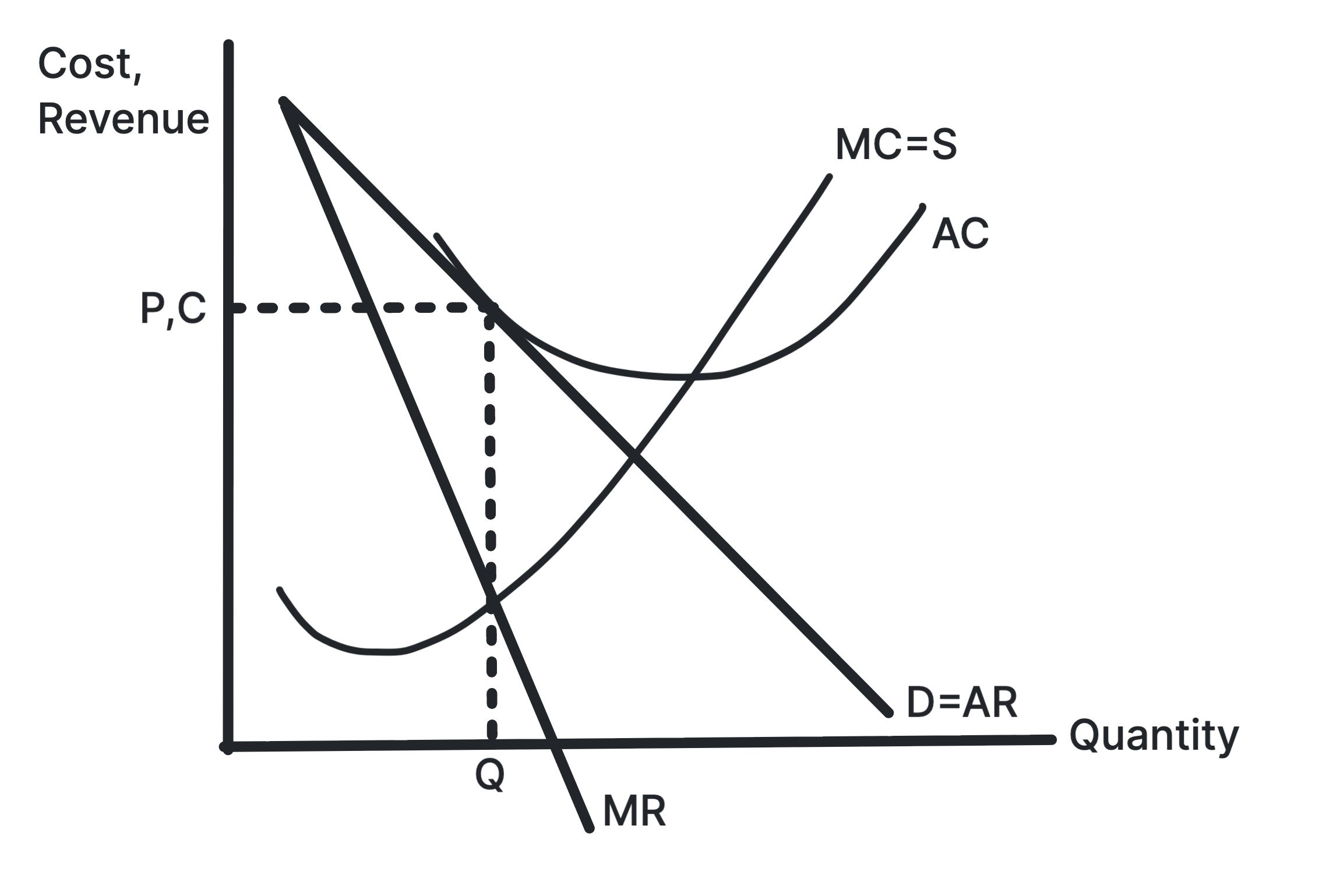

Profit is maximised at the output where the extra cost of

producing one more unit equals the extra revenue from

selling it. Price is then read from the AR curve.

Use in exams: Use it when comparing profit

maximisation with revenue maximisation, sales maximisation

or satisficing.

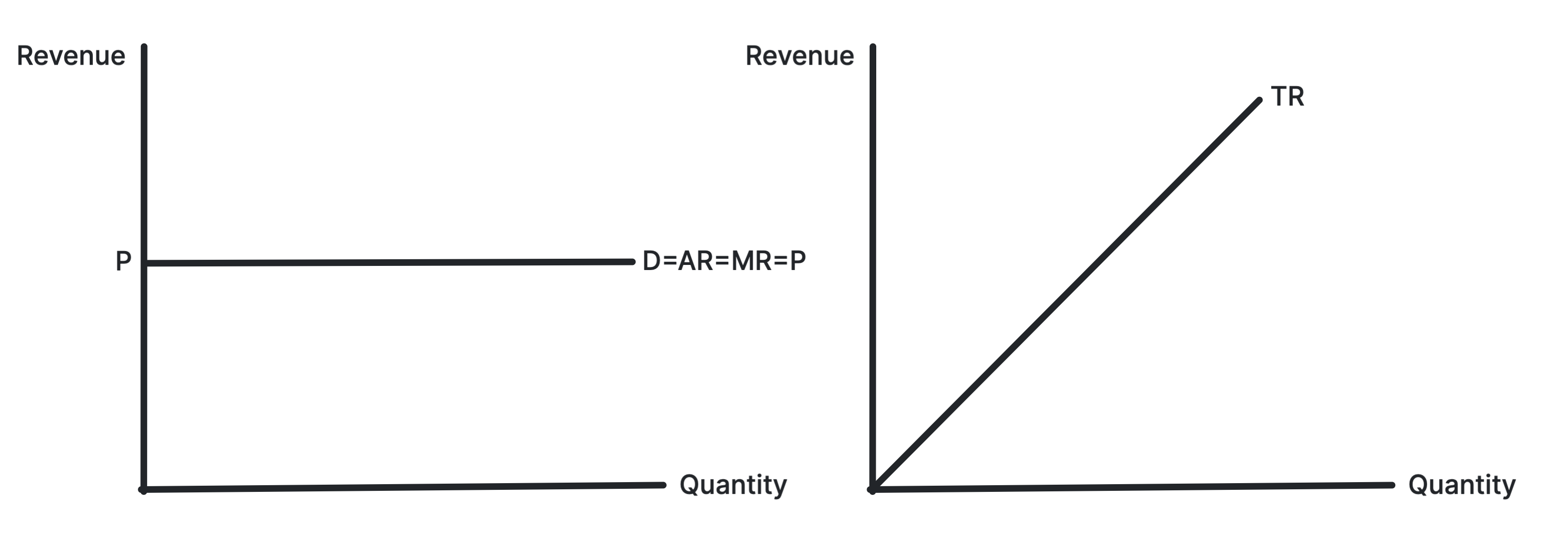

Shows AR and MR as horizontal at the market price.

A perfectly competitive firm is a price taker, so each extra

unit is sold at the same price. This makes AR equal to MR,

and total revenue rises at a constant rate.

Use in exams: Use it when explaining why

individual firms in perfect competition face perfectly

elastic demand.

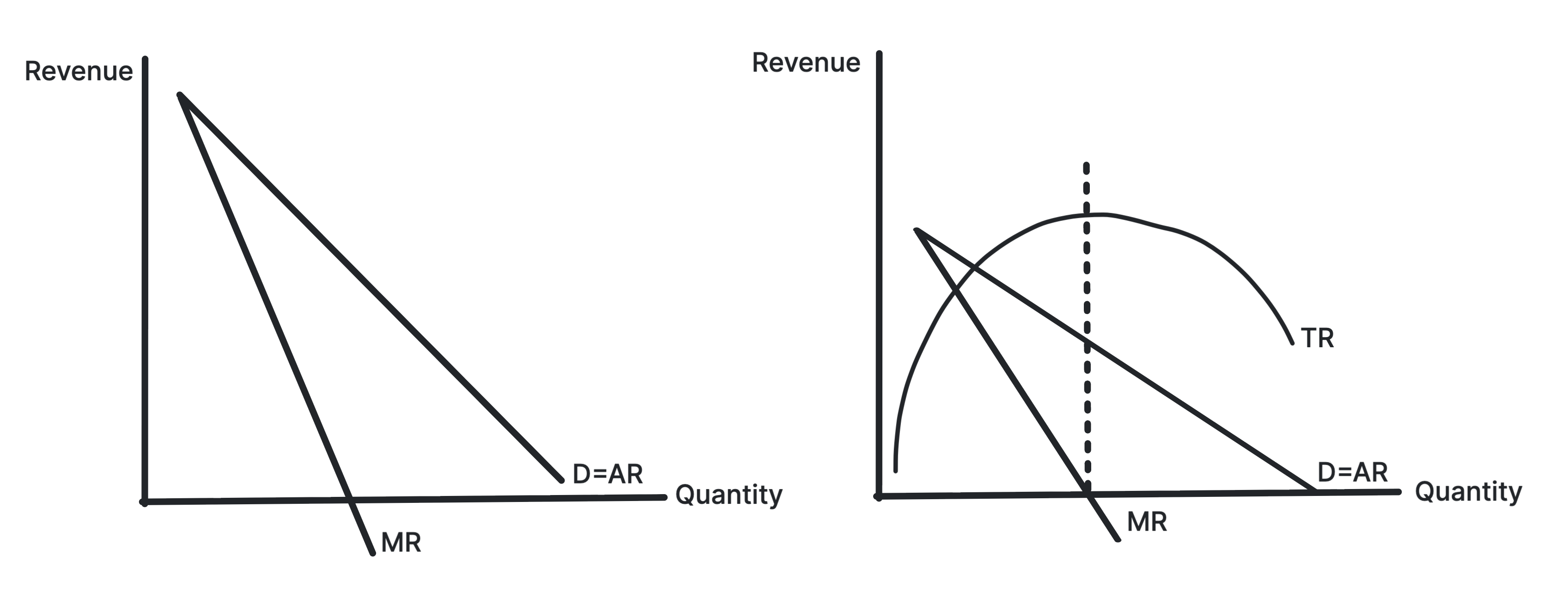

A firm with market power must lower price to sell more

output. Marginal revenue lies below average revenue because

extra sales reduce the price on previous units.

Use in exams: Use it for monopoly,

oligopoly and monopolistic competition diagrams.

