Perfect Competition

Key Characteristics

- Many buyers and sellers: Each firm is infinitely small with negligible market power.

- Homogeneous products: All firms sell identical products, so consumers have no preference for one firm over another.

- Perfect information: Buyers and sellers have full knowledge of prices and products in the market.

- Freedom of entry and exit: Firms can enter or leave the market without restrictions or cost, allowing for long-run adjustments.

These characteristics ensure that firms in perfect competition are price takers, meaning they accept the market price as given and cannot influence it through their own actions.

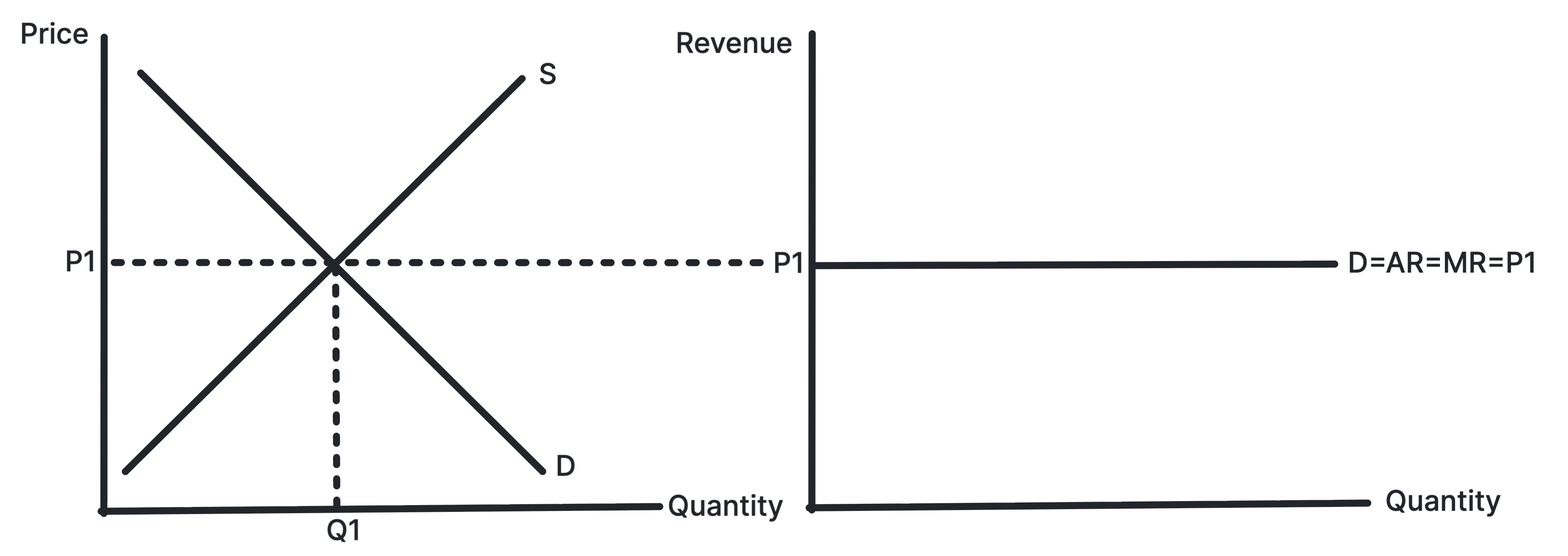

The Firm's Demand Curve

Because firms in perfect competition are price takers, the demand curve facing an individual firm is perfectly elastic, so it is horizontal.

This means \( P = MR = AR \).

The market price itself is determined by market supply and demand.