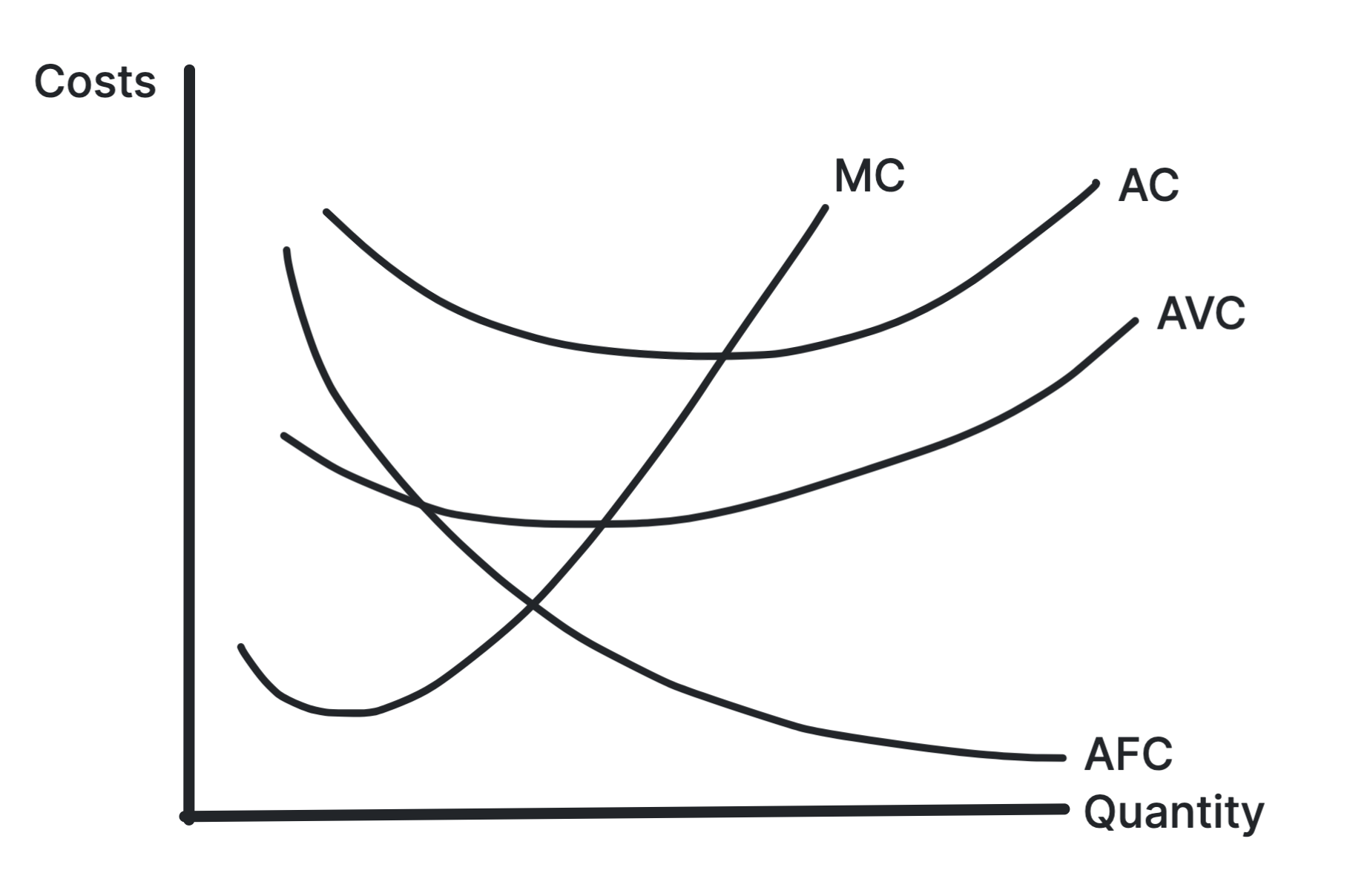

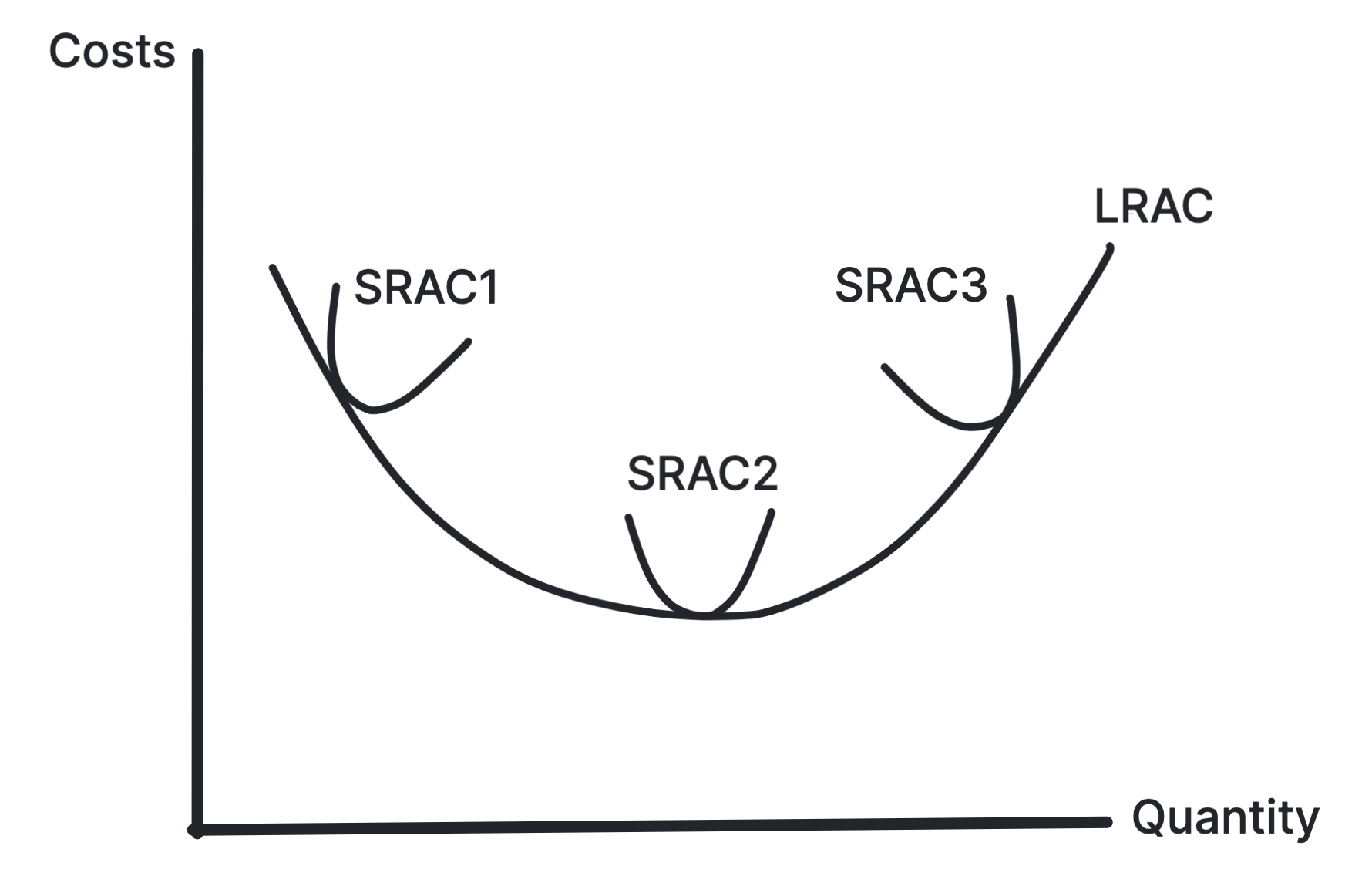

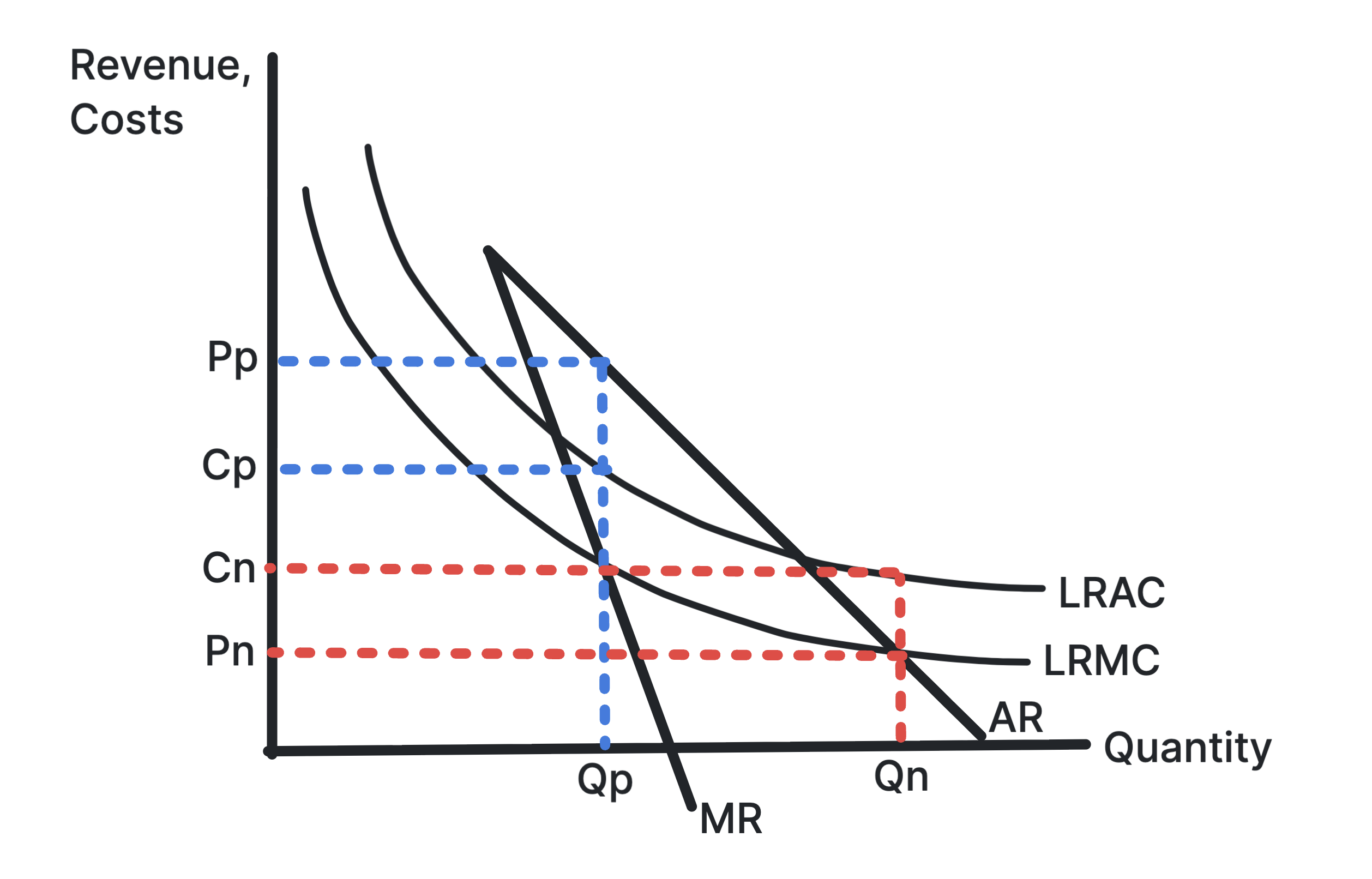

Shows how long-run average cost changes as the firm

expands its scale.

The LRAC curve falls when economies of scale dominate and

rises when diseconomies of scale dominate. The minimum point

shows the lowest average cost attainable in the long run.

Use in exams: Use it for economies of

scale, diseconomies of scale, natural monopoly and minimum

efficient scale.

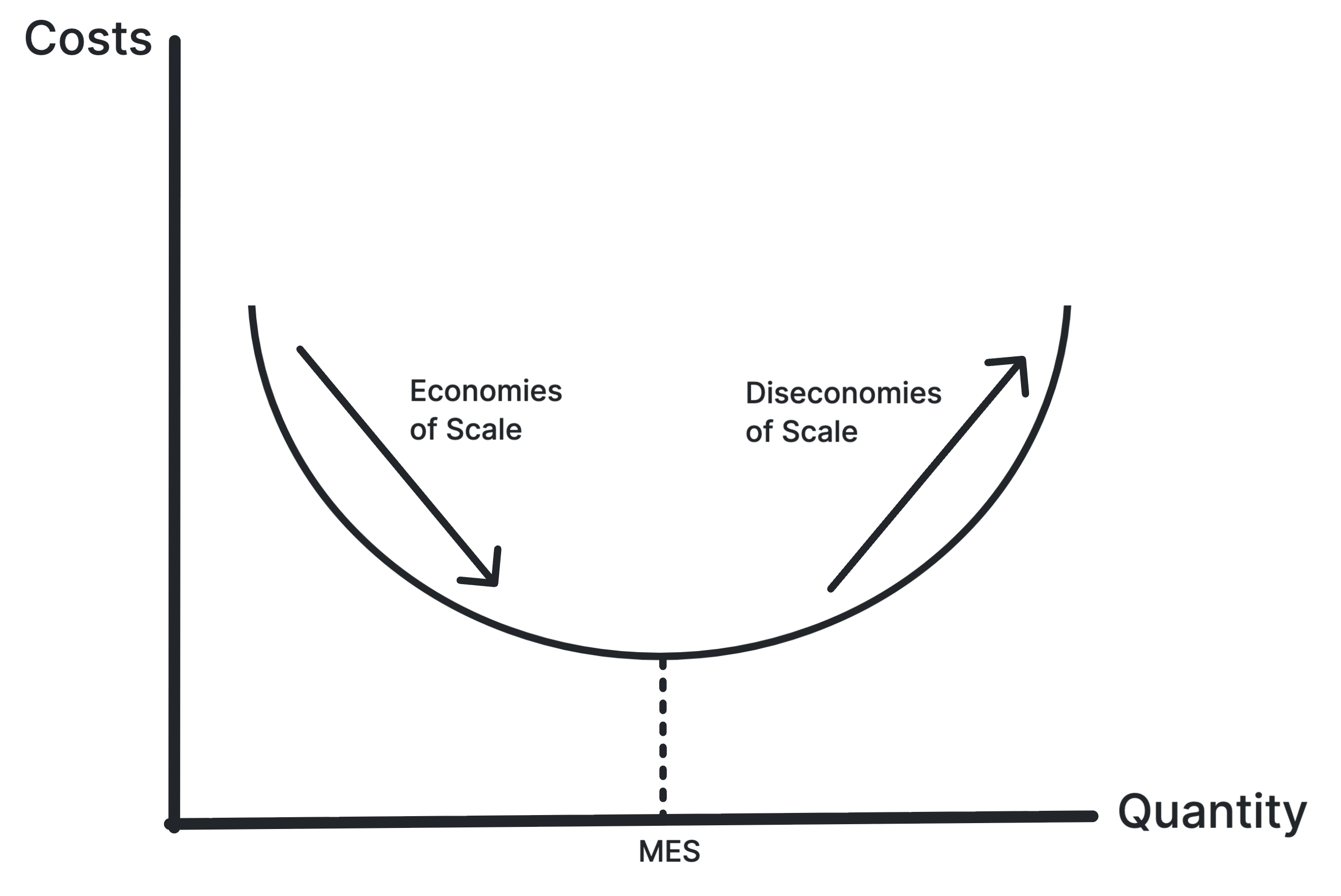

Shows the falling and rising sections of LRAC and the

minimum efficient scale.

As output expands, average costs may fall because of

purchasing, technical, financial, managerial, marketing or

risk-bearing economies. Beyond the efficient scale,

diseconomies can push LRAC upward.

Use in exams: Use it for business growth,

market concentration, barriers to entry and natural

monopoly.

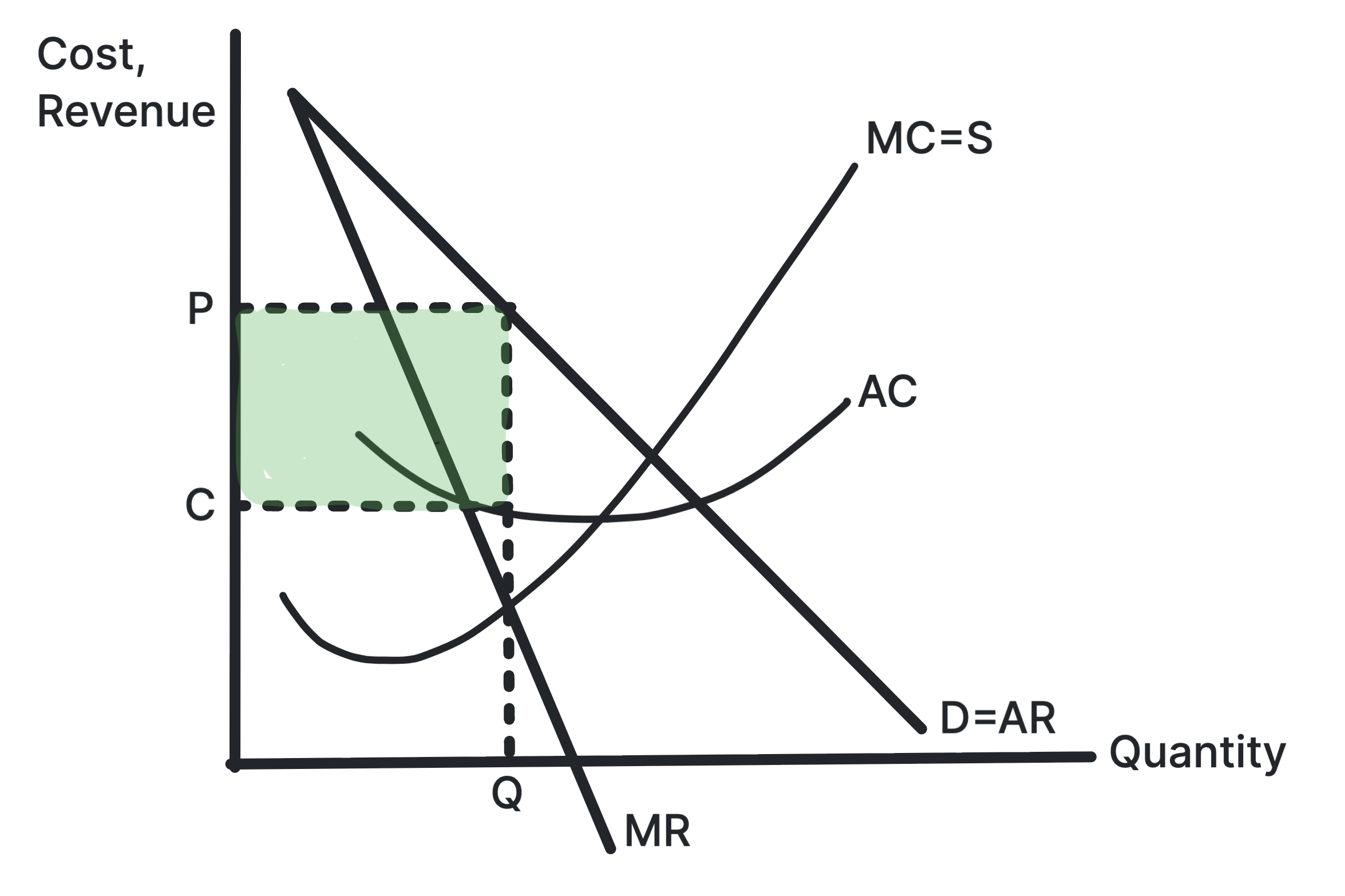

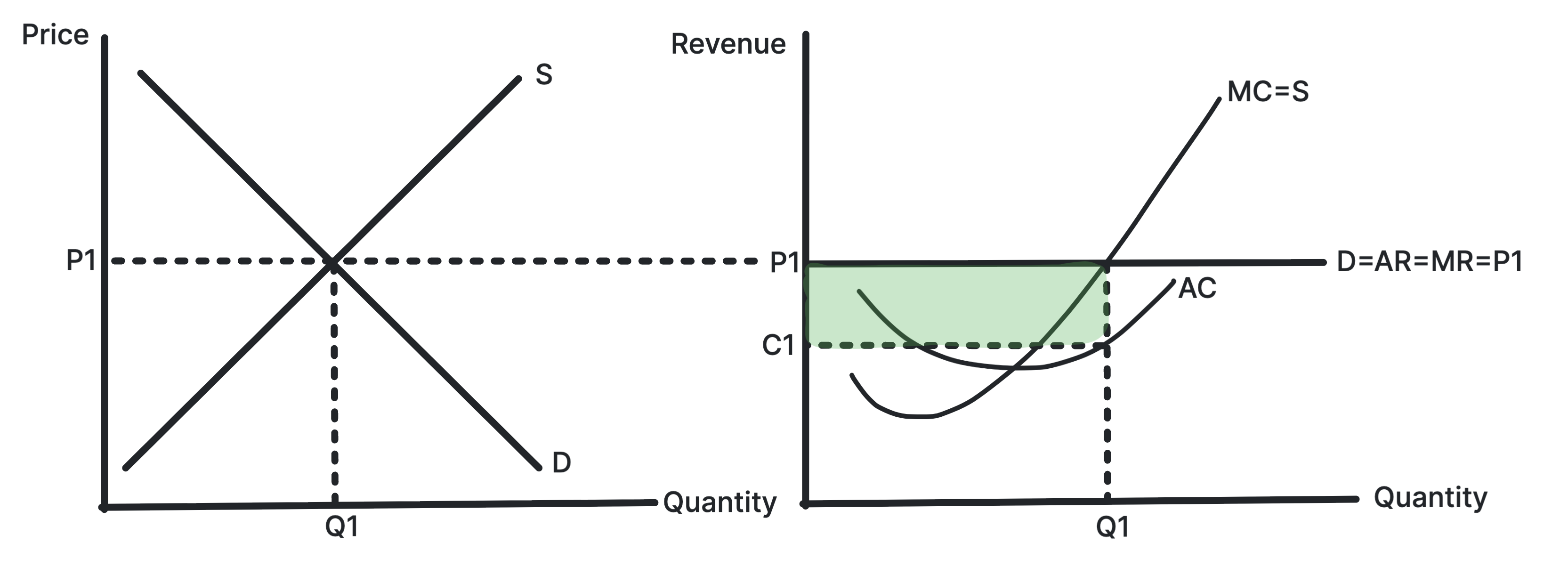

Shows profit where AR is above AC at the profit-maximising

output.

The firm produces where MC equals MR, then charges the price

on the AR curve. If price exceeds average cost at that

output, the shaded rectangle represents supernormal profit.

Use in exams: Use it for monopoly,

monopolistic competition, short-run perfect competition and

barriers to entry.