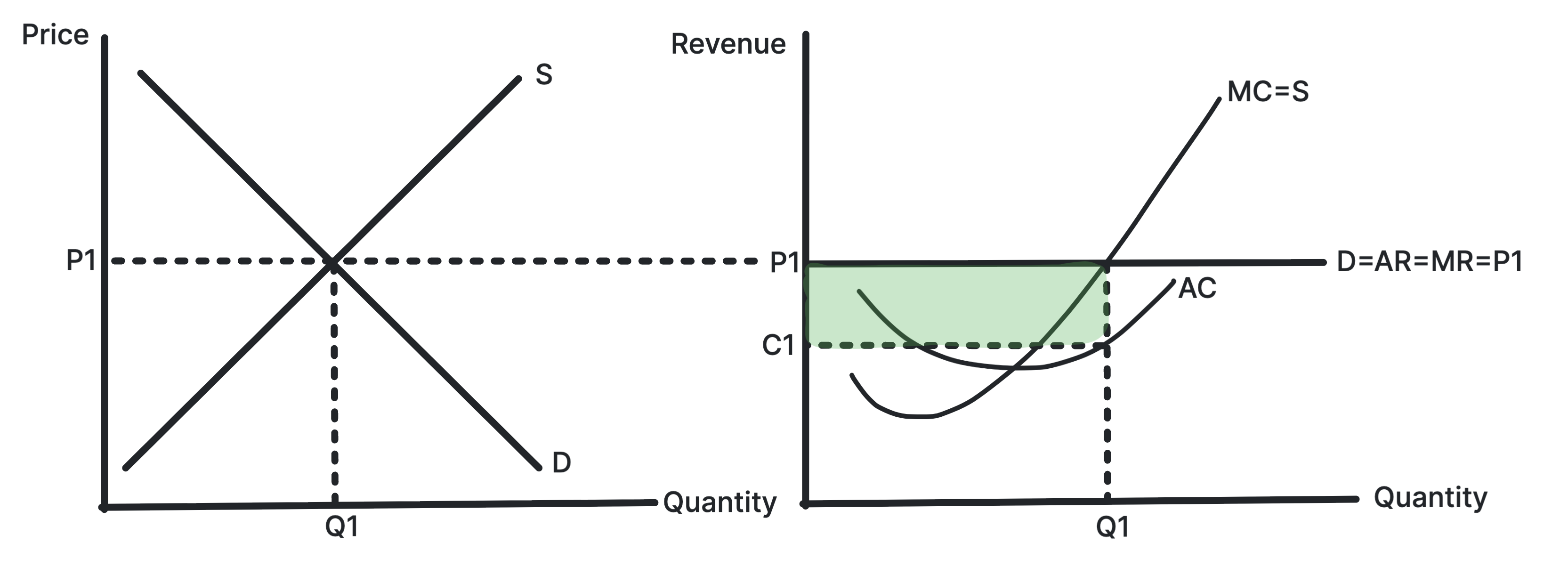

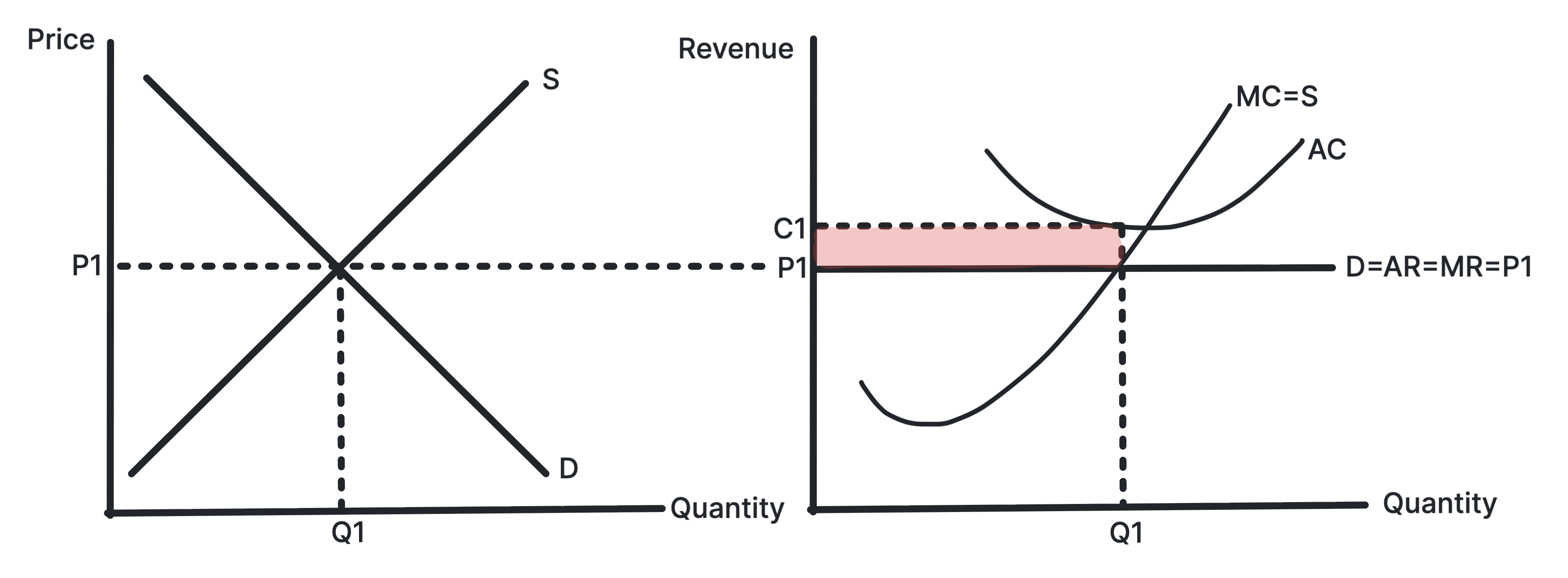

Short-Run Equilibrium: Profit and Loss

The firm maximises profit where \( MC = MR \).

Short run, Supernormal Profit

Short run, Loss