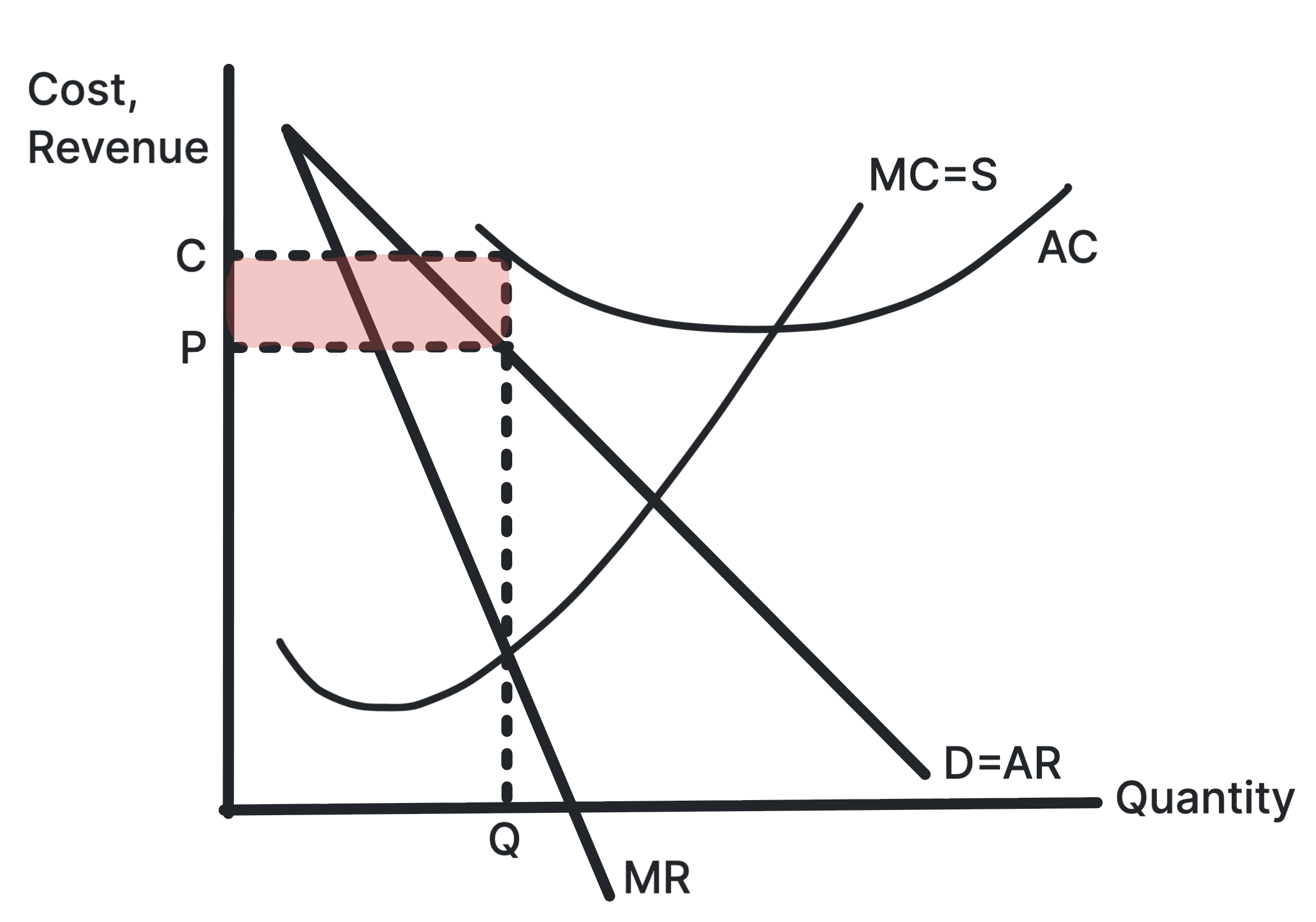

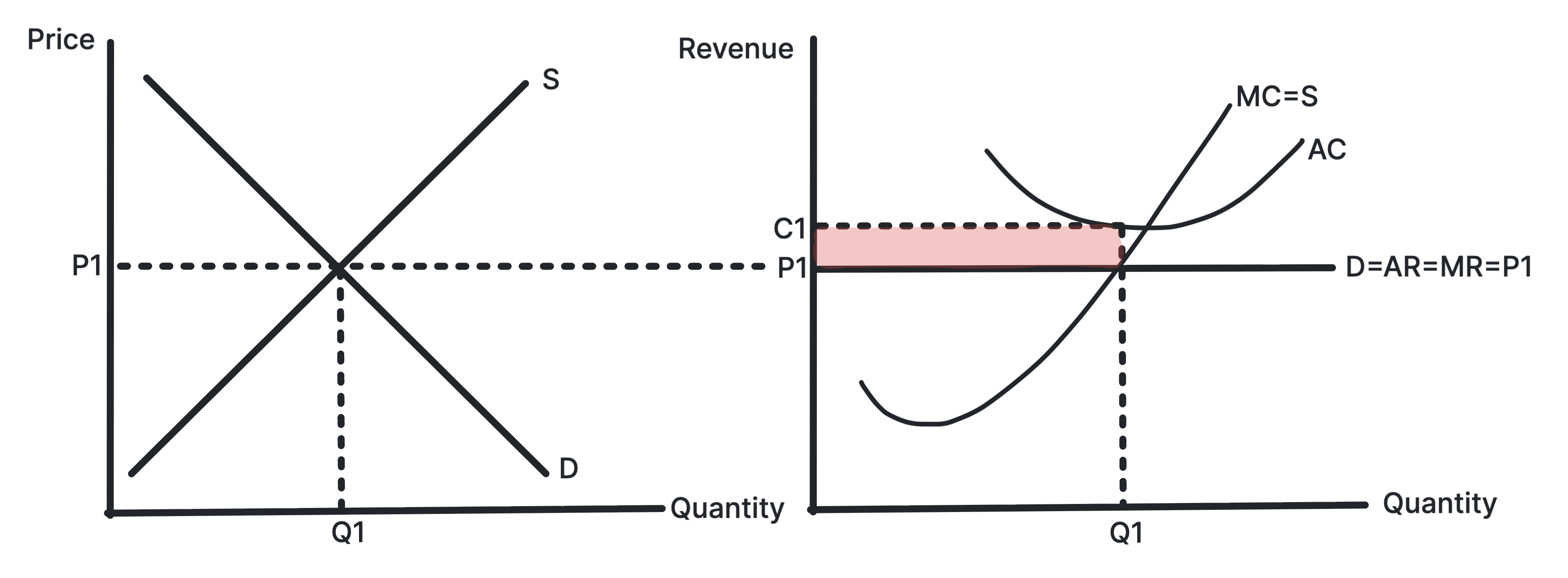

Shows a loss where AR is below AC at the profit-maximising

output.

The firm still produces where MC equals MR, but the price

from AR is below average cost. The shaded rectangle shows

the loss per unit multiplied by output.

Use in exams: Use it for short-run losses,

market exit and the adjustment process in perfect

competition.

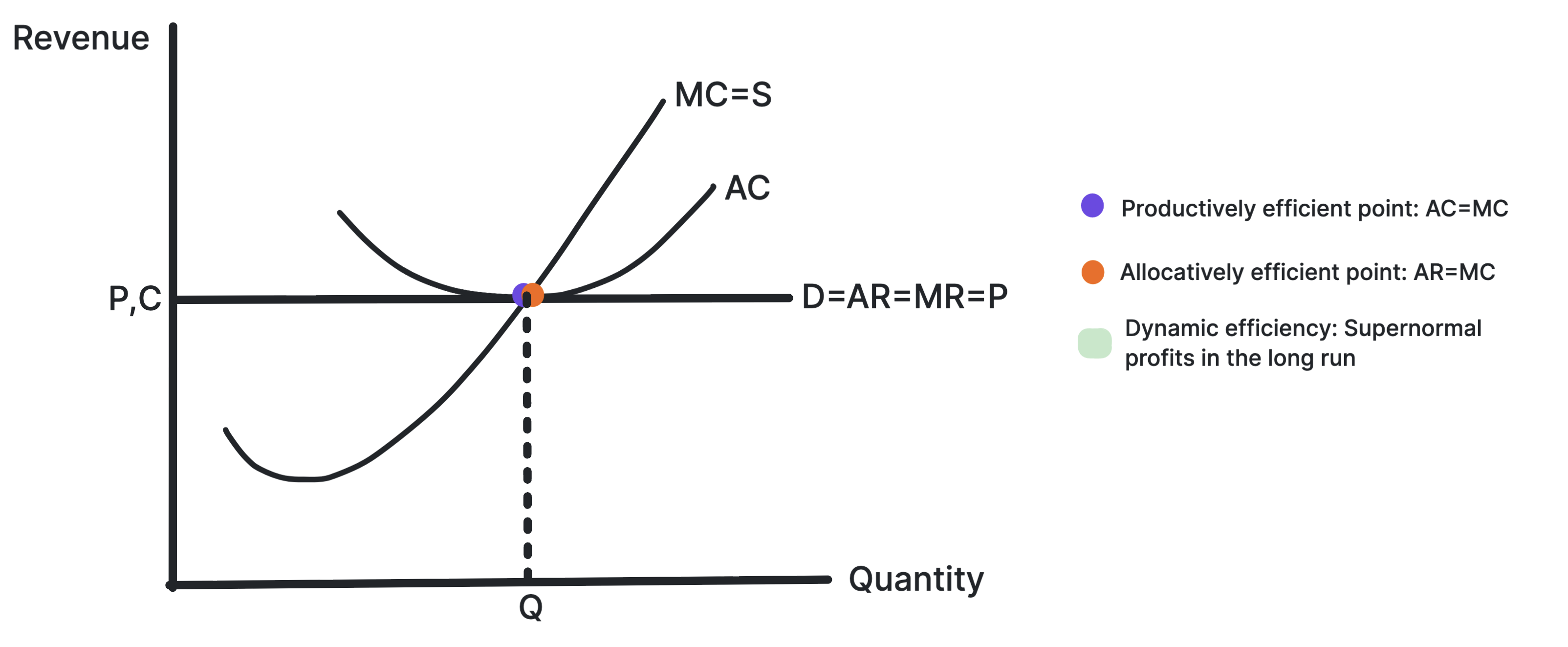

Shows P equals MC and production at the minimum point of

AC.

In long-run perfect competition, firms produce at the lowest

average cost and price equals marginal cost. This gives

productive and allocative efficiency, but not necessarily

dynamic efficiency.

Use in exams: Use it when comparing market

structures and judging whether consumers benefit.

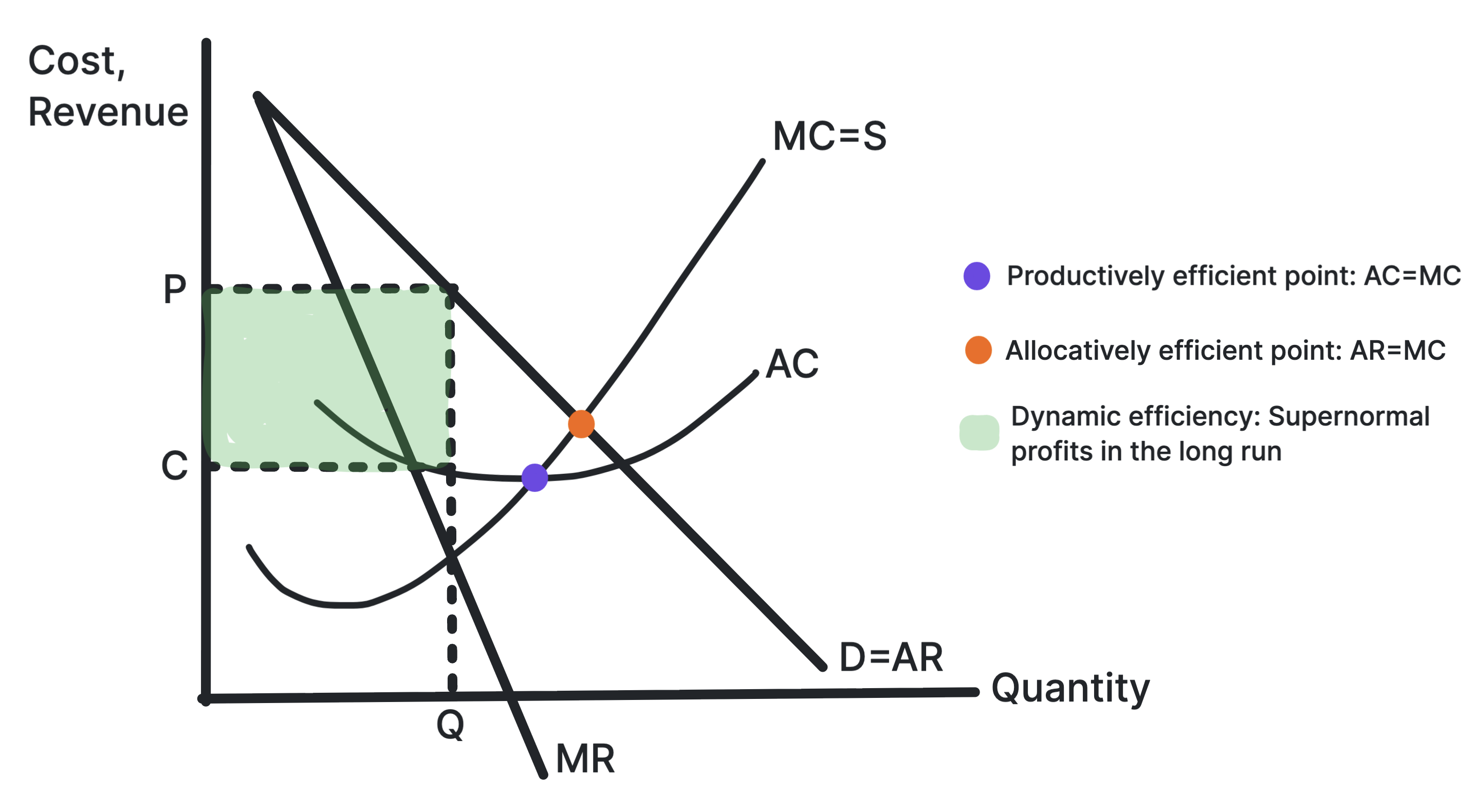

Shows allocative and productive inefficiency for a firm

with market power.

A firm with market power restricts output and charges a

price above marginal cost. It may also produce away from the

minimum point of AC, although supernormal profit can fund

dynamic efficiency.

Use in exams: Use it for monopoly,

oligopoly, regulation and comparisons with perfect

competition.

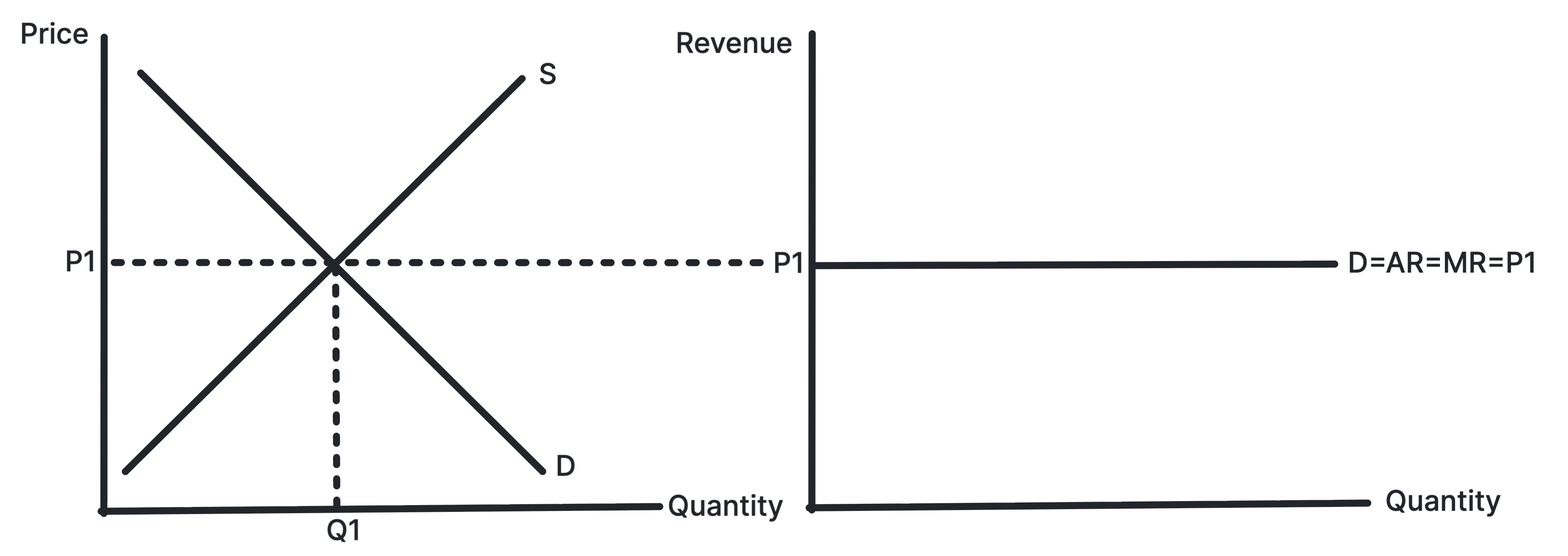

Shows industry supply and demand determining the market

price faced by the firm.