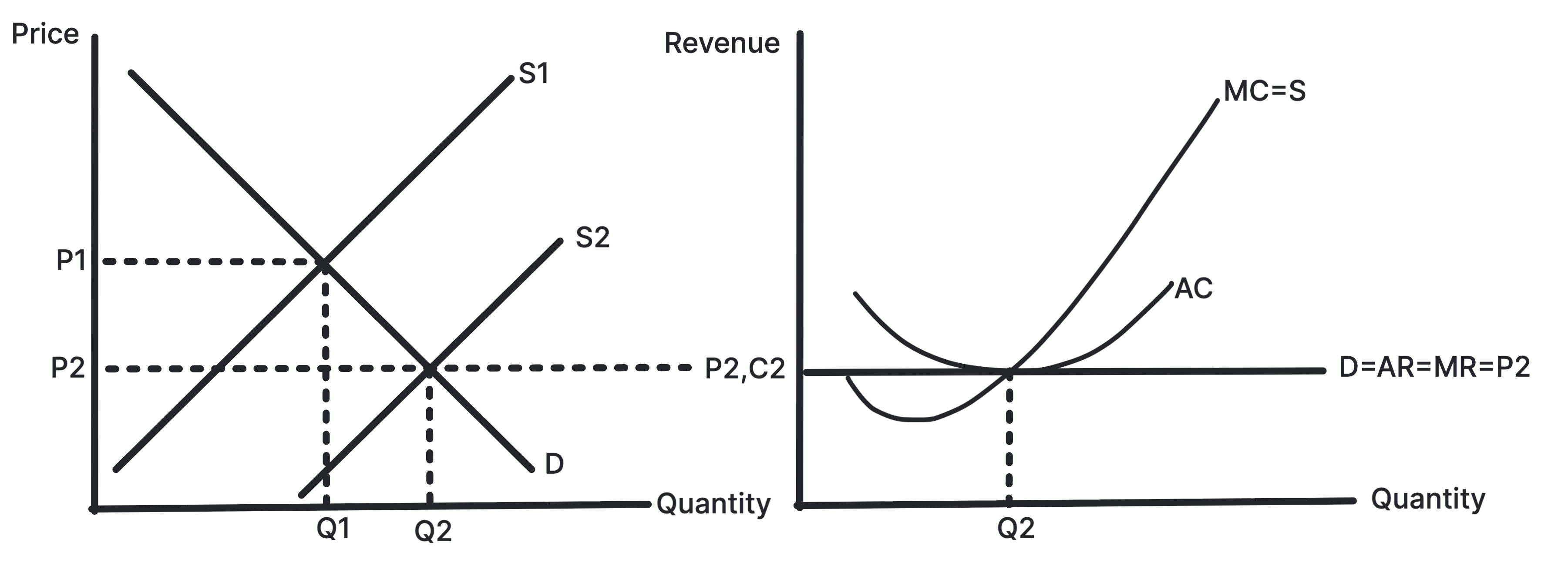

Long-Run Equilibrium: Normal Profit Only

Because there is freedom of entry and exit, perfect competition moves to a long-run equilibrium where firms earn only normal profit, so \( AR = AC \).