The industry sets the equilibrium price. Each individual

firm is too small to influence price, so it faces a

horizontal demand curve at the market price.

Use in exams: Use it to explain price

taking, perfectly elastic demand and the link between market

and firm diagrams.

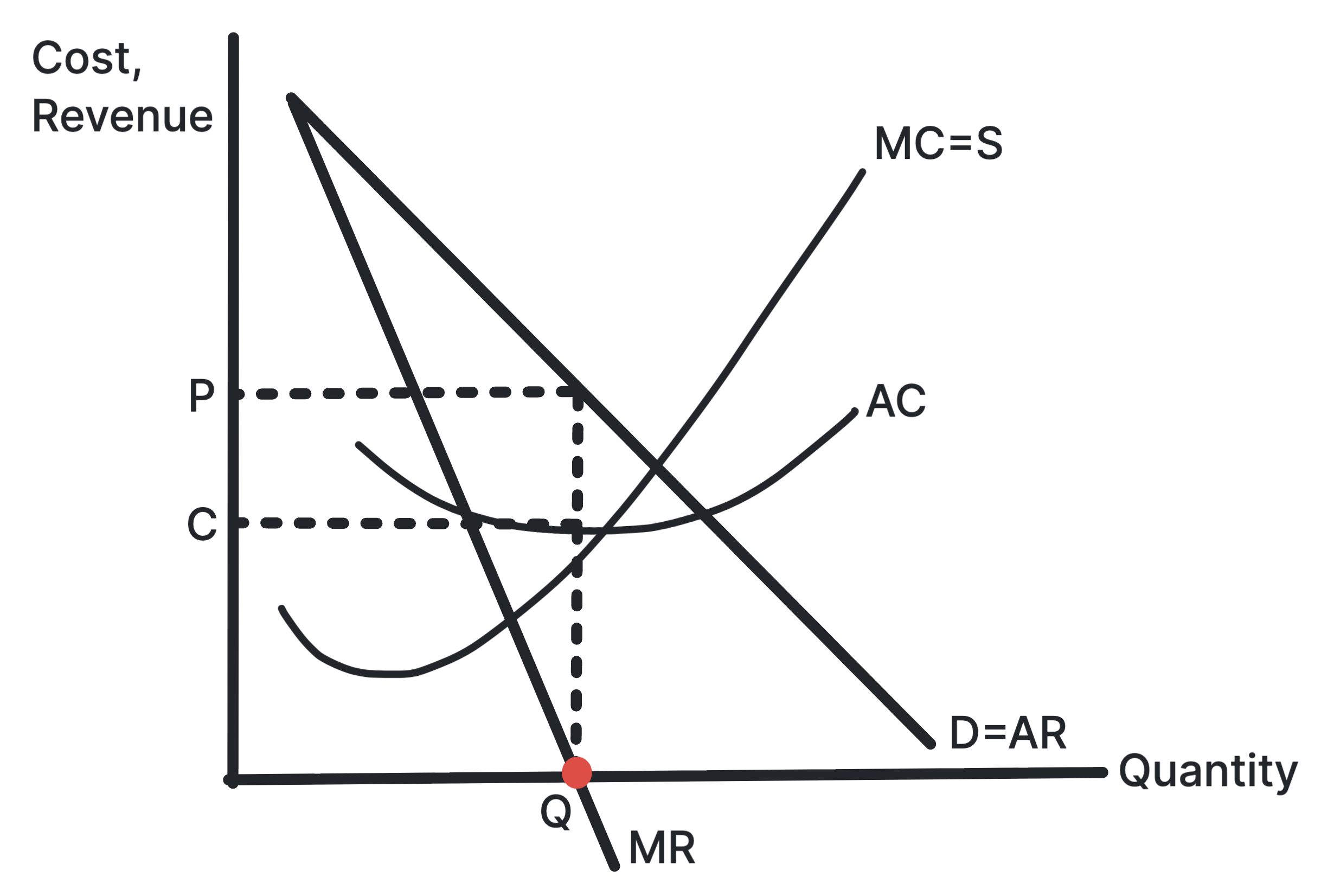

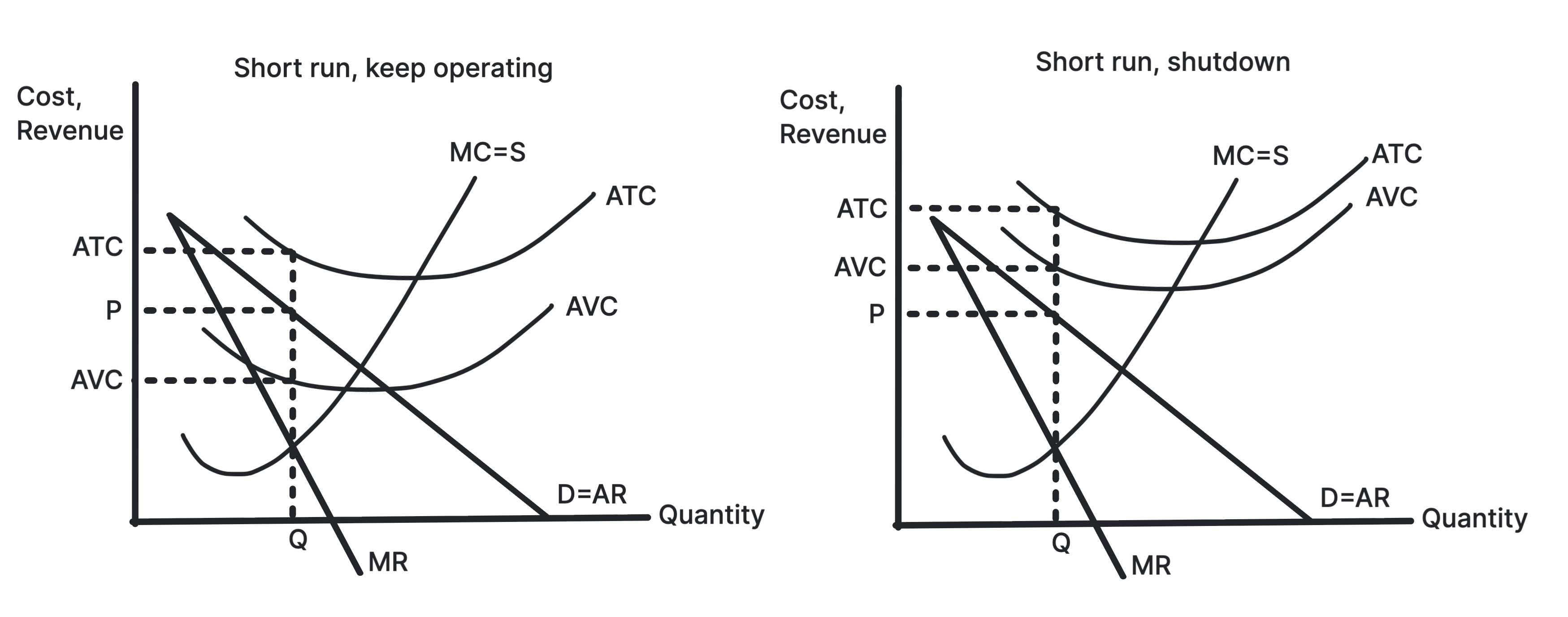

A perfectly competitive firm makes a loss if market price is

below average cost at the output where MC equals MR. It may

continue producing in the short run if it covers AVC.

Use in exams: Use it before explaining how

firms leave the market and losses are removed in the long

run.

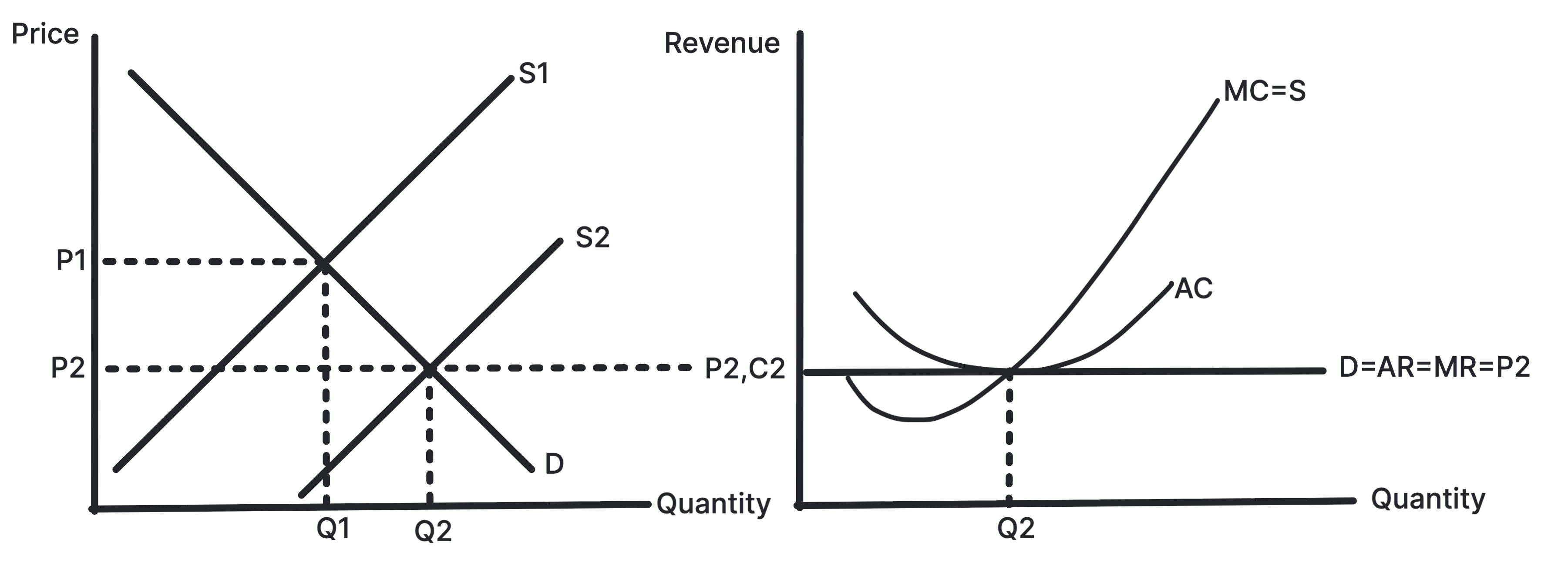

Perfect Competition: Profit to Long-Run Equilibrium

Shows entry shifting the firm's demand curve down until

only normal profit remains.

Supernormal profit attracts new firms into the industry.

Industry supply rises, market price falls, and each firm's

revenue curve shifts down until AR equals AC.

Use in exams: Use it for the long-run

adjustment process and the role of low barriers to entry.

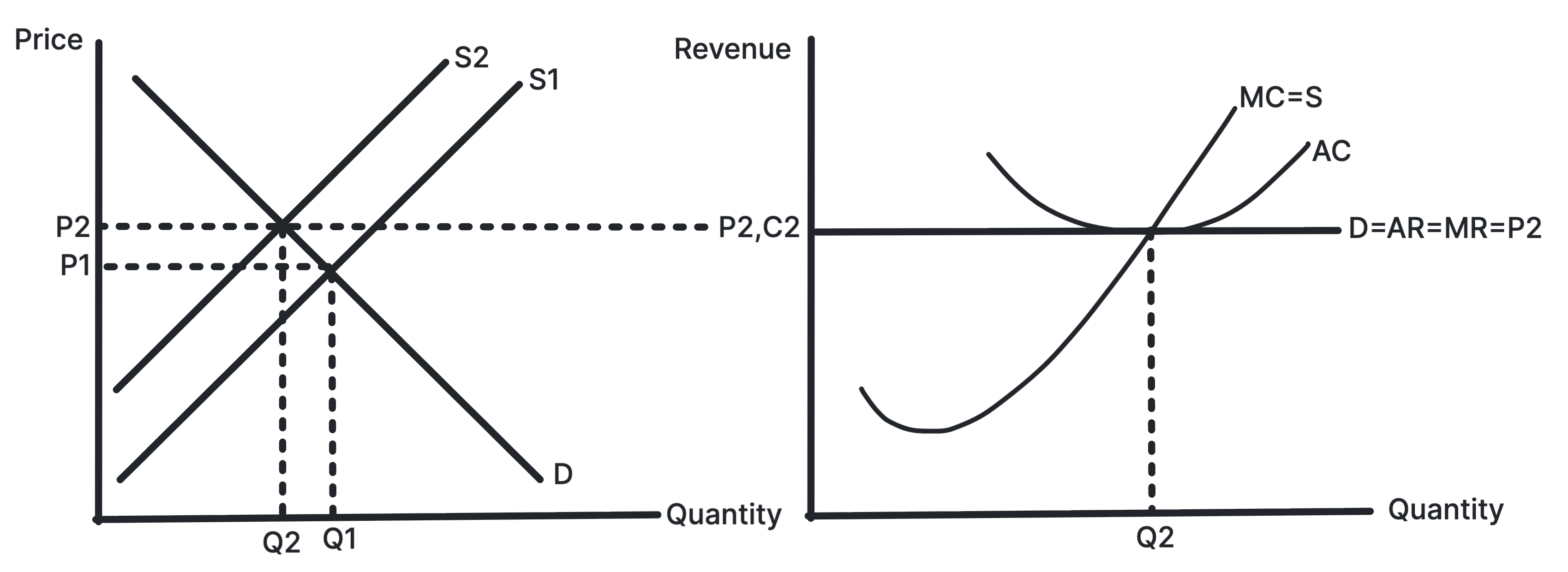

Shows exit shifting the firm's demand curve up until

normal profit returns.

Losses cause some firms to leave the industry. Industry

supply falls, market price rises, and each remaining firm's

revenue curve shifts up until AR equals AC.

Use in exams: Use it to show how perfect

competition removes losses in the long run.

Shows long-run normal profit where AR is tangent to AC.

In monopolistic competition, low barriers to entry mean

supernormal profits are competed away. Product

differentiation leaves the firm with downward-sloping

demand.

Use in exams: Use it for long-run

monopolistic competition and excess capacity.

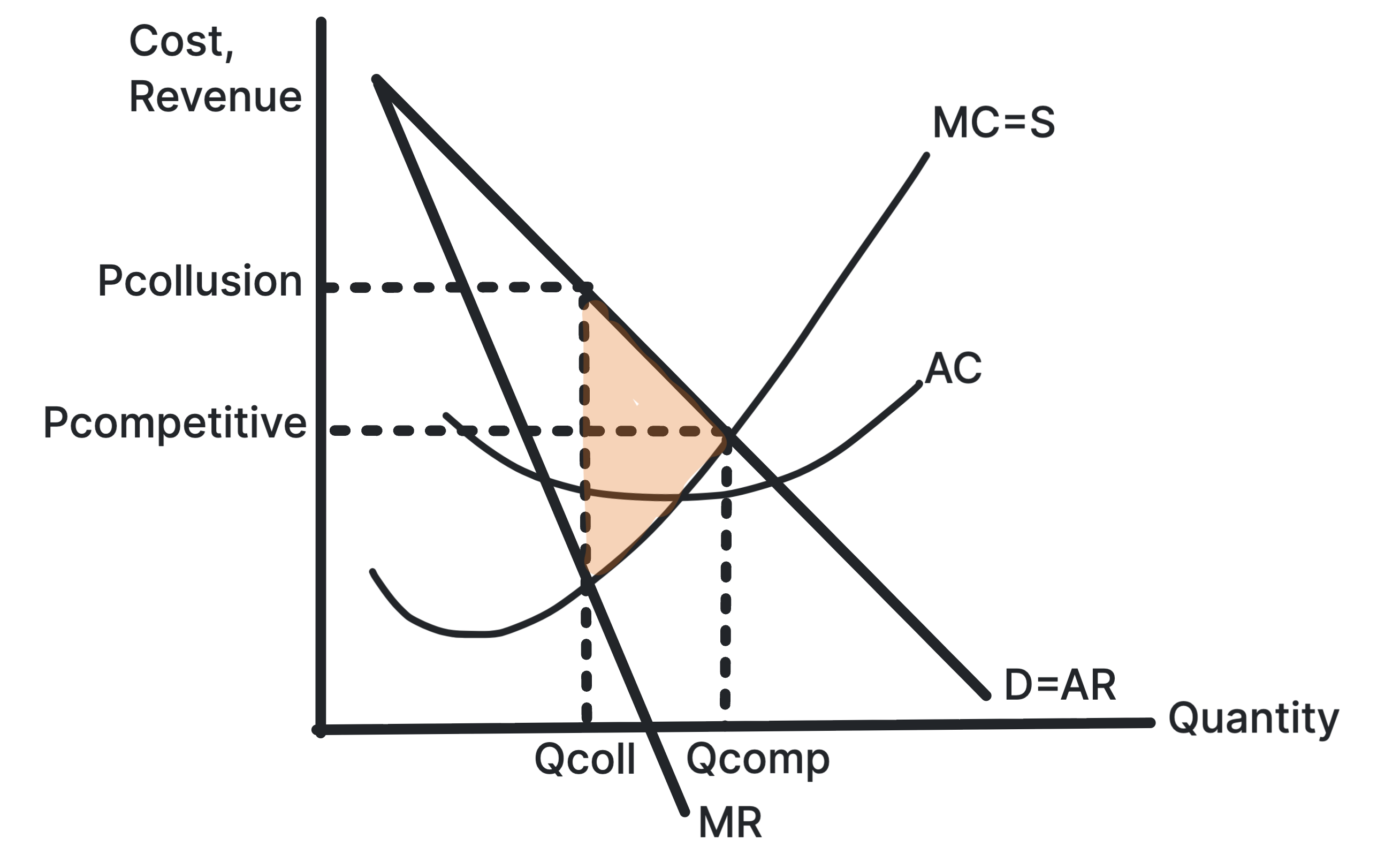

Colluding firms can act like a monopoly by restricting total

output and raising price. This can increase supernormal

profit but worsens consumer welfare.

Use in exams: Use it for cartels, price

fixing, market concentration and competition policy.

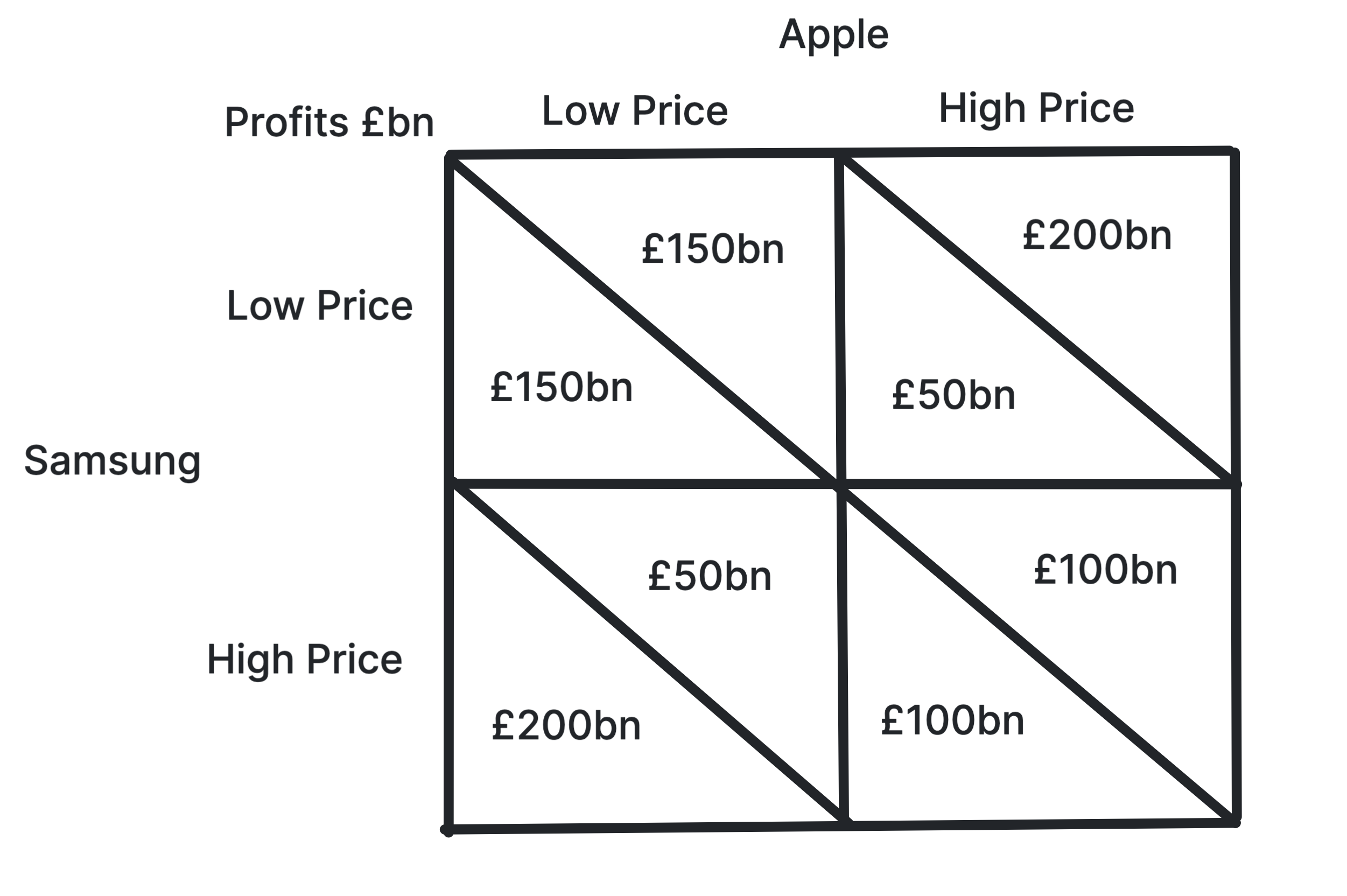

Shows why firms may compete even when joint collusion

would increase combined profits.

Each firm has an incentive to choose the dominant strategy

and compete, even if both firms would be better off if they

could trust each other to collude.

Use in exams: Use it for interdependence,

dominant strategy, Nash equilibrium and unstable collusion.