From Short-Run Supernormal Profit to Long-Run Equilibrium

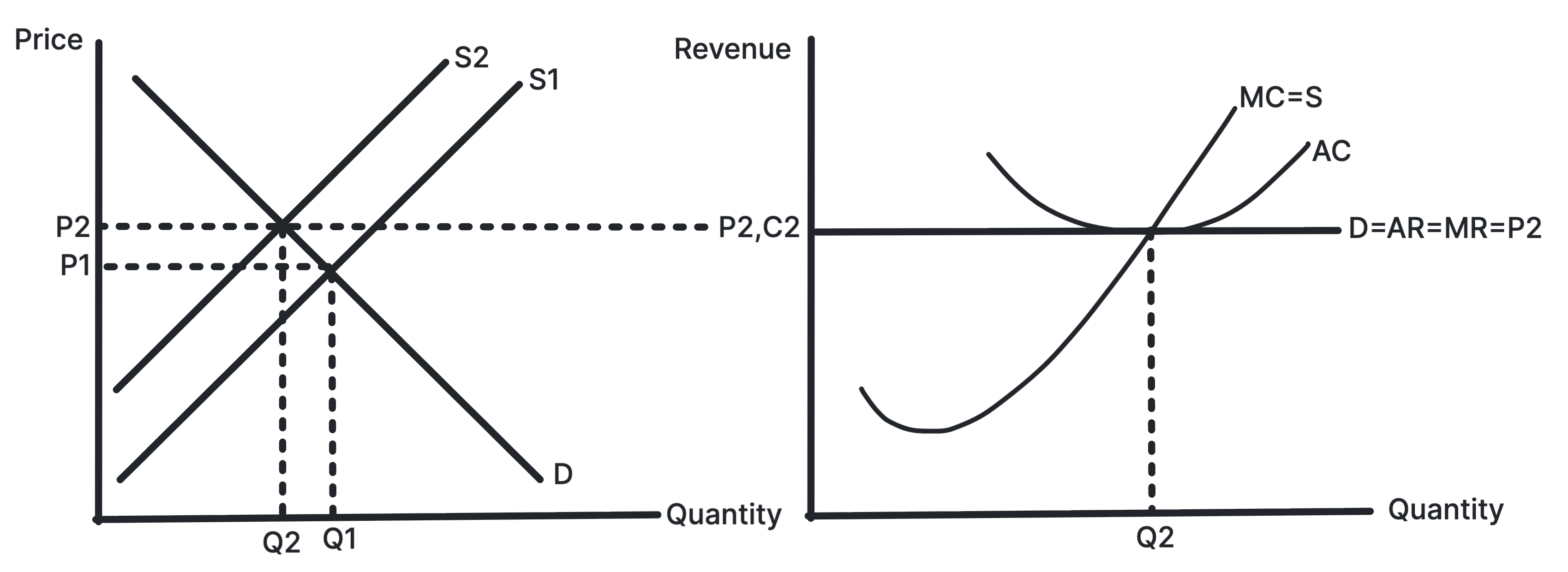

- In the short run, firms may make supernormal profit.

- These profits attract new firms into the industry.

- Industry supply increases and shifts to the right.

- The market price falls.

- The firm's horizontal demand curve falls until it becomes tangent to the minimum point of the AC curve.

- At this point, \( P = AR = AC = MC \) and firms earn normal profit.

From Short-Run Loss to Long-Run Equilibrium

- In the short run, firms may make losses.

- Some firms leave the industry.

- Industry supply decreases and shifts to the left.

- The market price rises.

- The firms' horizontal demand curves rise until they become tangent to the minimum point of the AC curve.

- At this point, \( P = AR = AC = MC \) and firms earn normal profit.

Efficiency in Long-Run Equilibrium

Productive efficiency: Yes - Firms in perfect competition produce at the minimum point of the average cost curve, where \( AC = MC \).

Allocative efficiency: Yes - Firms in perfect competition produce where \( MC = AR \), ensuring that resources are allocated efficiently.

Dynamic efficiency: No - Firms in perfect competition earn only normal profit in the long run, which may limit their ability to invest in research and development.

Test yourself on this topic

Seven original multiple-choice questions on the conditions for perfect competition, the firm as a price taker, and the adjustment to long-run equilibrium.

Practice Questions: 3.4.2 Perfect Competition