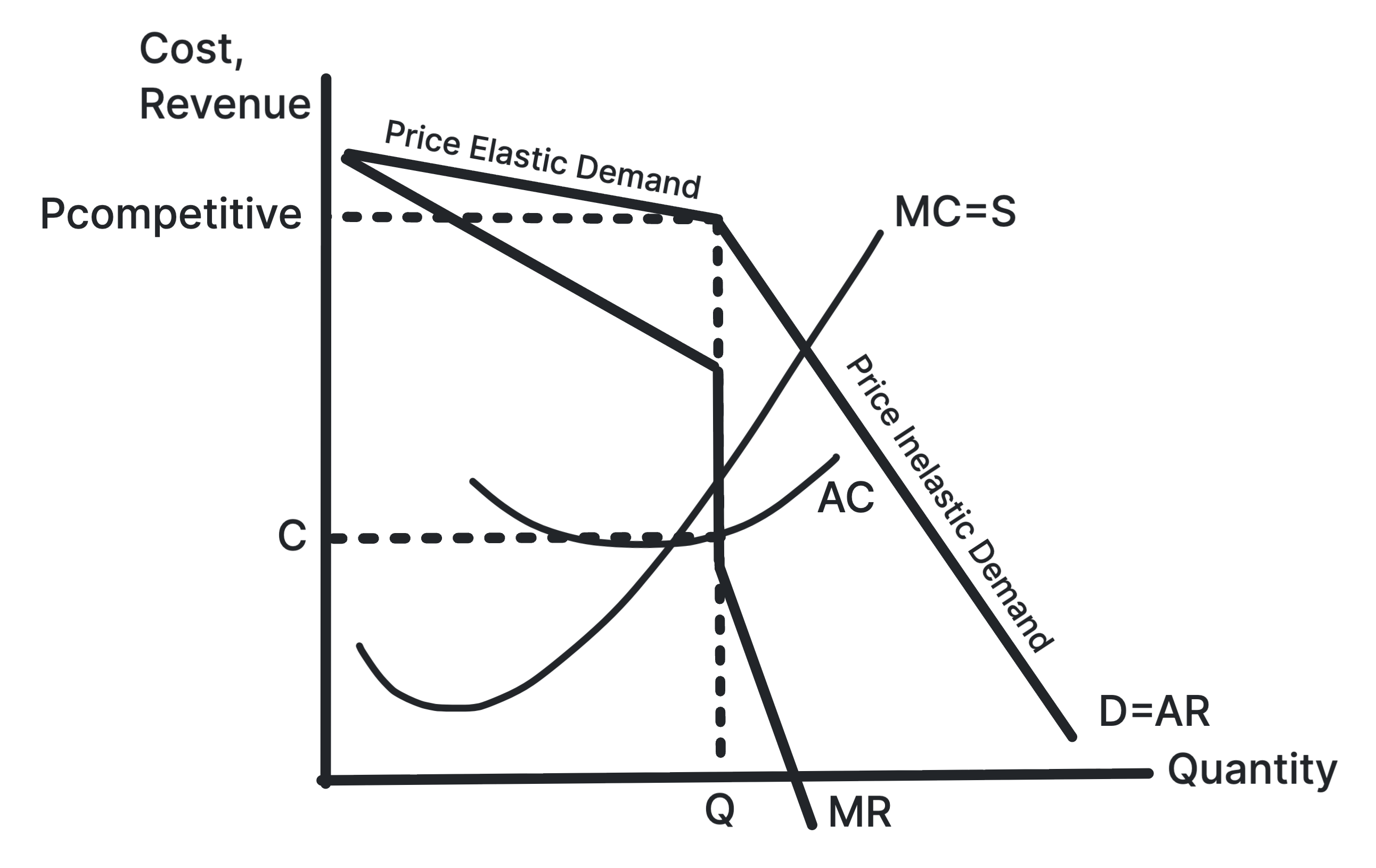

Demand is more elastic above the current price because

rivals may not follow a price rise, and more inelastic below

it because rivals may match a price cut. The gap in MR helps

explain stable prices.

Use in exams: Use it for non-price

competition, interdependence and price rigidity in

oligopoly.

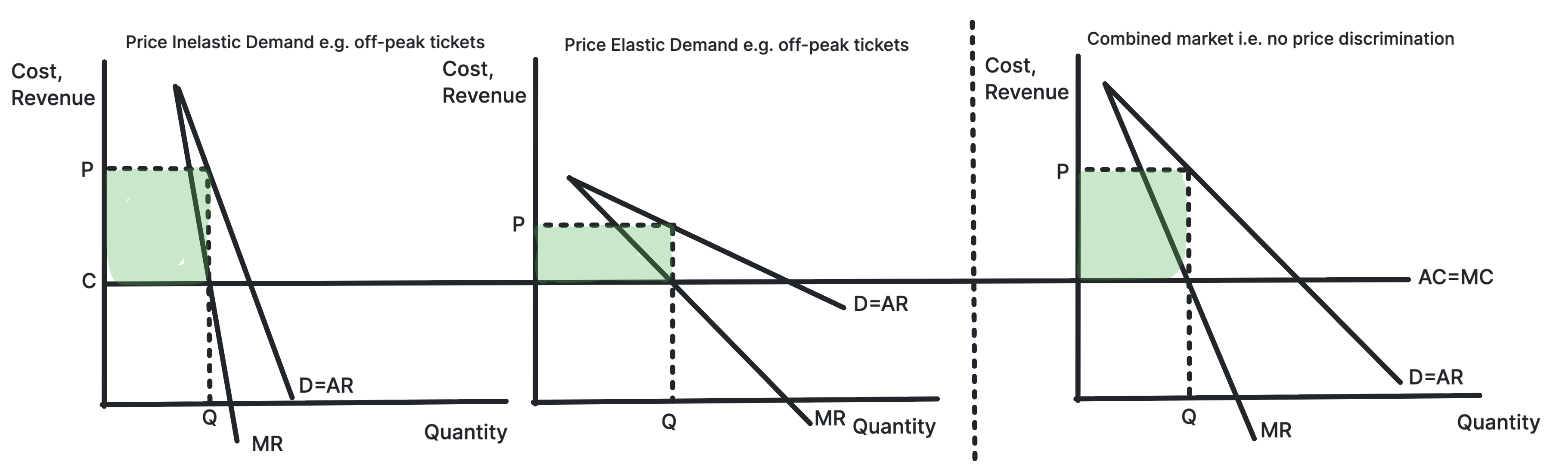

Shows a firm charging a higher price in the more inelastic

market.

A monopoly can split consumers into groups with different

elasticities of demand. It charges a higher price where

demand is more inelastic and a lower price where demand is

more elastic.

Use in exams: Use it for rail fares,

student discounts, peak pricing and welfare evaluation.

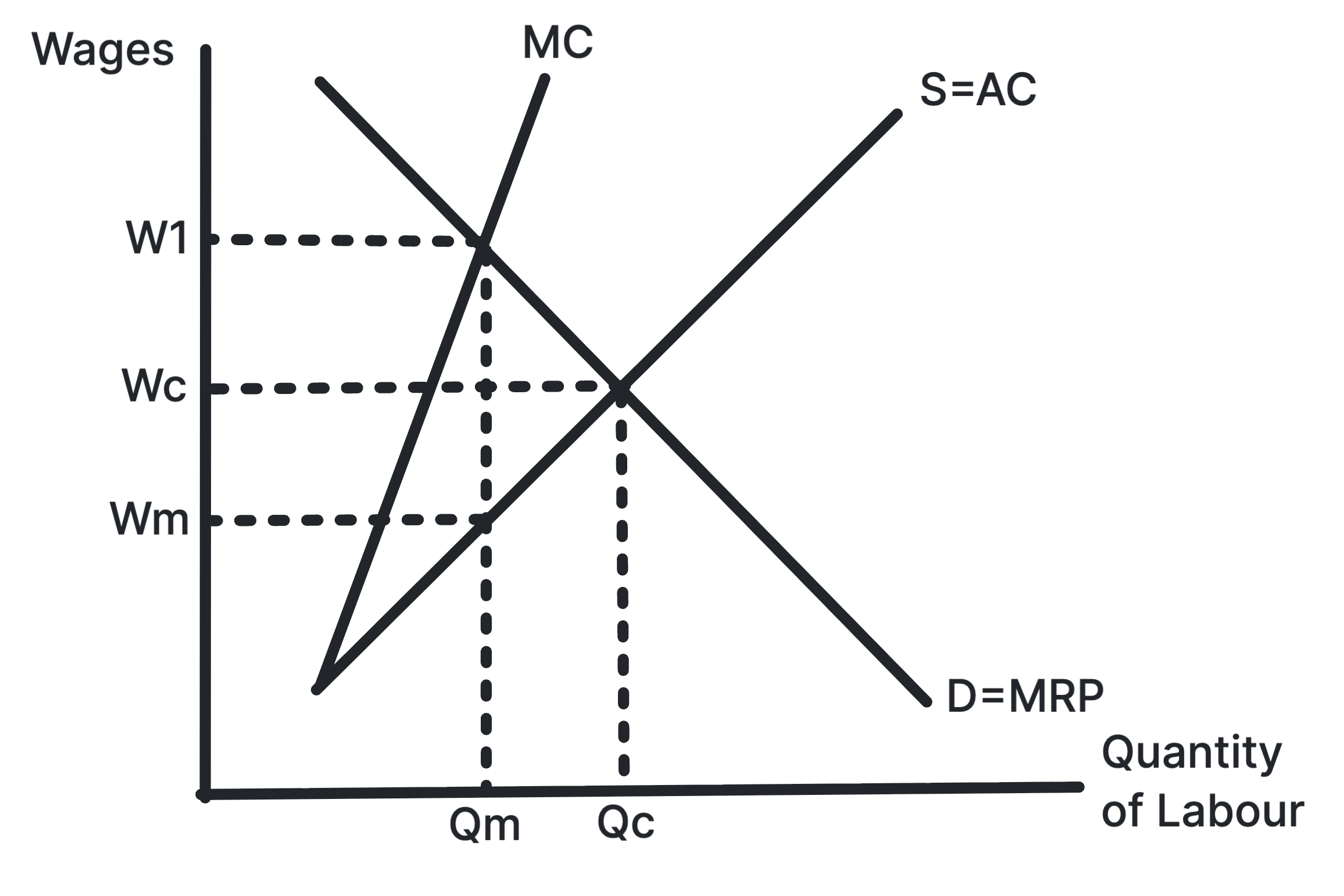

Shows a monopsonist paying a lower wage and employing

fewer workers than a competitive labour market.

A monopsonist faces the whole labour supply curve, so hiring

more workers requires raising the wage. MCL lies above ACL,

and the firm employs where MCL equals MRP.

Use in exams: Use it for employer power,

labour exploitation, minimum wages and public sector labour

markets.

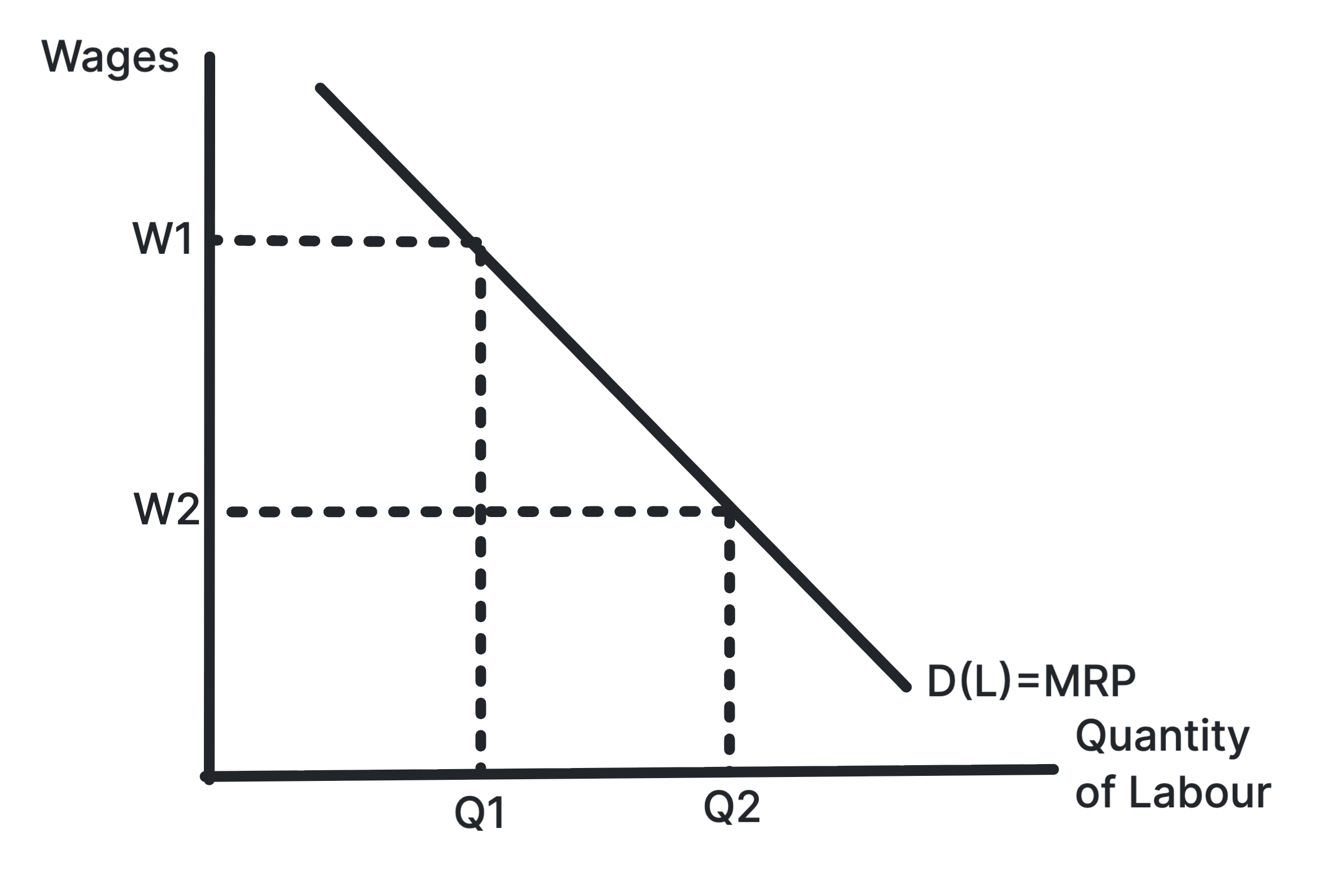

Shows the demand for labour as the marginal revenue

product of labour.

Firms hire workers because labour helps produce output and

revenue. The labour demand curve slopes downward because

marginal physical product often falls as more workers are

added.

Use in exams: Use it for derived demand,

productivity changes, output price changes and labour demand

shifts.

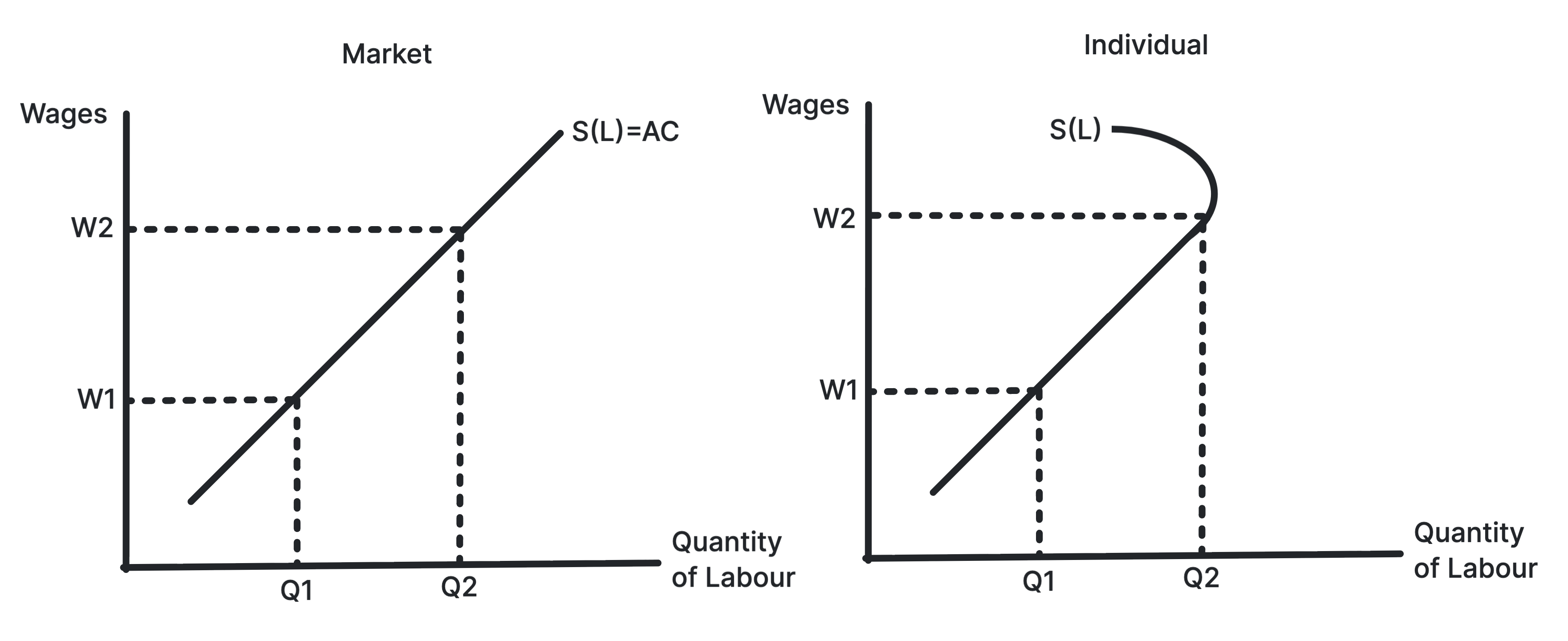

Shows market labour supply and the backward-bending

individual labour supply curve.

Higher wages usually encourage more labour supply, but for

some individuals very high wages may increase the desire for

leisure, creating a backward-bending supply curve.

Use in exams: Use it for substitution and

income effects, occupational labour supply and wage

incentives.

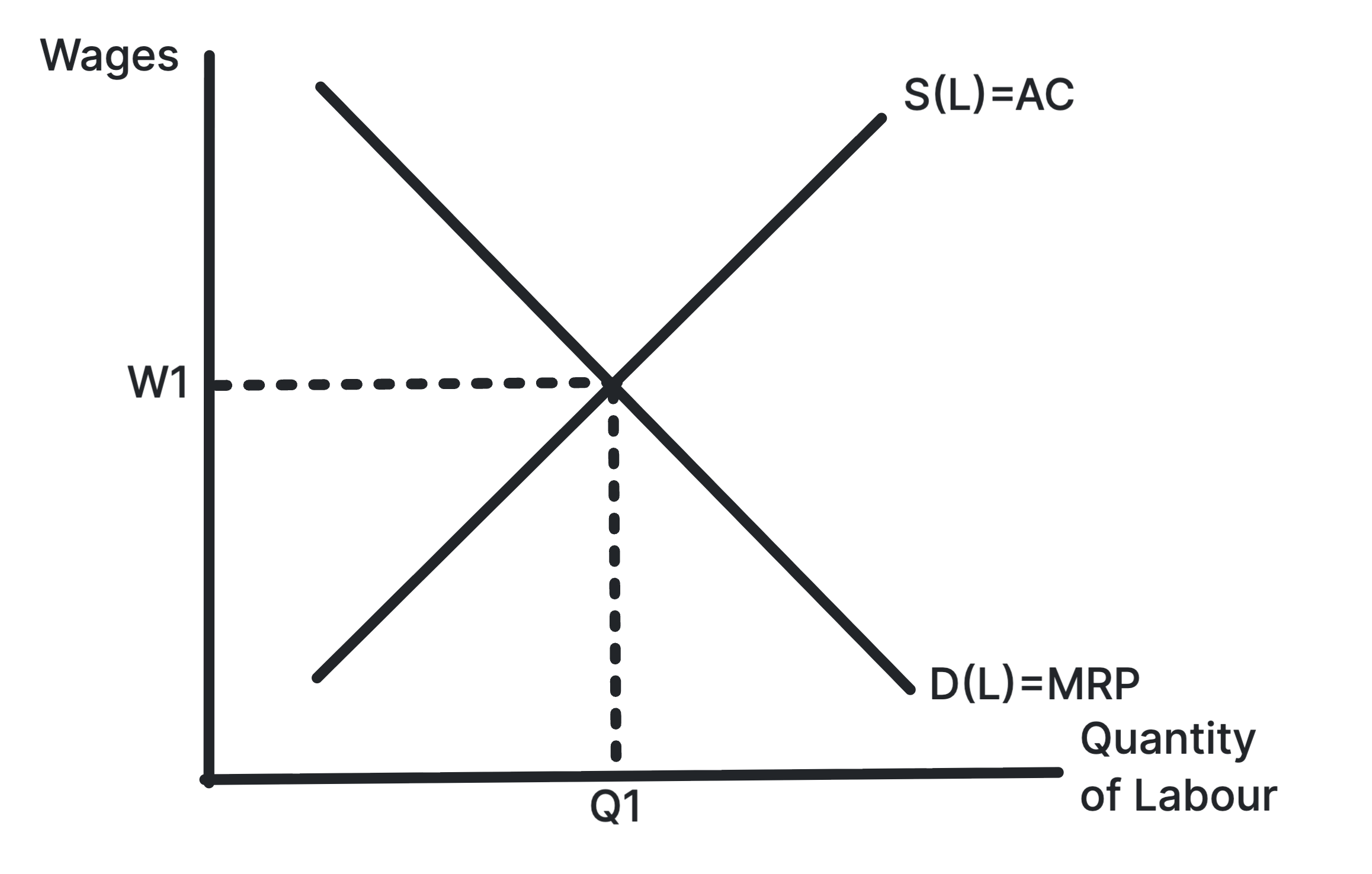

Shows the equilibrium wage and employment level where

labour demand equals labour supply.

In a competitive labour market, the wage rate is determined

by the interaction of labour demand and labour supply.

Changes in either curve change both wages and employment.

Use in exams: Use it for wage differences,

labour shortages, migration, skills and occupational labour

markets.

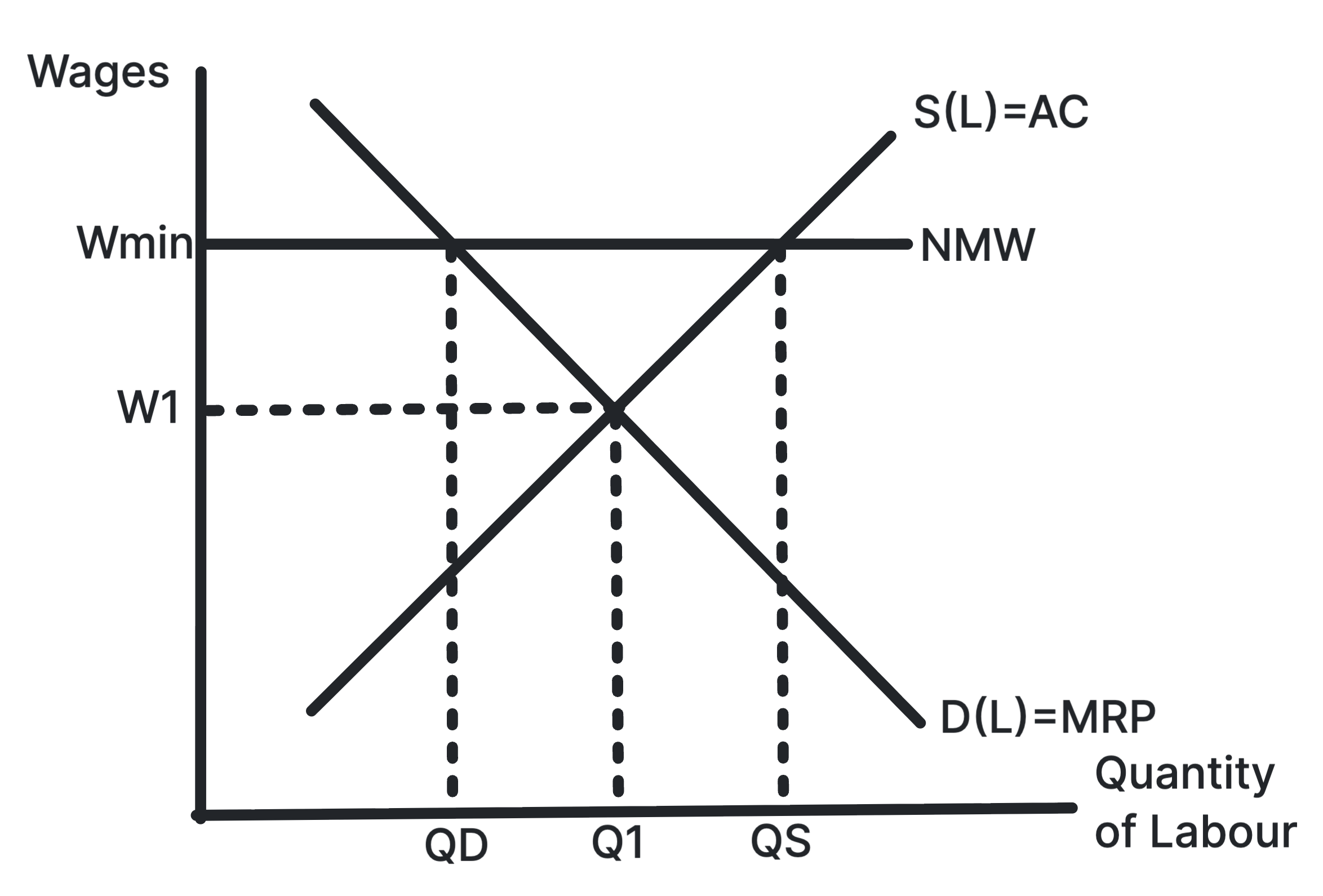

Shows a minimum wage above equilibrium creating excess

supply of labour.

If the legal minimum wage is above the competitive

equilibrium, more workers want jobs than firms want to hire.

This may create unemployment, though outcomes depend on

labour market conditions.

Use in exams: Use it for wage inequality,

unemployment risk, monopsony evaluation and labour market

intervention.

Shows how ownership and pricing objectives can affect

price and output in a natural monopoly.

In a natural monopoly, average costs fall over the relevant

range of output. Public ownership may set a lower price and

higher output than a private monopoly, though incentives may

differ.

Use in exams: Use it for natural monopoly,

state ownership, privatisation, regulation and efficiency

evaluation.